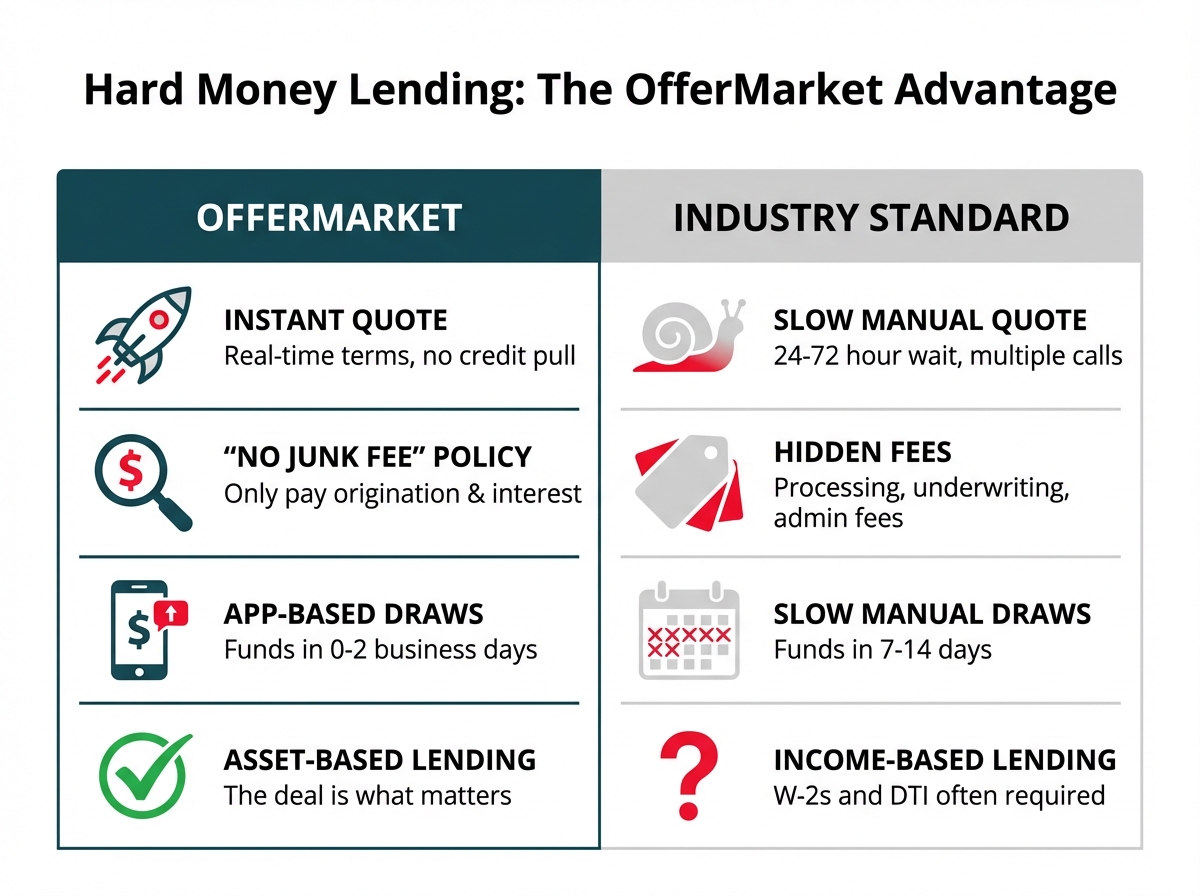

*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Fix and Flip Calculator

Last updated: June 9, 2026

Every successful flip starts the same way: with honest math done before any money changes hands. The difference between a profitable project and an expensive lesson usually is not the renovation skill or the finish quality. It is whether the investor ran the numbers correctly at the outset and built in enough margin to survive the things that inevitably go wrong. A fix and flip calculator is the tool that forces that discipline, turning a gut feeling about a deal into a defensible projection. Here is how the key inputs work, how the financing is structured, how taxes hit your profit, and what to do when a flip is not behaving like a flip.

What a Fix and Flip Calculator Actually Does

At its core, a fix and flip calculator answers one question: if I buy this property at this price, spend this much on renovations, hold it for this long, and sell it at this value, what is left for me at the end? It pulls together the purchase price, the rehab budget, the financing costs, the holding costs, the selling costs, and the projected sale price into a single profit figure and a return percentage.

The value of the exercise is not the final number so much as the structure it imposes. A calculator makes you confront every cost, not just the obvious ones, and it makes you state your after repair value explicitly rather than assuming the home will simply sell for more than you put in. The investors who lose money on flips are almost always the ones who skipped or fudged an input. Let us walk through the ones that matter most.

ARV: The Number Everything Hangs On

After repair value, or ARV, is the estimated market value of the property once your renovations are complete. It is not your purchase price plus your rehab spend. It is what the finished property will actually sell for, determined by recent sales of comparable renovated homes in the immediate area. Every other number in a flip analysis ultimately answers to the ARV, because it is both your exit price and the basis lenders use to size your loan.

The single most common way investors blow up a flip is by inflating the ARV. An optimistic ARV makes a marginal deal look great on paper and a bad deal look acceptable. The discipline here is to pull recent, nearby, genuinely comparable sales of finished homes, and when in doubt, to lean conservative. A deal that only works with an aggressive ARV is not a deal.

Rehab Costs and the Scope of Work

The rehab budget is where flips are won or lost on the cost side, and it begins with a detailed scope of work. A scope of work is an itemized plan of everything you intend to do to the property, from the kitchen and baths down to flooring, paint, roof, HVAC, and any structural or layout changes. The more specific it is, the more accurate your budget and the fewer surprises mid-project.

A vague rehab estimate is a liability. "Around 50,000 dollars" is not a budget, it is a wish. A real scope breaks the work into line items with material and labor costs for each, which lets you catch the gaps before they catch you. It also serves a second purpose, because lenders and appraisers reviewing a subject-to ARV will want to see exactly what work justifies the projected finished value. A clear scope supports a stronger ARV.

Whatever your scope totals, build in a contingency. Experienced flippers add a cushion, often ten to twenty percent, for the hidden conditions that surface once walls are open. Older properties in particular hide problems that no walkthrough reveals. The contingency is not padding, it is realism.

Loan to Cost (LTC)

When financing a flip, two leverage ratios govern how much a lender will advance, and the first is loan to cost, or LTC. LTC measures the loan amount against the total cost of the project, meaning the purchase price plus the rehab budget. A lender offering, say, ninety percent LTC on the purchase and one hundred percent of the rehab is willing to fund most of your acquisition and all of your renovation, provided the other ratio also checks out.

LTC matters because it determines how much cash you must bring to the table. The higher the LTC a lender offers, the less of your own capital is tied up in the deal, which improves your return on the cash you actually invest. It also explains why your down payment and out-of-pocket costs are a function of both the price and the rehab, not the price alone.

Loan to After Repair Value (LTARV)

The second leverage ratio is loan to after repair value, or LTARV, sometimes written ARLTV. This caps the total loan as a percentage of the projected finished value. A lender offering seventy percent LTARV on a property with a 300,000 dollar ARV will lend up to 210,000 dollars total, including both acquisition and rehab.

In practice, a fix and flip lender applies both LTC and LTARV and lends up to the lower of the two. LTC keeps the loan tied to what you are actually spending, while LTARV keeps it tied to what the finished property is worth, protecting the lender if your ARV proves optimistic. Understanding that your loan is constrained by both ratios is essential, because a deal can pencil out on cost but get capped by value, leaving you to cover the gap in cash. A good calculator models both so you know your true cash requirement before you commit.

The Costs Investors Forget

The purchase and rehab are the obvious costs. The ones that quietly erode profit are the holding costs and the transaction costs, and a proper calculator captures all of them.

Holding costs accrue every month you own the property and include loan interest, property taxes, insurance, utilities, and any HOA dues. They are why time is the enemy of a flip. A renovation that runs two months long does not just delay your payday, it adds months of carrying cost that come straight out of profit. This is also why the holding period is one of the most sensitive inputs in the whole analysis.

Transaction costs hit on both ends. On the buy side there are closing costs, lender points, and title fees. On the sell side there are agent commissions, transfer taxes, and seller-paid closing costs, which together commonly run in the high single digits as a percentage of the sale price. Investors who model only the purchase, rehab, and sale price routinely overstate their profit by tens of thousands of dollars because they ignored the cost of getting in and out.

ROI: Measuring the Return Correctly

Return on investment ties the whole analysis together, but it must be measured correctly to mean anything. Profit is the sale price minus everything: purchase, rehab, holding costs, financing costs, and selling costs. ROI expresses that profit as a percentage, and the key is to measure it against the cash you actually invested, not the total project cost.

Because flips are typically leveraged, the cash-on-cash return is what matters. If you put 60,000 dollars of your own money into a deal and walk away with 40,000 dollars in profit, that is a far better return on your capital than the raw profit suggests, precisely because the lender funded most of the project. This is also why LTC and LTARV connect directly to ROI: the more of the deal the lender funds, the less of your cash is committed, and the higher your return on that cash.

It is equally important to think about ROI in annualized terms. A thirty percent return is excellent in four months and mediocre over two years. Since flips are short-term by design, the speed of the project is part of the return, which loops back to why holding costs and timelines deserve real attention.

How Taxes Work on a Flip

Taxes are the input investors most often overlook entirely, and they can meaningfully change whether a deal is worth doing. This is a general overview rather than tax advice, and you should consult a CPA familiar with real estate for your specific situation, but the broad strokes matter for planning.

The central point is that profit from a typical fix and flip is generally treated as ordinary income, not as a long-term capital gain. Investors who actively buy, renovate, and resell properties are frequently classified by the IRS as dealers, and the properties are treated as inventory rather than investment assets held for appreciation. That means the favorable long-term capital gains rates that apply to property held over a year generally do not apply to active flipping, because the intent is resale rather than holding.

On top of ordinary income tax, dealer income from flipping can be subject to self-employment tax, which adds a further layer many first-time flippers do not anticipate. The combined bite can be substantially higher than the capital gains rate investors often assume in their head. The practical takeaway is to model your profit on an after-tax basis. A deal that nets 50,000 dollars before taxes may net considerably less after ordinary income and self-employment taxes, and that after-tax figure is the one that actually matters for your life. Building a tax estimate into your analysis keeps you from celebrating a number you will not get to keep.

When the Flip Should Become a Rental

Sometimes the smartest move is to stop trying to flip. Markets shift, a property sits unsold, carrying costs mount, or you simply realize the property would cash flow beautifully as a rental. Pivoting from a flip to a hold, often called fix and rent, is one of the most powerful risk management tools an investor has, and the best investors evaluate it before they ever start.

The mechanism is a refinance into a DSCR loan. Once the renovation is complete and the property is rented, you refinance out of your short-term fix and flip loan into a long-term DSCR loan that qualifies based on the property's rental income rather than your personal income. Because the property is now renovated and worth its ARV, the refinance is typically based on that higher value, often letting you pull most or all of your invested capital back out while keeping the property. You convert a one-time gain into a cash-flowing asset and recover your cash to deploy on the next deal.

This pivot is what turns a single-exit gamble into a deal with a fallback. If the sale market is not cooperating, you are not forced to dump the property at a discount to escape your holding costs. You refinance, rent it, and wait for better conditions, collecting income the whole time. The discipline worth adopting is to underwrite both exits before you buy: confirm the deal works as a flip, and confirm it would still work as a rental refinanced with a DSCR loan. If only one exit works, you are exposed. If both work, you have built in protection that costs nothing until you need it.

A Quick Reference on the Key Inputs

The table below summarizes the core inputs and what each one tells you.

| Input | What It Means | Why It Matters |

|---|---|---|

| ARV | Projected value of the finished, renovated property | Sets the exit price and the basis for loan sizing |

| Scope of work | Itemized plan of all renovations | Drives the rehab budget and supports the ARV |

| Rehab budget plus contingency | Total renovation cost with a cushion for surprises | The largest controllable cost in the deal |

| LTC | Loan as a percentage of purchase plus rehab | Determines cash needed and ties the loan to actual cost |

| LTARV | Loan as a percentage of after repair value | Caps the loan against finished value; lender uses the lower of LTC and LTARV |

| Holding costs | Monthly interest, taxes, insurance, utilities | Accrues every month and makes time the enemy of profit |

| Selling costs | Commissions, transfer taxes, seller closing costs | Often high single digits of sale price; easily overlooked |

| ROI | Profit as a percentage of cash invested | The true measure of return; best viewed annualized |

| After-tax profit | Profit net of ordinary income and self-employment tax | The number you actually keep |

Closing Thoughts

A good fix and flip calculator is not about predicting the future perfectly. It is about stress-testing a deal before you risk capital on it. Run the numbers with a conservative ARV, a fully itemized rehab budget plus contingency, both leverage ratios, every holding and selling cost, an honest after-tax profit, and a second scenario where the property becomes a rental. If the deal still shows an acceptable return after all of that, you have a real opportunity. If it only works when you squint and assume everything goes right, the calculator has done its job by telling you to walk away.

The best flippers are not the most optimistic ones. They are the most disciplined, and disciplined math at the start is what protects everything that follows.

Join 25,000+ real estate investors

Our mission is to help you build wealth through real estate. OfferMarket membership is free and includes the following benefits:

OfferMarket Loans

Check your rate

60 seconds · no credit pull