*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

10 Important Questions to Ask Hard Money Lenders for Real Estate Projects

Last Updated: March 25, 2025

You want reliable funding for your rental or fix and flip project. Asking the right questions to ask hard money lenders will help you pick a solid financing option.

This short guide shows you how these loans work so you can feel confident when you talk terms. By tackling rates and loan conditions up front you stay in control of your investment plans.

You're about to see which factors matter most from loan duration to fees and proof of funds. That way you know what to expect and can lock in the loan that suits your goals.

Understanding Hard Money Lending

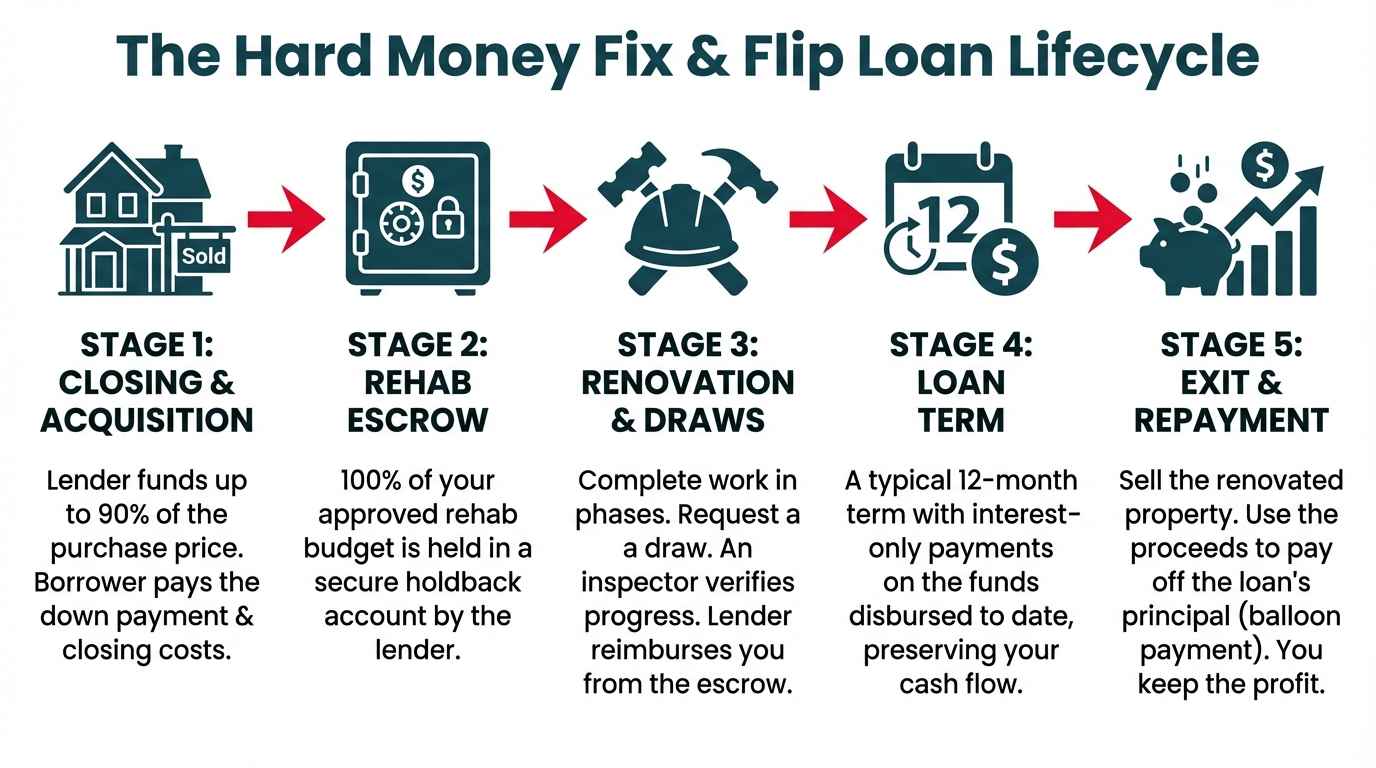

Hard money lending is a fast way to secure real estate funds. A hard money lender bases terms more on collateral than on your credit. This helps you gain capital if you do not qualify for standard funding.

- Know what a hard money loan covers. It often funds fix-and-flip or rental projects. Rates are higher due to the added risk that a private lender or a private money lender might face.

- Check the typical duration. Some terms run 6 to 24 months. Extensions are possible if the project needs more time.

- Study the fees. Common charges include points, origination, and underwriting costs. The total expense might be acceptable if timelines are tight.

- Ask about the process. Certain lenders need fewer documents than traditional sources. This saves time when speed is a priority.

Preparing Before You Contact A Lender

Early prep builds confidence. Sort key details in advance for any hard money or private lender discussions.

Gather Your Financial Information

Collect 2 forms of identity and 3 months of bank statements. Gather property details that apply to your fix-and-flip or rental plans. Present updated credit reports if they are available. A current valuation helps when a hard money lender or a private money lender wants a property overview. Clarify assets or outstanding debts to give a clear picture of your financial stability. Keep each document in a single folder for fast reference. This clarity often supports a quick hard money loan process.

Define Your Real Estate Goals

Pin down the target period for renovations or rental terms. Consider a 6 to 24-month timeline if a fix-and-flip is on your agenda. Set a target profit or preferred rental income for each project. Estimate possible improvements before finalizing your budget. Decide if the plan involves an exit strategy once the project is complete. Hard money can be ideal for quick acquisitions while a private lender or private money lender might fit other scenarios. State your desired funding amount with an eye on loan interest and fees. This guidance shows you are ready to discuss your plan with confidence.

Key Questions To Ask Hard Money Lenders

When you approach a lender, it's essential to ask key questions that will give you confidence in their service and the loan structure. Here are some important queries to consider:

What are your interest rates, and how do they compare to other lenders?

What is the maximum loan-to-value (LTV) ratio you offer?

What are your loan terms and conditions, and how flexible are they?

What is the repayment schedule, and are there any prepayment penalties?

What fees will I be charged besides interest?

What are the collateral requirements for this loan?

How quickly can the funds be disbursed after approval?

Do you offer extensions if the project runs over schedule?

What is your process for appraisals and inspections?

How often do you require updates on the project’s progress?

Evaluating Lender Credibility And Red Flags

Check if the hard money or private lender meets your needs. Look for clues that confirm honesty and fulfill your project requirements.

Ask About Experience And Track Record

Request data on years in the business and number of deals closed. A hard money lender or private lender with a solid record can share real numbers on past funding. Ask how many projects stayed on schedule or under budget. Seek insight on property types they have financed. Some focus on fix-and-flip sites while others deal with rentals. Ask about credit flexibility or equity requirements. That step helps match your project profile with a lender who has handled similar work. If possible, request examples of previous clients who had similar project sizes or durations. Their feedback might show if this lender can adapt to changing conditions.

Check Licensing And References

Verify certificates or business permits the hard money lender or private money lender claims. In some regions, local authorities require specific registrations to fund real estate deals. Request proof of all documentation. Contact at least two of their past borrowers. Ask if payments were processed promptly and if closing times matched the initial claims. Direct statements from actual clients can show if the lender acts as promised. Look for lenders who share a consistent message about rates, terms, and fees. Check if they provide a customer service line or a clear way to address any concerns. That step promotes trust in the long run.

Identify Warning Signs

Watch for big charges that appear before you sign official papers. Hidden rates or vague loan terms might point to possible issues. A potential provider who sidesteps basic questions or dismisses your project specifics might be unreliable. Intensive pressure to finalize your contract fast can signal deeper problems. Stay cautious if they skip basics like thorough appraisals or honest assessments of repair budgets. If the lender tries to rush you past your due diligence, pause and review each detail to protect your investment.

How to Choose the Right Hard Money Lender

Selecting the right hard money lender is crucial for the success of your project. While there are many lenders available, they vary greatly in terms of rates, fees, and service quality. Here’s what to look for when comparing lenders:

a) Reputation: Check online reviews and ask for referrals from other real estate investors to ensure you are dealing with a trusted lender. A good reputation often signifies reliability and customer satisfaction.

b) Loan Terms and Conditions: Make sure the lender's terms align with your project’s needs. Look for flexibility in repayment schedules, loan duration, and the potential for extensions if needed.

c) Communication: The lender should be responsive and easy to communicate with. Clear communication throughout the process ensures that you can quickly resolve any issues that arise.

d) Speed of Funding: Since you may need to move fast on a property, it’s essential to choose a lender that can provide quick funding. Some lenders can approve and disburse loans in a matter of days, while others may take weeks.

How Interest Rates Impact Your Return on Investment

Interest rates play a significant role in determining the overall cost of your hard money loan. While these loans tend to have higher interest rates than traditional financing, it’s important to understand how the rate will affect your investment’s return.

Short-Term vs. Long-Term Loans: If you are flipping a property and planning to sell quickly, a higher interest rate may be less of an issue because the loan will be paid off in a short period. However, for rental properties, higher rates could affect long-term profitability. Ensure your investment plan accounts for the added costs of the loan.

How to Calculate Your Costs: Understanding how interest compounds over time helps you estimate your total repayment amount. Use an online loan calculator to get a sense of how different rates will impact your budget.

Strategies to Minimize Interest Costs: If possible, try to negotiate better terms. A larger down payment, for instance, can lower the loan-to-value (LTV) ratio, which may lead to a lower interest rate.

The Role of Property Appraisal in Hard Money Loans

Property appraisal is an essential part of the hard money lending process. The appraisal helps the lender determine the value of the property you're financing, ensuring that it’s enough to cover the loan if needed.

Why Appraisals Matter: The lender uses the property’s value to determine the loan amount they are willing to offer. If the property’s value is lower than expected, the lender may reduce the loan or require a larger down payment from you.

How to Prepare for an Appraisal: Make sure the property is in good condition and highlight any recent upgrades or repairs that could increase its value. This can help ensure that the appraisal comes back higher and improves your chances of securing the loan amount you need.

What Happens if the Appraisal Comes In Low? If the appraisal value is lower than anticipated, you may need to come up with a larger down payment or reconsider the scope of your project. Some lenders offer to lend based on the property’s after-repair value (ARV), which could work to your advantage in a fix-and-flip situation.

Common Issues And Troubleshooting

Unexpected expenses or timing problems might arise during a hard money loan. Each section addresses ways to handle frequent roadblocks.

Dealing With Unexpected Costs

Renovation expenses can shift without warning.

- Establish a fund for surprises. Rely on 10% to 20% in reserves if estimates change.

- Confirm if your hard money lender or private lender allows new draws. Example: a $50,000 rehab plan might increase to $57,500 if repair quotes rise 15%.

- Request detailed bids from contractors. Spot possible price variations if materials spike.

Handling Potential Delays

Project slowdowns can affect completion timelines.

- Communicate changes with your hard money lender if tasks slip by 2 weeks.

- Check extension clauses. Some private money lender contracts might charge added fees if the loan goes past 12 months.

- Update project milestones in weekly increments. Track each phase if you want to detect delays early.

- Organize documentation. Show revised progress schedules if contractors miss targets.

Key Takeaways

- Understand that hard money loans rely heavily on collateral rather than credit, providing faster but often more expensive funding options.

- Prepare essential documents (financial statements, property details, and identity proof) in advance to streamline your application and approval.

- Clarify fees, interest rates, and loan durations (often 6–24 months) so you can forecast costs and assess your project’s feasibility.

- Investigate a lender’s track record and licensing, verifying past deals and client feedback to ensure credibility.

- Watch for warning signs like hidden charges or overly aggressive sales tactics, and maintain clear communication about project timelines to prevent unexpected setbacks.

Conclusion

A well-prepared list of inquiries keeps you in control of your financial journey. Showing lenders you’ve done your homework can spark honest discussions about terms and expectations. By actively engaging and clarifying potential hurdles, you gain a clearer picture of whether a hard money loan suits your needs.

Stay proactive by comparing multiple lenders and tracking responses to your questions. This extra effort helps you avoid unwelcome surprises and fosters better collaboration throughout your project. Remember that every question helps shape a relationship built on trust. Armed with focused strategies, you’re set to make confident financing decisions.

Frequently Asked Questions

What is hard money lending?

Hard money lending is a financing option where loans are backed by property collateral rather than credit scores. It’s common for real estate investors who need quick funds for fix-and-flip or rental projects. These loans typically have higher interest rates but offer faster approvals than traditional mortgages.

What do hard money loans typically cover?

They usually cover the purchase price and renovation costs for properties. This includes repairs, materials, and sometimes fees tied to construction. Since these loans focus on the property’s value, they can be a good fit when speed and collateral-based financing are priorities.

How long do hard money loans last?

Most hard money loans range from 6 to 24 months. Some lenders can grant extensions if renovation or sale takes longer than planned. Shorter terms help investors complete projects quickly and move on, but you should verify specifics with each lender.

What fees are common with hard money loans?

Typical fees include points (a percentage of the loan), origination charges, and underwriting costs. These can add to project expenses. Ensure you understand all fees before signing, and confirm whether any hidden charges might affect your overall budget.

How should I prepare before contacting a lender?

Gather essential documents like identification, bank statements, property details, and credit reports. Having this information organized speeds up the approval process. Define your goals—such as renovation timelines, profit targets, and exit strategies—to show lenders you have a solid plan.

Why verify a lender’s track record?

Experience and a proven history of successful projects indicate reliability. Checking their track record, licenses, and past deals helps you avoid unprofessional lenders. Request references from previous borrowers or reviews to ensure your lender meets expectations and avoids cynical practices.

What are potential warning signs from a lender?

Look out for hidden fees, pushy sales tactics, or unclear repayment terms. Legitimate hard money lenders are transparent about rates, loan conditions, and penalties. If you feel pressured or sense vague communication, consider seeking alternative financing options.

How do I handle unexpected costs?

It’s wise to have a buffer of 10% to 20% for surprise expenses. Confirm if your lender allows for extra draws if the renovation budget exceeds your initial plan. Keeping open communication and proper documentation with your lender is crucial for adjustments.

How can I avoid project delays?

Plan thoroughly, maintain organized paperwork, and communicate timeline changes early with your lender. Check your loan agreement for extension clauses, and track milestones to ensure you’re meeting projected deadlines. Staying prepared helps keep your project running smoothly.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.