*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Lender Terms Explained: Key Concepts for Real Estate Financing

Last Updated: jan 3, 2025

Navigating the world of real estate investment can be complex. Especially when it comes to understanding the financial aspects.

One key concept that often puzzles investors is DSCR. Short for Debt Service Coverage Ratio, it's a term frequently used by lenders.

But what does it mean? And why is it so important in real estate financing?

This article aims to demystify DSCR lender terms. We'll break down the complexities and explain how they apply to your investment strategies.

Whether you're an aspiring real estate investor or a seasoned agent, understanding DSCR is crucial. It can influence your investment decisions and the advice you give to clients.

We'll cover everything from how to calculate DSCR to its impact on loan terms and interest rates. We'll also delve into the requirements for DSCR loans and how they differ from traditional mortgages.

By the end of this article, you'll have a comprehensive understanding of DSCR lender terms. And you'll be better equipped to make informed decisions in your real estate ventures.

So, let's dive in and unravel the intricacies of DSCR in real estate financing.

Understanding DSCR in Real Estate Financing

The Debt Service Coverage Ratio (DSCR) is a vital metric in real estate. It helps evaluate a property's ability to generate enough income to cover its debt obligations. For aspiring investors and agents, grasping this concept is essential.

A strong DSCR indicates a safe investment. Investors and lenders use it to assess the likelihood that a borrower can cover future debt payments. Understanding DSCR can help you identify more lucrative investment properties.

Several factors contribute to the DSCR, which include:

- Net Operating Income (NOI)

- Total Debt Service (TDS)

- Monthly Revenue Streams

A higher DSCR reflects a healthier financial position, while a lower DSCR might indicate risk. Knowing how to evaluate these figures can empower your investment decisions.

In real estate, every point change in DSCR can impact your financing terms. It influences the interest rates and the overall loan structure that lenders offer.

For real estate agents, being able to articulate DSCR concepts to clients can enhance your advisory role. It equips you to better guide investors through financing choices and potential investments.

