*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Cash flow calculator

Last updated: March 29, 2025

Cash flow is vital for your business because it covers payroll loan payments and other obligations. Without enough on hand you risk missing critical expenses that could jeopardize daily operations.

A cash flow calculator helps you predict inflows and outflows so you can plan ahead with confidence. For example if your inflows total 150000 and outflows are 100000 your net cash flow is 50000. That number reveals whether you can meet short-term obligations or pursue growth opportunities. Watching these figures closely lets you manage finances more effectively and keep your future secure.

What is Cash Flow Calculator?

A cash flow calculator is a tool that estimates net monthly or annual cash flow for your business or real estate investments. It factors in income, expenses, financing considerations, and potential vacancies. This process reveals break-even points and risk thresholds. You can compare multiple properties if you're analyzing rental opportunities, or explore refinancing options if you're evaluating financing changes.

A simple calculation involves subtracting total outflows by total inflows. If a company had $150,000 cash inflow and $100,000 cash outflow, the net flow would be $50,000. Tracking these figures helps you manage ongoing operations and align your spending with reliable cash inflows. This awareness can guide your decisions when projecting future performance.

Purpose

The purpose of a cash flow calculator is to provide investors with a clear understanding of their financial landscape before making significant investment decisions. By predicting profitability prior to purchasing a property, investors can avoid costly mistakes and ensure that their investments align with their financial goals. This tool allows for the identification of "break-even" points, which are crucial for understanding the minimum performance required to cover costs.

Additionally, it helps establish risk thresholds, enabling investors to gauge how much risk they are willing to take on based on their financial situation. By analyzing these factors, investors can make informed decisions that enhance their chances of success in the competitive real estate market. Ultimately, a cash flow calculator serves as a vital resource for strategic planning, allowing investors to visualize potential outcomes and adjust their strategies accordingly.

When to Use It

A cash flow calculator is particularly useful in various scenarios, especially when analyzing rental properties, whether for long-term leases or short-term vacation rentals. It provides insights into expected income and expenses, helping investors determine the viability of a property.

Additionally, it is beneficial when assessing the impact of financing changes, such as refinancing existing loans. By inputting new interest rates and terms, investors can see how these changes affect their cash flow and overall profitability. Furthermore, the calculator is invaluable for comparing multiple investment opportunities. By evaluating different properties side by side, investors can identify which options offer the best potential returns and align with their investment strategies. This comprehensive analysis empowers investors to make data-driven decisions that maximize their financial outcomes.

How to Calculate Cash Flow

Gross Income

Calculate gross income by adding rent and other income (laundry, parking, fees). Include every income source, for example a property with rent at $1,200 plus $50 from parking for a total of $1,250. Use this combined figure for the starting point in estimating your monthly or annual cash flow.

Total Expenses

Sum fixed costs (mortgage, property taxes, insurance), then add variable items like maintenance (5–10% of rent), vacancies (5–8%), and property management (8–12%). Factor each expense separately, for example if $1,200 rent is collected and maintenance is 5% of that rent, the maintenance expense equals $60. Combine all expenses to arrive at your total outflow.

Net Cash Flow

Subtract total expenses from gross income to see net cash flow. If gross income is $150,000 and total expenses are $100,000, the resulting net flow is $50,000. Track this figure over time to ensure that your inflows consistently exceed your outflows.

Automated Calculation Tools

Gather inputs such as purchase price, loan terms, rent, and expense ratios. Enter each figure into the calculator. Observe outputs like monthly cash flow, annual net income, and cash-on-cash return, which reflect how effectively the cash flow calculator forecasts your financial performance.

Why Cash Flow Analysis Matters

Benefits

Risk Mitigation

Cash flow analysis plays a crucial role in risk mitigation by revealing negative cash flow risks early in the investment process. By understanding the inflow and outflow of cash, investors can identify potential financial pitfalls before they escalate. This proactive approach allows for timely adjustments to investment strategies, ensuring that investors are not caught off guard by unexpected expenses or lower-than-expected rental income. By pinpointing break-even points, investors can make informed decisions about pricing and occupancy rates, ultimately safeguarding their investments.

Financing Optimization

Another significant benefit of cash flow analysis is financing optimization. By testing different loan terms, such as 15-year versus 30-year mortgages, investors can see how these variations impact their profits. This analysis allows for a comparison of monthly payments and interest rates, helping investors choose the most advantageous financing options. Understanding how different financing structures affect cash flow enables investors to make strategic decisions that enhance their overall profitability and financial stability.

Scalability Planning

Cash flow analysis also aids in scalability planning by projecting how many properties an investor can afford based on available free cash and estimated carrying costs. This insight is invaluable for those looking to expand their real estate portfolio. By assessing current cash flow and potential future income, investors can determine the feasibility of acquiring additional properties, ensuring that their growth is sustainable and aligned with their financial goals.

Limitations

Assumption-Dependent

Despite its benefits, cash flow analysis has limitations, primarily its assumption-dependent nature. The accuracy of the analysis hinges on realistic expense estimates. Underestimating costs such as maintenance, repairs, or vacancy rates can skew the outcome, leading to misguided investment decisions. Therefore, it is essential for investors to conduct thorough research and use conservative estimates to ensure reliable results.

Ignores Appreciation/Equity

Additionally, cash flow analysis focuses solely on income and expenses, often ignoring property appreciation and equity gains that may impact long-term wealth. While understanding cash flow is vital for short-term financial health, it does not provide a complete picture of an investment's potential for growth over time. Investors should complement cash flow analysis with other metrics that account for property value appreciation to gain a comprehensive understanding of their investment's long-term viability.

Cash Flow vs. Other Metrics

Cash Flow vs. Profit

Profit includes equity paydown and appreciation. It reflects gains in property value or reductions in principal that build long-term wealth.

Cash Flow is liquid income after bills. It shows the immediate funds that support your day-to-day operations and monthly obligations.

Cash Flow vs. NOI (Net Operating Income)

NOI = Gross Income – Operating Expenses (without financing costs). It accounts for rent and additional charges minus items like maintenance, insurance, and taxes.

Cash Flow = NOI – Debt Service. It factors in loan payments so you see the remaining funds each reporting cycle. If your NOI is 50,000 dollars and your annual debt service is 40,000 dollars, your cash flow is 10,000 dollars.

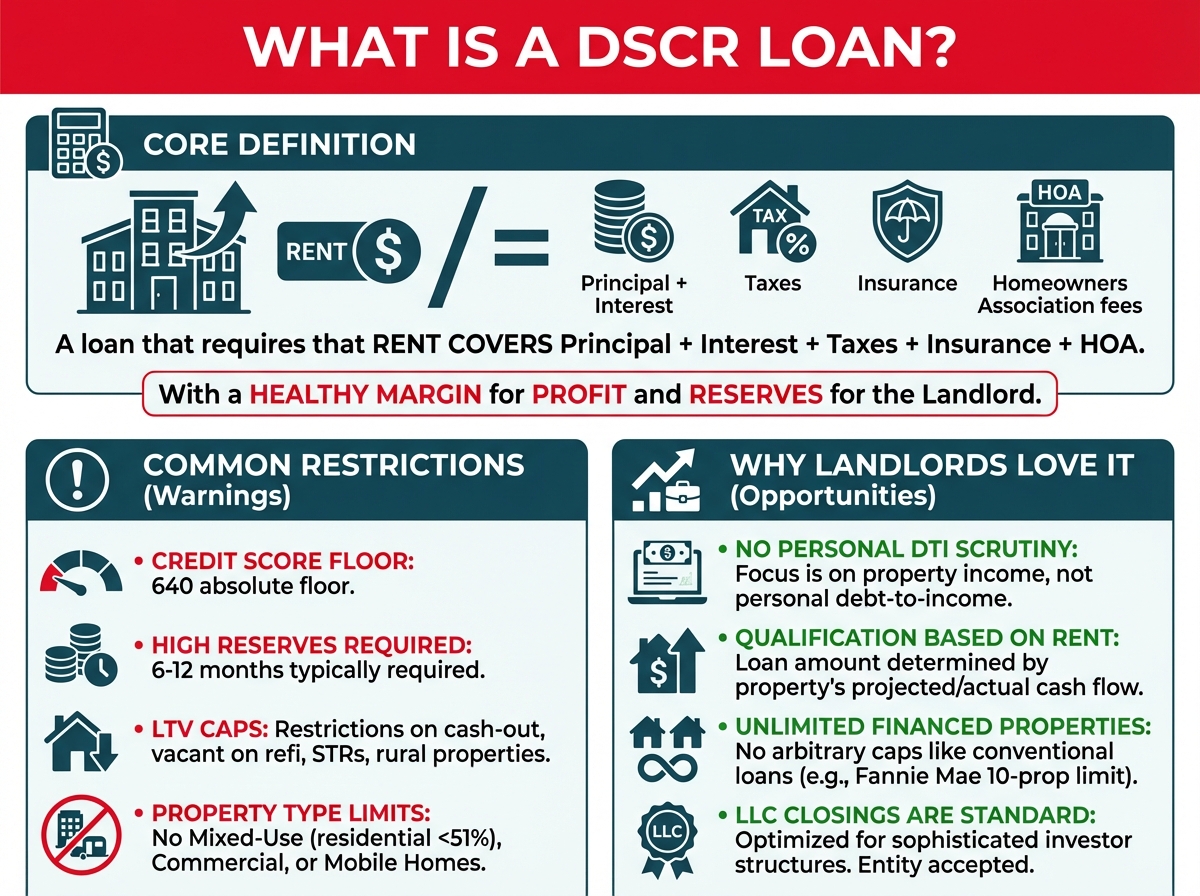

Cash Flow vs. DSCR (Debt Service Coverage Ratio)

DSCR = NOI / Debt Service. Lenders compare these values to identify repayment capacity. A DSCR above 1.20 is common in commercial lending.

Cash Flow is the actual dollars left in your pocket. It confirms how much you can place back into your cash flow calculator each period.

Types of Cash Flow Calculations

Operating Cash Flow (OCF) measures net cash from regular operations. It's calculated by adding net income and non-cash expenses, then subtracting any changes in working capital. For example, if your net income is 250,000, your non-cash expenses are 100,000, and your working capital change is 50,000, your OCF is 300,000.

Cash Flow from Investing (CFI) tracks the net amounts from buying or selling property, other businesses, or marketable securities. If your property purchases total 50,000, your acquisitions for other businesses total 75,000, and your marketable securities activity totals 25,000, your CFI is 150,000.

Cash Flow from Financing (CFF) records inflows from debt or equity issuances minus outflows such as dividends or debt repayments. If your equity inflows are 150,000, your dividends paid are 20,000, and your repurchase of debt is 50,000, your CFF is 80,000.

Rental Property Calculations often include long-term monthly rent and short-term rent with seasonal adjustments. Assess net income after subtracting expenses like mortgage, maintenance, and potential vacancies. If a short-term rental experiences a 20% dip in occupancy during off-season months, your rent revenue decreases proportionately.

Commercial Real Estate Calculations commonly compare triple net (NNN) leases, where tenants cover expenses, to gross leases, where owners pay for taxes and insurance. Estimate cash flow by reviewing the lease type and factoring in property management costs.

Fix-and-Flip Calculations involve a holding period that can generate rent if you lease the property during rehab. Track incoming rent against rehab costs to see if the project creates positive cash flow before selling.

Key Factors Affecting Cash Flow

| Factor | Data/Recommendation |

|---|---|

| Rent Prices | Based on market comparables |

| Occupancy Rates | 90–95% for stable markets |

| Maintenance | 1–2% of property value per year |

| Property Taxes | Vary by location (Texas vs. California) |

| Interest Rates | Higher rates = lower cash flow |

| Down Payment | Larger down payments improve cash flow |

Income variables, such as rent prices and occupancy rates, influence your gross inflow. Rent prices often follow local market comparables, and occupancy rates often hover between 90–95% in stable areas. Tracking these figures helps forecast consistent monthly income for business or property expenses.

Expense variables, like maintenance and property taxes, affect net inflow. Maintenance costs can represent 1–2% of a property's value annually. Property taxes shift based on location and can add significant recurring expenses.

Financing variables, including interest rates and down payments, further impact monthly cash figures. Higher interest rates reduce your monthly surplus by increasing financing costs. Larger down payments lessen ongoing loan obligations, resulting in stronger cash flow performance.

Pros and Cons of Cash Flow Investing

Advantages

Passive Income

You generate steady monthly income by collecting rent from investment properties. You may see 90–95% occupancy rates in stable markets, though actual numbers vary by location. You can reference cash flow return on investment (CFROI) percentages to track ongoing gains or losses.

Inflation Hedge

You often see rental income track rising expenses during inflationary periods. You bolster cash flow by adjusting rents to match cost-of-living increases. You may offset mortgage costs if loan terms remain fixed.

Disadvantages

High Initial Costs

You face large down payments and capital expenditure (CapEx) reserves. You encounter additional repair expenses after purchase. You also see higher loan expenses if interest rates rise, which reduces your monthly net flow.

Management Intensive

You invest time addressing tenant issues and property upkeep. You respond to maintenance emergencies, such as plumbing leaks or electrical problems. You may outsource tasks, though that adds third-party costs.

How to Improve Cash Flow

Increase Income

Rent Adjustments: Add amenities (storage, pets)

Adding storage units or pet-friendly policies can raise monthly rent by 3–5%. These adjustments often appeal to renters seeking convenience, which boosts occupancy and increases overall returns.

Auxiliary Income: Laundry, parking fees

Providing on-site laundry can generate $30–$50 per unit each month. Charging parking fees of $40–$60 per space further supplements your rental income and strengthens your cash flow.

Reduce Expenses

Refinance: Lower interest rates

Reducing your interest rate from 6.0% to 4.5% can lower monthly payments by about 15%. This creates additional liquidity for daily operations, especially for long-term loan durations.

DIY Management: Self-manage vs. hire a company

Self-managing can cut monthly management costs by 6–10% of your collected rent. It involves direct oversight of maintenance and tenant relations, which helps keep more revenue in your pocket.

Tax Strategies

Depreciation: Offsets taxable income

Claiming depreciation on real estate assets reduces taxable income, which frees cash for reinvestment. This non-cash expense aligns with standard accounting practices and lowers immediate tax liabilities.

Cost Segregation: Accelerated depreciation

Separating building components into shorter depreciation schedules accelerates tax benefits. This defers a portion of tax payments, making more funds available for ongoing expenses or expanding your portfolio.

Common Cash Flow Mistakes

Underestimating Expenses

Many calculations overlook day-to-day costs. Unexpected repairs and routine upkeep, including plumbing and electrical fixes, often exceed early estimates. It's crucial to consider capex for roofs and HVAC replacements, if the property faces aging infrastructure. The total bill can reach thousands of dollars and disrupt projected cash flow.

Overleveraging

Financing too much property debt squeezes monthly margins. Large loan balances lead to higher mortgage payments, which create negative cash flow if vacancies rise above 10%. According to rental market data, an occupancy drop from 95% to 85% can reduce income drastically and strain repayment schedules.

Ignoring Market Cycles

Purchasing real estate at peak pricing with low rent yields stifles returns. Rental values may remain stagnant, if local demand softens. Overpaying when interest rates are fluctuating limits flexibility and lowers future cash flow potential. Market data from regional housing reports shows that peak-season acquisitions often yield smaller net returns than off-season deals.

Advanced Cash Flow Strategies

Sensitivity Analysis

Sensitivity Analysis models worst-case scenarios to gauge the impact of fluctuations on net cash flow. A 20% vacancy rate reduces revenue on a property with a projected monthly rent of $2,000 to $1,600. That shift affects monthly obligations like debt service and maintenance costs. Factoring capital expenditures of $150,000 from investing activities introduces more clarity on long-term budget allocations. Identifying these breakpoints helps guide financing decisions and contingency plans.

Portfolio Diversification

Portfolio Diversification balances risk and potential returns by allocating funds to both high-cash-flow properties, like those found in certain Midwest cities, and high-growth markets, like coastal regions, to capture appreciation. Examining multiple assets at once highlights variations in rent structure, tax obligations, and maintenance expenses. Tracking free cash across these segments focuses resources on reliable sectors, especially when local market cycles slow down.

BRRRR Method

BRRRR Method calculates cash flow after refinancing to measure the effectiveness of recycled capital from property renovations. A fully leased property with updates that cost $50,000 can improve fair market rents, which can increase post-refinance cash flow. Accounting for reduced principal balances after the cash-out refinance reveals leftover funds for next acquisitions. Projections in a BRRRR analysis reflect the resulting cash surplus or shortfall after debt service.

Frequently Asked Questions (FAQs)

What’s a Good Monthly Cash Flow per Property?

A good monthly cash flow per property ranges from $200 to $500 or more after expenses. This amount varies by location and property type. Investors should aim for positive cash flow to cover expenses and provide a buffer for unexpected costs, ensuring financial health and investment sustainability.

Can Cash Flow Be Negative?

Cash flow can be negative, especially in high-cost-of-living areas or overleveraged deals, when expenses exceed income. This is common among new investors who may overlook costs. Understanding the risk of negative cash flow is essential for making informed decisions and developing effective risk mitigation strategies.

How Accurate Are Cash Flow Calculators?

Cash flow calculators offer accuracy of ±10–15% with realistic inputs. Their effectiveness depends on quality data for income and expenses. Regular updates enhance reliability, aiding financial planning. These tools help track finances, evaluate funding options, and identify potential issues, empowering investors to make informed decisions and refine their portfolios.

Grow your real estate portfolio with OfferMarket

OfferMarket is a real estate investing platform. Month-in-month-out, thousands of real estate professionals leverage our platform to grow and optimize their business. Our mission is to help you build wealth through real estate and we offer the following benefits to our members:

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights