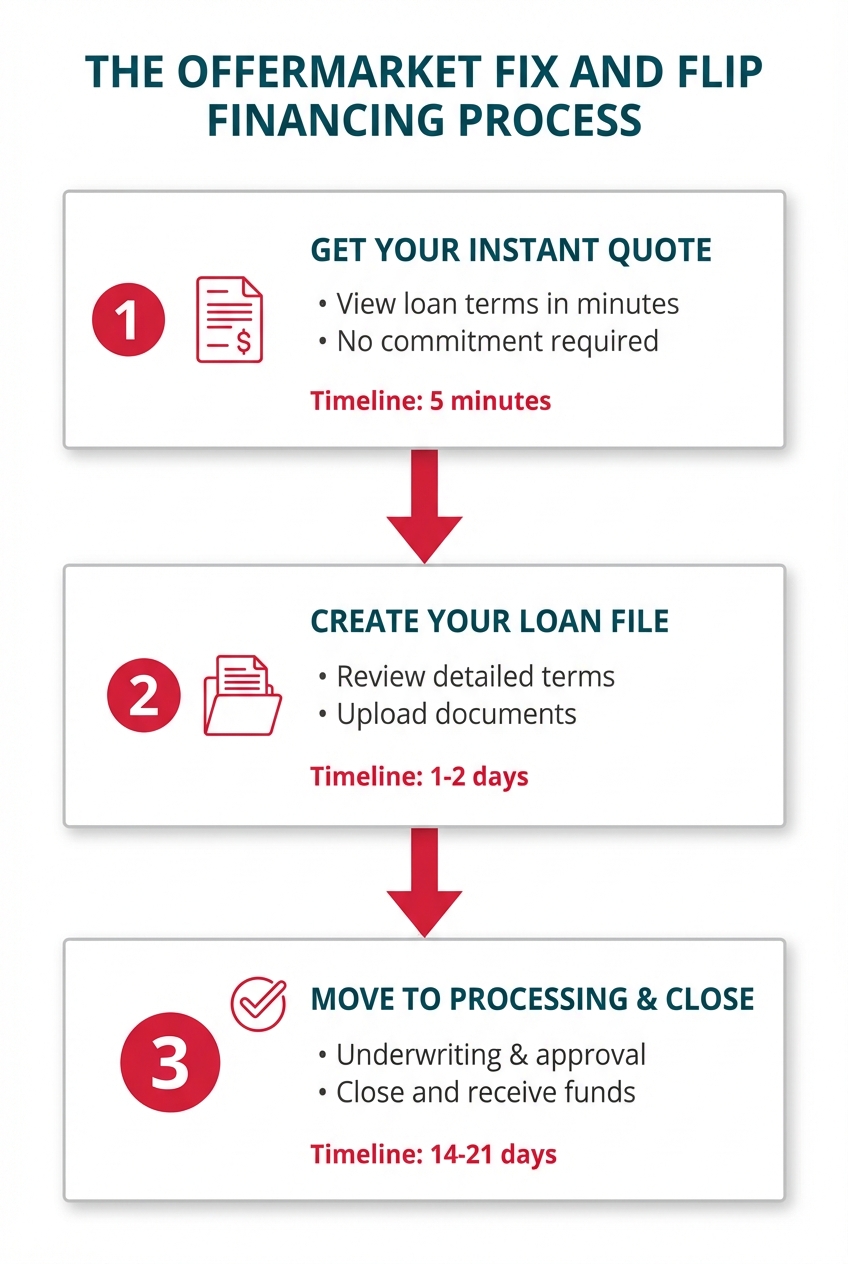

*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Understanding the Debt Service Coverage Ratio Formula: A Key Financial Metric

Understanding the debt service coverage ratio (DSCR) is crucial for anyone involved in finance or real estate. This key financial metric helps assess a company's ability to meet its debt obligations by comparing its net operating income to its total debt service. A solid grasp of the DSCR formula not only aids in evaluating financial health but also plays a pivotal role in investment decisions.

Investors and lenders alike rely on the DSCR to gauge risk and make informed choices. A higher ratio indicates a better capacity to cover debt payments, while a lower ratio raises red flags. In this article, we’ll break down the DSCR formula, explain its significance, and explore how to apply it effectively in various financial contexts.

Understanding Debt Service Coverage Ratio

The debt service coverage ratio (DSCR) is critical for assessing a company's financial capability to fulfill its debt obligations. Understanding the DSCR helps investors and lenders evaluate risk and make informed decisions regarding financial commitments.

Definition and Importance

The debt service coverage ratio (DSCR) quantifies a company's ability to generate enough net operating income to cover its total debt service, which includes interest and principal repayments. A DSCR greater than 1 indicates sufficient income to meet debt obligations, while a ratio below 1 signals potential difficulties in covering debts. This metric serves as a benchmark for financial health, influencing lending decisions and investment strategies significantly.

Key Components of the Formula

The DSCR formula comprises two main components: net operating income (NOI) and total debt service (TDS).

- Net Operating Income (NOI): This figure represents the income generated from regular business operations, excluding taxes and interest. It's calculated by subtracting operating expenses from gross rental income or total revenue.

- Total Debt Service (TDS): Total debt service includes all required payments on debt obligations, both short-term and long-term. This encompasses interest payments and installments of principal due within a specific period.

The formula is expressed as:

DSCR Ratio = Rent / PITIA

Where:

Rent = Total monthly collected rents

PITIA = Monthly payments covering Principal, Interest, Taxes, Insurance, and Association dues

By analyzing these components, it becomes clear how a company's operational effectiveness impacts its financial stability and ability to service debt.

The Debt Service Coverage Ratio Formula

The debt service coverage ratio (DSCR) formula provides a clear method for evaluating financial stability. Understanding its components is crucial for financial assessment and decision-making.

Breakdown of the Formula

The DSCR formula consists of two primary components: Net Operating Income (NOI) and Total Debt Service (TDS).

- Net Operating Income (NOI): This value reflects the income generated from core business activities, calculated by subtracting operating expenses from total revenue. NOI excludes taxes and interest, focusing solely on operational income.

- Total Debt Service (TDS): TDS encompasses all scheduled debt repayments, including both principal and interest obligations. This figure represents the total amount a company must pay out to service its debts.

The relationship is captured in the equation:

DSCR Ratio = Rent / PITIA

Where:

Rent = Total monthly collected rents

PITIA = Monthly payments covering Principal, Interest, Taxes, Insurance, and Association dues

A DSCR value greater than 1 indicates that the entity earns more income than needed to meet its debt obligations, while a value below 1 suggests potential challenges in meeting those obligations.

Example Calculation

To illustrate the application of the DSCR formula, consider the following scenario:

- Net Operating Income (NOI): $150,000

- Total Debt Service (TDS): $100,000

Using the DSCR formula:

DSCR = 150,000 / 100,000 = 1.5

This calculated DSCR of 1.5 signals that the company generates sufficient income to cover its debt payments with a margin to spare, demonstrating solid financial health.

Factors Affecting Debt Service Coverage Ratio

Several elements influence the debt service coverage ratio (DSCR), significantly affecting a company’s ability to meet its debt obligations.

Income Variations

Income variations arise from multiple sources, impacting the net operating income (NOI). Fluctuations in revenue often result from market conditions, customer demand, and seasonal trends. For example, a retail company may experience higher sales during holiday seasons but lower demand during off-peak periods. Consistent revenue generation enhances the DSCR, while volatile income can lead to uncertainty in fulfilling debt payments. Diverse revenue streams can mitigate risks associated with income variability, contributing to a more stable DSCR.

Expense Considerations

Expense considerations play a critical role in the calculation of net operating income. Fixed and variable operating expenses affect overall profitability. For instance, unexpected costs, such as equipment repairs or increased labor expenses, can reduce NOI, negatively impacting the DSCR. Companies that effectively manage expenses through budgeting and operational efficiency maintain a healthier DSCR. Regularly reviewing and optimizing costs helps ensure sufficient income remains available for debt servicing, ultimately strengthening financial stability.

Applications of Debt Service Coverage Ratio

The debt service coverage ratio (DSCR) plays a critical role in various financial scenarios, particularly in real estate investing and business financing. Understanding its applications enhances decision-making for investors and lenders.

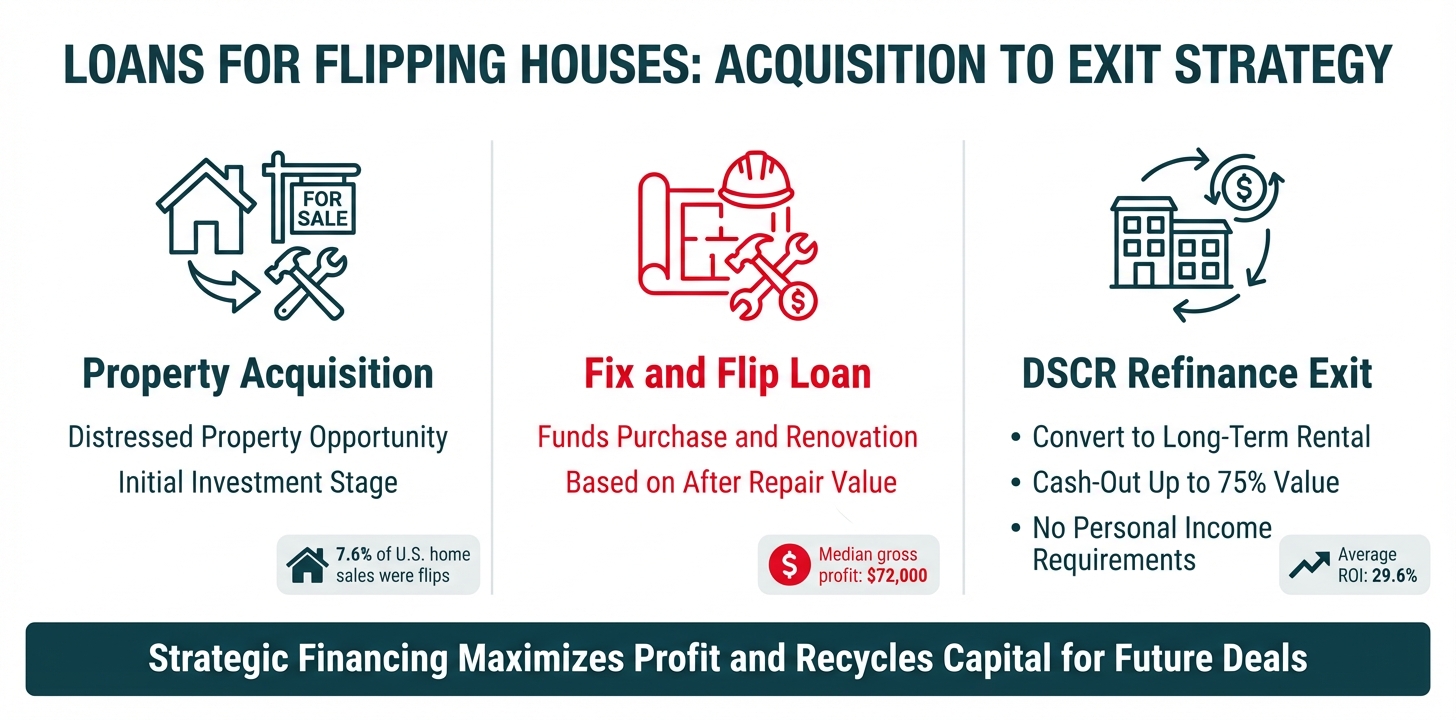

In Real Estate Investing

In real estate investing, the DSCR is essential for determining the viability of a property investment. Investors utilize the ratio to evaluate if rental income can sufficiently cover mortgage payments and other related expenses. A DSCR greater than 1 signals the property generates enough income to cover debt service obligations, indicating a favorable investment. Conversely, a ratio below 1 raises concerns about financial sustainability, potentially leading to default risks. Evaluating the DSCR helps investors select properties with sound income projections, ensuring long-term financial success.

In Business Financing

In business financing, the DSCR serves as a fundamental metric for assessing a company's creditworthiness. Lenders analyze the ratio to determine whether a business generates adequate operating income to meet its debt obligations. A strong DSCR reflects a company's ability to repay loans, enhancing its appeal to potential investors or creditors. Businesses typically aim for a DSCR above 1.25 to satisfy lenders, providing a cushion for unexpected downturns. By closely monitoring their DSCR, businesses can strategically manage debt levels and identify areas for operational improvement, ultimately achieving better financial health.

Conclusion

Mastering the debt service coverage ratio is vital for anyone involved in finance or real estate. This key metric not only helps assess a company's ability to meet its debt obligations but also plays a crucial role in investment decisions. A solid understanding of the DSCR can lead to more informed choices and improved financial health.

By focusing on net operating income and total debt service companies can better navigate financial challenges. A consistent DSCR above 1.25 provides a safety net against uncertainties. As investors and lenders prioritize financial stability the DSCR remains an essential tool for evaluating risk and ensuring long-term success.

Frequently Asked Questions

What is the Debt Service Coverage Ratio (DSCR)?

The Debt Service Coverage Ratio (DSCR) is a financial metric that measures a company's ability to cover its debt obligations. It compares net operating income (NOI) to total debt service (TDS), indicating whether a business generates enough income to pay its debts.

How is the DSCR calculated?

DSCR is calculated using the formula: DSCR = Net Operating Income (NOI) / Total Debt Service (TDS). This ratio helps evaluate a company's financial health and its capacity to manage debt obligations.

What does a DSCR greater than 1 mean?

A DSCR greater than 1 indicates that a company has sufficient net operating income to meet its total debt service, suggesting financial stability. It shows that the company can pay its debts comfortably.

What does a DSCR below 1 signify?

A DSCR below 1 suggests that a company may struggle to cover its debt obligations, indicating potential financial difficulties. It means the company’s income isn’t enough to meet its total debt payments.

What factors can affect the DSCR?

Factors impacting the DSCR include income variability due to market conditions, seasonal trends, and operating expenses. Unexpected costs or negative changes in revenue can lead to a lower DSCR, affecting financial health.

How is DSCR used in real estate investing?

In real estate, DSCR is vital for assessing whether rental income can cover mortgage payments and expenses. A DSCR above 1 indicates a viable investment, while a ratio below 1 raises concerns about sustainability.

Why is DSCR important for lenders?

Lenders focus on DSCR to evaluate a company's creditworthiness. A strong DSCR shows the business’s ability to meet debt obligations, making it a crucial metric for secure loans and financing decisions.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.