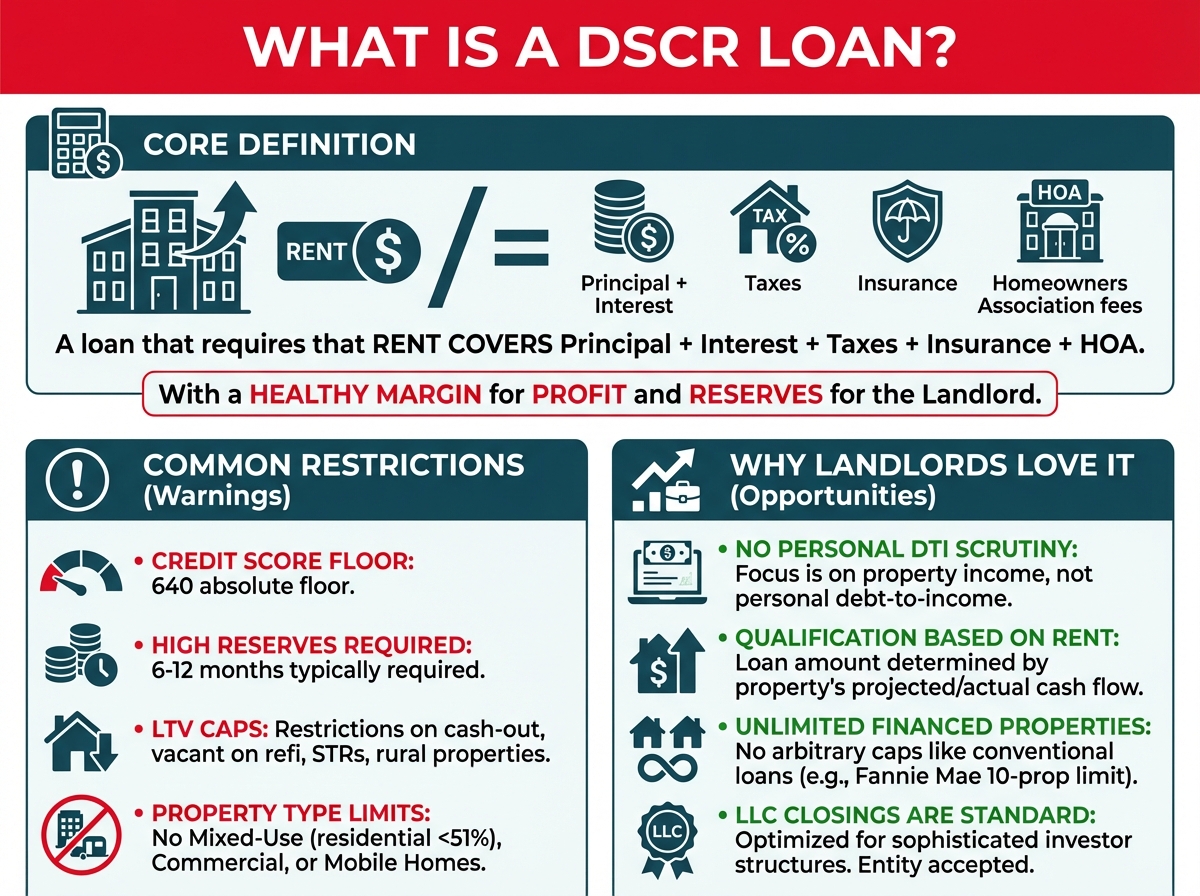

What is Debt Service Coverage Ratio (DSCR)?

DSCR is a financial ratio. It measures a property's cash flow to its debt obligations. Specifically, it evaluates if the property earns enough to pay its mortgage.

This ratio is vital for both lenders and investors. A DSCR above 1.0 means income surpasses debt obligations. This implies positive cash flow.

Lenders often require a minimum DSCR of 1.25. This buffer helps ensure coverage of unexpected financial shortfalls. Understanding DSCR helps you gauge an investment's financial health.

How to Calculate DSCR

To calculate DSCR, divide Net Operating Income (NOI) by Total Debt Service (TDS). The formula is:

DSCR = Net Operating Income (NOI) ÷ Total Debt Service (TDS)

NOI represents the property's revenue minus operating expenses. It excludes taxes and mortgage payments.

TDS includes all periodic debt payments, such as principal and interest. Calculating this gives you a view of how well a property handles its debt.

Knowing how to compute DSCR helps in understanding a property's financial viability. It aids in comparing investment opportunities and securing favorable loan terms.

The Importance of DSCR for Lenders and Investors

For lenders, DSCR serves as a risk assessment tool. It helps determine a borrower's ability to manage debt obligations. Higher DSCR values are more appealing to lenders, indicating lower risk.

Investors also rely on DSCR to evaluate properties. A strong DSCR can signal stable cash flow and manageable debt levels. This insight aids in making informed purchasing decisions.

A robust DSCR impacts negotiating power. Investors with higher DSCRs may secure better financing terms, reducing overall investment costs. Understanding DSCR is, therefore, key in optimizing your investment strategies.

DSCR Loan Requirements and Eligibility

DSCR loans are a popular choice for real estate investors. They offer flexibility and are tailored to properties that exhibit strong cash flow. However, they come with specific requirements that must be met.

Understanding the prerequisites is crucial for a successful application. These loans evaluate the property's ability to cover its debt more than the investor's income. Therefore, ensuring your property meets certain standards is vital.

Common DSCR loan requirements include:

- A minimum DSCR ratio (often 1.25 or above)

- Acceptable property types (usually income-producing real estate)

- A satisfactory credit score

- Detailed financial documentation of the property's income and expenses

Each lender may have unique requirements. It's essential to verify these specifics with your chosen DSCR lender. This ensures you meet their eligibility criteria.

Lenders assess the property's financials to ensure loan viability. The better you demonstrate financial stability, the easier it becomes to secure favorable loan terms. Adequate preparation helps you present a compelling case to lenders.

Minimum DSCR Ratios

Most DSCR lenders require a minimum DSCR ratio to mitigate risk. This ratio is generally set at 1.25 or higher. Such a threshold reassures lenders that the property generates enough income to cover its debt and unforeseen expenses.

A DSCR below the required minimum can signal higher risk. It suggests the property may struggle to fulfill debt commitments, leading lenders to hesitate. Meeting the minimum ratio is crucial for loan approval and favorable terms.

Lenders vary in their minimum DSCR requirements. Some may accept slightly lower ratios if other factors are favorable, like a high credit score or substantial down payment. Researching and choosing a lender with terms aligning with your financials can improve your loan chances.

Credit Score and Financial Documentation

A strong credit score enhances your DSCR loan application. While DSCR loans emphasize property income, lenders still consider personal financial responsibility. Typically, a score above 680 is favored, though requirements can differ among lenders.

Your credit history reflects your ability to manage debt. A solid score reassures lenders of your reliability. It can also positively influence the terms offered, like interest rates and repayment periods.

Additionally, detailed financial documentation is essential. This includes proof of the property's income, operating expenses, and existing debts. Accurate records allow lenders to gauge the property's profitability and manageability.

Thorough preparation before application is beneficial. By presenting clear financials and maintaining a strong credit record, you improve your chances of obtaining an advantageous DSCR loan.

The Impact of Loan-to-Value (LTV) on DSCR Loans

The Loan-to-Value (LTV) ratio is a significant factor in DSCR loan assessments. It reflects the amount of the loan compared to the property's value. This ratio helps lenders evaluate the risk associated with financing a specific property.

A lower LTV means the borrower is investing more capital upfront. This reduces the lender's risk and can lead to more favorable loan terms. Properties with strong LTV ratios often align with a stable DSCR, making them attractive to lenders.

High LTV ratios indicate higher risk. They suggest less borrower equity in the property, which may lead to stricter loan conditions. Lenders might demand higher interest rates or additional collateral in such situations.

Understanding LTV's relationship with DSCR loans is crucial for investors. It allows them to strategize effectively and make financial decisions that enhance their loan eligibility. Balancing these ratios can optimize borrowing potential.

Understanding LTV in Relation to DSCR

LTV is calculated by dividing the loan amount by the property's appraised value. A lower LTV indicates a more secure investment for lenders. This security parallels the assurance provided by a high DSCR, which ensures loan payments through steady income.

Both LTV and DSCR are vital in loan evaluations. They collectively offer lenders a comprehensive view of investment risk and repayment ability. Investors must appreciate this interplay to better meet lender expectations.

Strategies to Improve LTV for Better DSCR Terms

One effective way to improve LTV is by increasing your down payment. A larger down payment reduces the loan principal, lowering the LTV. This can make you more appealing to lenders and may result in better loan terms.

Another strategy is enhancing the property's value. Renovations or upgrades can boost appraised value, consequently improving LTV. With a stronger LTV and DSCR, borrowers are more likely to secure favorable financing conditions. Effective property management and strategic investments thus pay significant dividends.

Advantages and Risks of DSCR Loans

DSCR loans can be a powerful tool for real estate investors. They offer certain advantages that can enhance investment potential. However, understanding the associated risks is crucial for informed decision-making.

These loans primarily benefit investors with their flexibility. They often accommodate a variety of property types beyond the scope of traditional loans. This opens up broader investment opportunities.

Additionally, DSCR loans assess the property’s income potential rather than the borrower’s personal income. This can benefit investors with substantial property cash flow but inconsistent personal earnings. Such criteria can allow for greater leveraging of property portfolios.

Yet, there are inherent risks with DSCR loans. Market fluctuations can affect rental income, impacting DSCR and potentially leading to financing issues. Economic downturns or vacancies can expose investors to financial strain.

Regularly monitoring cash flow is key to risk mitigation. Investors should be prepared with contingency plans for periods of reduced income. A proactive approach can help navigate these uncertainties effectively.

Working with seasoned financial advisors is also recommended. Expert guidance can assist in structuring investments to minimize risks. Comprehensive strategies can help ensure sustainable growth and protect against market volatility.

Benefits for Real Estate Investors

DSCR loans offer key benefits tailored for real estate investors. These advantages can significantly aid in expanding and optimizing property portfolios.

Notably, they prioritize property income over personal credit. This focus allows investors with stable rental properties to secure financing even with less-than-perfect credit scores. This can be advantageous for expanding portfolios.

Another benefit is the potential for longer amortization periods. This can result in lower monthly payments and improved cash flow management. Enhanced liquidity allows investors to reinvest in additional properties.

Investors often appreciate the following benefits of DSCR loans:

- Reliance on property cash flow for qualification

- Flexibility in financing various types of investment properties

- Potential for favorable terms with strong DSCR and LTV ratios

Potential Risks and How to Mitigate Them

Below is a comprehensive table outlining the Potential Risks of DSCR Loans along with Mitigation Strategies to help investors safeguard their investments and maintain financial security.

| Potential Risk | Description | Mitigation Strategy | Details |

|---|---|---|---|

| Interest Rate Fluctuations | Changes in interest rates can increase loan payments, making them more burdensome and impacting cash flow. | Lock in Fixed Interest Rates | - Opt for long-term fixed-rate loans when possible. - Consider refinancing if rates are favorable. |

| Vacancies | A decrease in tenant occupancy reduces rental income, negatively affecting the Debt Service Coverage Ratio (DSCR). | Maintain Property Conditions | - Regularly maintain and improve properties. - Implement effective marketing strategies to attract and retain tenants. |

| Property Management Inefficiencies | Poor property management can lead to higher tenant turnover and increased maintenance costs, impacting revenue. | Employ Skilled Property Management Services | - Hire experienced property managers. - Implement efficient property management practices to ensure smooth operations. |

| Maintenance and Repair Costs | Unexpected maintenance or repair expenses can strain finances and reduce profitability. | Budget for Contingencies | - Allocate a reserve fund for unexpected expenses. - Conduct regular inspections to identify and address issues early. |

| Market Downturns | Economic downturns can lead to decreased property values and rental incomes, affecting loan repayment ability. | Diversify Investment Portfolio | - Invest in properties across different markets. - Diversify property types to spread risk. |

| Regulatory Changes | Changes in housing laws or regulations can impact rental income and property management practices. | Stay Informed and Compliant | - Keep abreast of local and national real estate regulations. - Adjust strategies to comply with new laws. |

| Tenant Defaults | Tenants failing to pay rent on time can disrupt cash flow and affect loan repayment. | Implement Rigorous Tenant Screening | - Conduct thorough background and credit checks. - Establish clear lease agreements and enforce them consistently. |

| Property Depreciation | Physical or functional deterioration of the property can reduce its market value and income potential. | Regular Property Upgrades and Maintenance | - Invest in regular upgrades and renovations. - Ensure properties are well-maintained to preserve value. |

| Economic Instability | Broader economic issues can affect overall rental markets and property values. | Flexible Financing Options | - Choose DSCR loans with flexible terms. - Maintain good relationships with multiple lenders to access various financing options if needed. |

| Natural Disasters | Events like floods, earthquakes, or hurricanes can cause significant property damage and financial loss. | Obtain Comprehensive Insurance | - Secure adequate insurance coverage for natural disasters. - Implement risk management plans to minimize damage. |

How to Find and Negotiate with DSCR Lenders

Finding the right DSCR lender is crucial for securing the best financing terms. Research is the foundation for identifying lenders who understand your investment goals. Start by exploring local and national lenders specializing in real estate investments. This can provide a broad perspective on available options.

Networking within real estate communities can also offer valuable insights. Experienced investors often share recommendations and personal experiences. Attending seminars and joining investment groups can expand your understanding and connections. Building relationships with professionals might lead to introductions to reputable lenders.

It's important to assess the lender's experience with DSCR loans specifically. A lender's track record with similar financing deals can be telling. Ensure they can accommodate your property's unique characteristics and investment objectives. Transparent communication with lenders about your needs can foster a strong partnership.

Once you've identified potential lenders, comparing their terms is essential. Examine interest rates, fees, and loan-to-value ratios. Understanding these factors will help you choose a lender whose terms align with your financial strategy. Comprehensive evaluation is key to making an informed decision.

Finally, negotiation plays a critical role in securing favorable terms. Strengthening your negotiating position can significantly impact the loan's long-term benefits. Prepare thoroughly by understanding industry standards and your property's financial metrics. Confidence and clarity during negotiations can influence outcomes positively.

Identifying Reputable DSCR Lenders

When searching for reputable DSCR lenders, prioritize lenders with a solid history in real estate financing. Look for those who actively participate in industry associations, as this often indicates professionalism. Review customer testimonials and case studies from their past clients for insights into their service quality.

Lenders with specialization in DSCR loans are preferable due to their targeted expertise. Such specialization often results in a smoother and more informed loan process. Ask potential lenders about their experience with properties similar to yours.

Additionally, check if the lender offers transparency in their dealings. It's vital they communicate clearly about all terms and conditions. Openness and straightforward communication suggest reliability. Transparency helps build trust, an essential factor for a long-term financial relationship.

Negotiating Favorable Lender Terms

To negotiate favorable DSCR lender terms, preparation is key. Start by understanding your property's financial strengths and market position. A clear presentation of high DSCR values and stable cash flow can strengthen your case. Highlighting these can lead to more competitive loan offers.

Approach the negotiation with a clear understanding of market conditions and standard lending terms. Knowledge about typical interest rates and fees provides leverage. It enables you to push for adjustments if the initial terms are less favorable.

During negotiations, maintain flexibility but be clear about your expectations. Propose alternatives if the initial offers don’t meet your criteria. Sometimes, adjusting the loan structure, such as suggesting a longer amortization period, can lead to mutually beneficial terms.

Being prepared and informed helps facilitate negotiations that align closely with your investment goals.

Conclusion: Leveraging DSCR Loans for Real Estate Success

Understanding DSCR lender terms is essential for real estate financing success. These loans offer strategic benefits, particularly for rental property investments. By focusing on cash flow and property management, investors can unlock favorable terms.

Effective DSCR loan use involves thorough preparation and analysis. Investors and agents must stay informed about market conditions and lender criteria. By doing so, they can better navigate the complexities of real estate financing.

Key Takeaways for Aspiring Investors and Real Estate Agents

Aspiring investors should prioritize mastering DSCR concepts to enhance their investment decisions. A solid DSCR can boost loan eligibility and terms, aiding portfolio growth. Real estate agents can use this knowledge to guide clients towards smarter financing options.

Understanding DSCR's role in assessing property risks and opportunities is crucial. By leveraging this ratio, both investors and agents can make more informed and strategic real estate decisions. This focus on DSCR provides a foundation for long-term success in real estate investing.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull