*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Loan Minimum Amounts: Everything You Need To Know

Navigating the world of real estate investment can be complex. One term you may encounter is DSCR loan.

But what exactly is a DSCR loan?

DSCR stands for Debt Service Coverage Ratio. It's a type of loan used in real estate investment, particularly for rental properties.

Understanding the specifics of DSCR loans, especially the minimum loan amounts, can be a game-changer for investors. It can help you make informed decisions and maximize your investment returns.

In this blog post we will delve into the nuances of DSCR loan minimum amounts, requirements, and how they can be leveraged for rental property investments.

Whether you're an aspiring investor, a real estate agent, or a property manager in Texas, this comprehensive guide will equip you with the knowledge you need to navigate DSCR loans effectively.

Understanding DSCR Loans

DSCR loans are a crucial component of real estate financing. They focus on a property's cash flow. This approach is different from conventional loans that emphasize personal income.

These loans assess whether a property's income can cover debt payments. This focus makes them appealing to investors with multiple properties.

Key elements of DSCR loans include:

- Debt Service Coverage Ratio (DSCR)

- Rental income potential

- Property type and location

Understanding these elements is essential for maximizing loan benefits. DSCR calculations determine loan eligibility. A higher ratio indicates better loan prospects.

Lenders prefer a DSCR above 1.2. This ratio shows that income exceeds debt obligations. It's a critical factor in securing financing.

By mastering DSCR loans, investors can enhance their portfolios. They become better equipped to identify profitable opportunities. This knowledge leads to more strategic investment decisions.

What is a DSCR Loan?

A DSCR loan is a type of financing used in real estate investments. It relies on the Debt Service Coverage Ratio. This ratio is crucial in assessing the property's income versus its debt obligations.

This type of loan benefits property investors. It evaluates the property's cash flow rather than the borrower's personal income. This shift allows for increased flexibility and wider access to financing.

Real estate investors often choose DSCR loans. They're ideal for purchasing rental properties. This approach focuses on the property's ability to generate enough income to cover its debts.

How is DSCR Calculated?

Calculating the DSCR is straightforward. The formula divides the net operating income by the total debt service. This calculation provides a clear picture of the property's financial health.

Net operating income includes rental income after expenses. It reflects the cash flow available to service debt. This figure is the numerator in the DSCR formula.

Total debt service includes principal and interest payments. This number is the denominator in the DSCR equation. It represents the total obligations owed by the property.

For example, if a property earns $120,000 and has debt payments of $100,000, the DSCR is 1.2. This ratio indicates a property's income covers its debt by 20%.

Knowing the DSCR helps investors assess loan eligibility. A DSCR above 1 often meets lenders' requirements for approval.

The Role of DSCR in Real Estate Investment

The DSCR plays a vital role in real estate investment. It helps assess the property's financial performance. The ratio directly impacts loan eligibility.

Investors benefit from a strong DSCR. It signals healthy cash flow relative to debt commitments. This financial health increases attractiveness to lenders.

A solid DSCR can unlock better financing terms. Investors can secure loans with favorable conditions. This benefit helps optimize investment returns over time.

DSCR Loan Minimum Loan Amounts

Understanding the minimum loan amounts for DSCR loans is crucial. These amounts vary but generally cater to substantial property investments. Minimums often start around $100,000, sometimes reaching into the millions.

This variance is due to lenders' different policies and borrower profiles. Lenders assess the property's income and market conditions. The location also has a significant impact on loan amounts.

In high-demand areas, minimums tend to be higher. Locations with strong rental markets can require larger loan commitments. This difference influences how investors plan their financing strategies.

Property type is another determining factor. Commercial properties often lead to larger loan requirements. Residential investments may see smaller minimums under DSCR terms.

The investor's financial health and experience also play roles. Lenders look at credit scores and investment portfolios. This information informs their risk assessment, impacting loan offerings.

Lenders typically prioritize properties with strong earning potential. They view these as lower-risk investments. This focus makes DSCR loans ideal for cash-flow-positive properties.

The minimum loan amount should align with investment goals. It must support the acquisition costs and potential improvements. Properly aligning these aspects ensures financial stability.

Understanding these loan amounts helps in informed decision-making. Investors need to consider both immediate needs and long-term benefits. This consideration is vital for strategic growth and success.

Factors Affecting Minimum Loan Amounts

Several key factors influence the minimum loan amounts for DSCR loans. These elements help lenders determine risk and profitability. Understanding them can guide better investment choices.

Critical factors include:

- Property location and market demand

- Property type, such as residential or commercial

- Investor creditworthiness and financial history

Location is crucial. High-demand areas often lead to higher minimums. Properties in burgeoning markets promise steady income, reducing lender risk.

Property type significantly impacts loan amounts. Commercial spaces typically require larger loans. These properties often hold higher values and potential returns.

Lender policies also affect minimums. Each lender has unique requirements and risk tolerance. They set thresholds based on internal assessments and market conditions.

Investor creditworthiness plays a role too. Strong credit histories can lead to more favorable terms. A solid financial profile assures lenders of repayment capability.

Market trends influence lender decisions. Economic factors shift lender confidence, altering minimum loans. Staying informed allows investors to adjust strategies effectively.

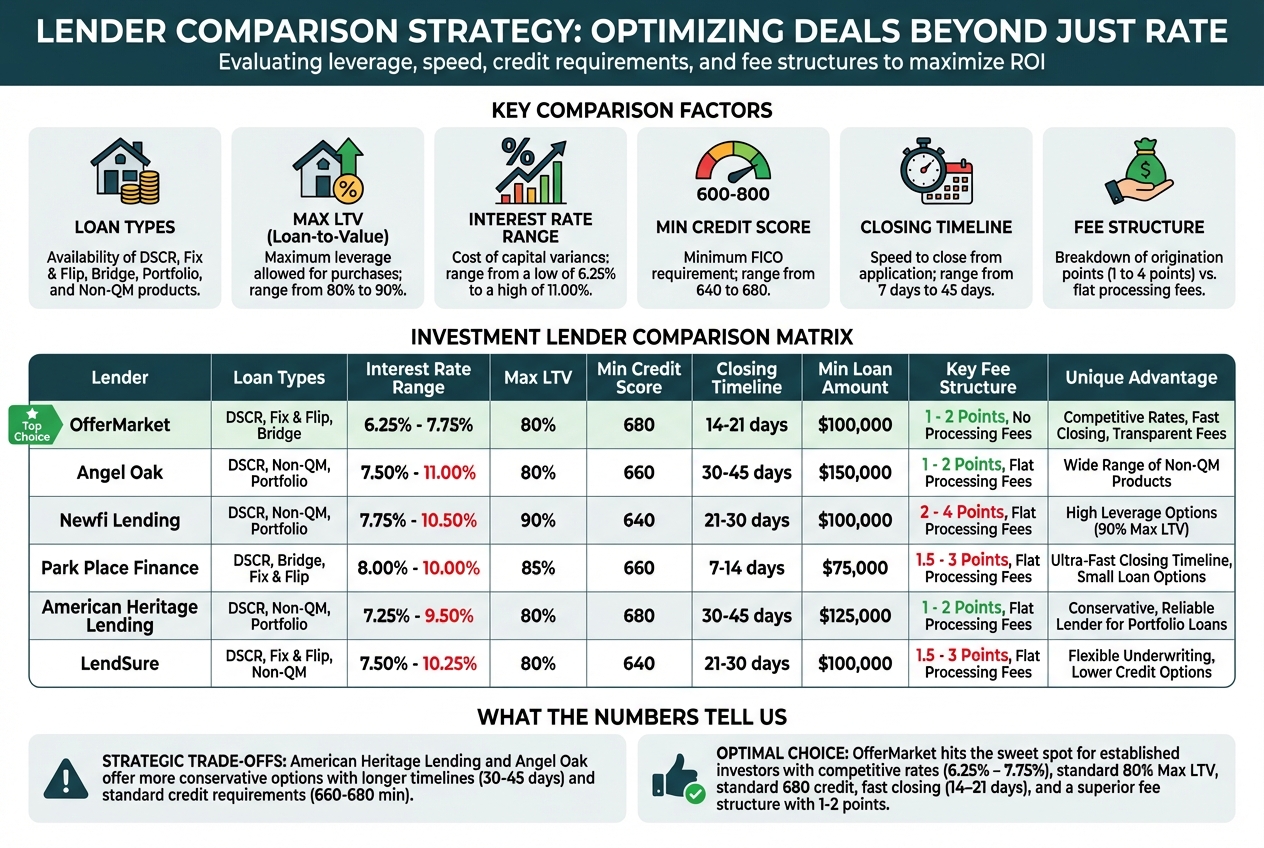

Comparing Lenders: Minimum Amount Variations

Lenders vary widely in their minimum loan requirements. These differences arise from distinct risk strategies. Comparing these lenders helps find the best fit for investment needs.

Some lenders cater to large-scale investments. They require higher minimum loan amounts. This approach suits investors targeting high-value properties or commercial spaces.

Others focus on smaller-scale investments. They offer more accessible minimums for residential properties. This flexibility attracts newer investors or those with varied portfolios.

Research is key in comparing lender terms. Evaluating options ensures alignment with investment goals. It helps in securing favorable terms and optimizing cash flow.

Engage with lenders directly. This step clarifies their specific criteria and options. Open communication helps in navigating the approval process effectively.

Remember, lender policies change over time. Regularly review terms and conditions to stay updated. This diligence is necessary to capitalize on new opportunities as they arise.

DSCR Loan Requirements

To qualify for a DSCR loan, investors need to meet specific requirements. These criteria ensure that both the investor and property are viable. Lenders assess multiple factors to gauge risk and repayment capability.

Key requirements typically include:

- Sufficient DSCR ratio

- Adequate credit score

- Necessary down payment and acceptable LTV (Loan-to-Value) ratios

A sufficient DSCR ratio is fundamental. Lenders seek assurance that property income exceeds debt obligations. This ratio varies but usually needs to be above 1.25.

Credit scores are another crucial aspect. Strong scores enhance eligibility and terms. They reflect financial responsibility and reduce perceived risk.

Down payments and LTV ratios also play significant roles. A substantial down payment lowers lender risk. Acceptable LTV ratios enhance loan approval chances.

Rental income and property type determine loan capacity. Properties generating stable income are attractive. The property type influences the loan's size and requirements.

Meeting these requirements secures better terms. It minimizes interest costs and maximizes investment returns. Aligning with lender criteria is thus key in obtaining DSCR loan approval.

Credit Score Considerations

Credit scores significantly impact DSCR loan eligibility. Lenders use these scores to assess borrower risk. Typically, a score above 680 is preferred for DSCR loans.

Higher credit scores can lead to better terms. They might result in lower interest rates and higher loan amounts. This benefit reduces overall loan costs.

Maintaining or improving your credit score is critical. Pay bills on time and reduce outstanding debts. Proactive financial management enhances your loan prospects.

Down Payment and LTV Ratios

Down payments influence DSCR loan terms. Larger down payments often secure better interest rates. They reassure lenders about the investor’s financial commitment.

LTV ratios are equally important. Lenders compare the loan amount to property value. A lower LTV indicates less risk, favoring loan approval.

Typically, DSCR loans require LTV ratios below 80%. This threshold varies by lender, but lower is generally better. Favorable ratios demonstrate investment stability.

Beyond just approval, LTV affects loan terms. Lower ratios often lead to lower costs. They translate into decreased monthly payments.

Investors should aim to optimize both down payments and LTVs. This strategy improves both approval odds and investment yield. Balancing these factors is integral for securing favorable loans.

Rental Income and Property Type

Rental income plays a pivotal role in DSCR loans. It forms the primary source for debt repayment. Lenders expect income to comfortably cover loan obligations.

Reliable rental income decreases lender risk. Properties with consistent tenants are especially favorable. This consistency reassures lenders about investment viability.

Property type greatly affects loan considerations. Commercial properties usually have different income expectations. They might also entail more stringent requirements.

Residential investments usually focus on tenant stability. Securing leases with creditworthy tenants boosts appeal. This assurance lowers lender risk perception.

Selecting the right property type aligns with income goals. Investors should evaluate market demand and property characteristics. This analysis optimizes income potential and investment success.

Advantages and Challenges of DSCR Loans

DSCR loans offer compelling advantages for real estate investors. They primarily allow access to funds based on property income. This focus on income rather than personal finances is beneficial.

One significant advantage is flexibility. Investors with multiple properties can benefit from streamlined financing. It reduces the complexity of managing various loans.

Another benefit is the potential for higher loan amounts. Since approval hinges on property income, successful properties can secure larger funds. This increase supports ambitious investment plans.

Despite these perks, challenges exist. Interest rates on DSCR loans may be higher than traditional options. This difference affects the overall cost of financing.

Lenders also impose strict requirements on DSCR ratios and rental income. Meeting these parameters can be demanding. Investors must present thorough documentation to qualify.

Understanding both advantages and challenges is essential. This knowledge helps investors weigh DSCR loans against other financing types. Making informed decisions ensures they align with long-term investment goals.

Pros and Cons for Investors

DSCR loans are advantageous for investors targeting rental properties. One primary benefit is income-based qualification. This criterion suits investors focused on property potential rather than personal financial status.

These loans also offer flexibility. Investors can maintain cash flow and handle multiple properties effectively. Such flexibility supports portfolio expansion and diversification.

However, there are drawbacks. Interest rates can be higher compared to conventional loans. This difference may affect profit margins and long-term cost.

Moreover, DSCR loans have strict requirements for debt coverage ratios. They demand consistent rental income and well-maintained properties. Meeting these conditions requires diligent property management.

Investors should consider both sides of DSCR loans. Balancing benefits against costs ensures they make strategic financing choices. An informed approach can maximize investment returns.

DSCR vs. Traditional Mortgage Financing

Below is a table summarizing the key differences between DSCR and traditional mortgage financing, incorporating common distinctions highlighted by industry sources:

DSCR Loans in Texas: A Market Overview

Texas presents unique opportunities for those using DSCR loans. The state's growing population stimulates rental demand. This growth is fueled by strong economic performance and a high quality of life.

In recent years, cities like Boise and Meridian have seen significant appreciation in property values. This creates a favorable environment for investors aiming to build equity. Moreover, rental markets in these areas are robust, offering reliable cash flows.

The regulatory climate in Texas is also conducive to real estate investment. Landlord-friendly laws make property management more straightforward. This aspect attracts investors interested in maintaining profitable operations.

Additionally, Texas' economic sectors, such as technology and agriculture, continue to expand. This expansion supports a thriving rental market with diverse tenant demographics. This economic backdrop reinforces the potential for sustained rental income and property appreciation.

Understanding these dynamics is crucial for leveraging DSCR loans in Texas. Investing in the right locations at the right time can yield substantial returns. Successful investors in Texas use market insights to guide their DSCR loan strategies.

Understanding The Texas Rental Property Market

Texas rental market is characterized by steady demand. Cities like Boise have seen inflows of new residents. This population growth boosts rental housing needs.

Affordability remains attractive compared to other states. This affordability draws both tenants and investors alike. The cost-to-rent ratio supports healthy occupancy rates.

Seasonal variations play a role in this market. Understanding these can help in timing investments. Keeping an eye on trends ensures strategic decision-making.

Case Studies: Successful Texas Investments with DSCR Loans

An example of success is a small multi-family property in Boise. The investor utilized a DSCR loan to refinance. The improved cash flow led to further property upgrades.

Another successful case involved a commercial mixed-use property. The investor enhanced its appeal with new amenities. The property's increased value facilitated a profitable sale.

These examples underscore the strategic use of DSCR loans. Leveraging these loans with smart enhancements can yield high returns. Observing such successes helps guide future investment choices.

Conclusion and Key Takeaways

Understanding DSCR loans can transform your investment approach. They offer a unique path for financing rental properties. The flexibility provided by DSCR loans suits both new and seasoned investors.

Key factors include knowing minimum loan amounts and lender variations. These details impact your investment choices and long-term strategy. Thorough market analysis is essential for leveraging these loans effectively.

In T, the dynamic property market presents opportunities. Utilizing DSCR loans here requires familiarity with local trends. By understanding these nuances, you can maximize returns and minimize risks.

Armed with this knowledge, you can approach DSCR loans confidently. Whether for building or diversifying your portfolio, informed decisions are vital. Keep exploring, stay updated, and let informed strategies guide your investments.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull