*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR

Last updated: October 20, 2025

DSCR stands for Debt Service Coverage Ratio. DSCR is a cash flow metric used by lenders to determine how much debt an investment property can support based on the cash flow generated by the property.

DSCR is not just used in the real estate industry, it is used across all industries where lenders are determining a qualifying loan amount based on the cash flow generated by an asset such as any business. This guide is specifically focused on real estate investors.

What is the DSCR Formula?

There are two (2) formulas which result in slightly different DSCR values. For this reason, it's important to understand which DSCR formula applies to your unique scenario.

| Formula | Rent ÷ PITIA | NOI ÷ Debt Service |

|---|---|---|

| Use Case | 1-4 unit residential | 5+ unit multifamily, commercial, banks |

| Lender type | Non-bank private lenders | Non-bank private lenders, banks, credit unions |

DSCR Meaning

A DSCR above 1.0 means cash flows are positive after paying the ongoing loan costs, while a DSCR below 1.0 means that cash flows are negative. A DSCR of 1.0 therefore indicates breakeven cash flow.

Since the vast majority of DSCR loans use method 1 (Rent ÷ PITIA), we will focus on this DSCR formula as we share insights and example scenarios.

| Meaning | |

|---|---|

| > 1.0 | Positive cash flow |

| 1.0 | Breakeven cash flow |

| < 1.0 | Negative cash flow |

DSCR Greater Than 1.0

A DSCR greater than 1.0 means the property generates positive free cash flow. This means the property's rental income exceeds the property's costs. If you have a bank account strictly for this property, you should expect the cash balance to increase every month unless one or more of the following things happens:

- Tenant stops paying rent

- Taxes increase

- Insurance premium increases

- Maintenance is required

- Property management costs increase

DSCR Equal To 1.0

A DSCR equal to 1.0 means the property operates at breakeven cash flow. This means the property's rental income is exactly the same as the property's costs. If you have a bank account strictly for this property, you should expect the cash balance to remain unchanged every month unless one or more of the following things happens:

- Tenant stops paying rent

- Rent increases

- Taxes increase or decrease

- Insurance premium increase or decrease

- Maintenance is required

- Property management costs increase or decrease

DSCR Less Than 1.0

A DSCR less than 1.0 means the property generates negative free cash flow. This means the property's rental income is less than the property's costs. If you have a bank account strictly for this property, you should expect the cash balance to go down (dangerous!) every month unless one or more of the following things happens:

- Rent increases

- Taxes decrease (not likely!)

- Insurance premium decreases

- Property management costs increase or decrease

DSCR Examples

Example 1: High DSCR

Let's say you're purchasing a SFR with a DSCR loan. You want to have the lowest possible down payment and therefore the highest possible LTV. You find a DSCR lender called OfferMarket and you get the following quote:

- Purchase price: $200,000

- Loan amount: $160,000 (80% LTV)

- Interest rate: 6.25%

- Annual taxes: $2,000

- Annual insurance: $1,000

- Annual HOA: $0

- Monthly rent: $2,000

- Monthly payment: $1,261

- DSCR: 1.59

In this example, the property generates $739 in monthly free cash flow which most rental property investors would find particularly attractive as a starting point from which rents can be gradually increased over time.

Example 2: Low DSCR

Now let's say you're a BRRRR method investor and you're getting a cash out refi with no seasoning. You really want 75% LTV but the DSCR is too low and it's looking like you'll need to lower your LTV in order to qualify your DSCR loan.

| Criteria | 75% LTV | 70% LTV |

|---|---|---|

| Interest rate | 6.50% | 6.25% |

| Loan amount | $150,000 | $140,000 |

| DSCR | 0.95 | 1.01 |

| Cash out proceeds | $142,000 | $133,000 |

| Loan commitment | No, DSCR too low | Yes |

In this example, the DSCR at 75% LTV is below the 1.0 minimum which has become the industry standard. Even if your DSCR lender will allow a DSCR below 1.0, from a risk management perspective, this is not advised. At OfferMarket, we strongly recommend a DSCR of 1.1 or higher because a DSCR of 1.0 will not build cash reserves for the inevitable maintenance and vacancy you will need to budget for.

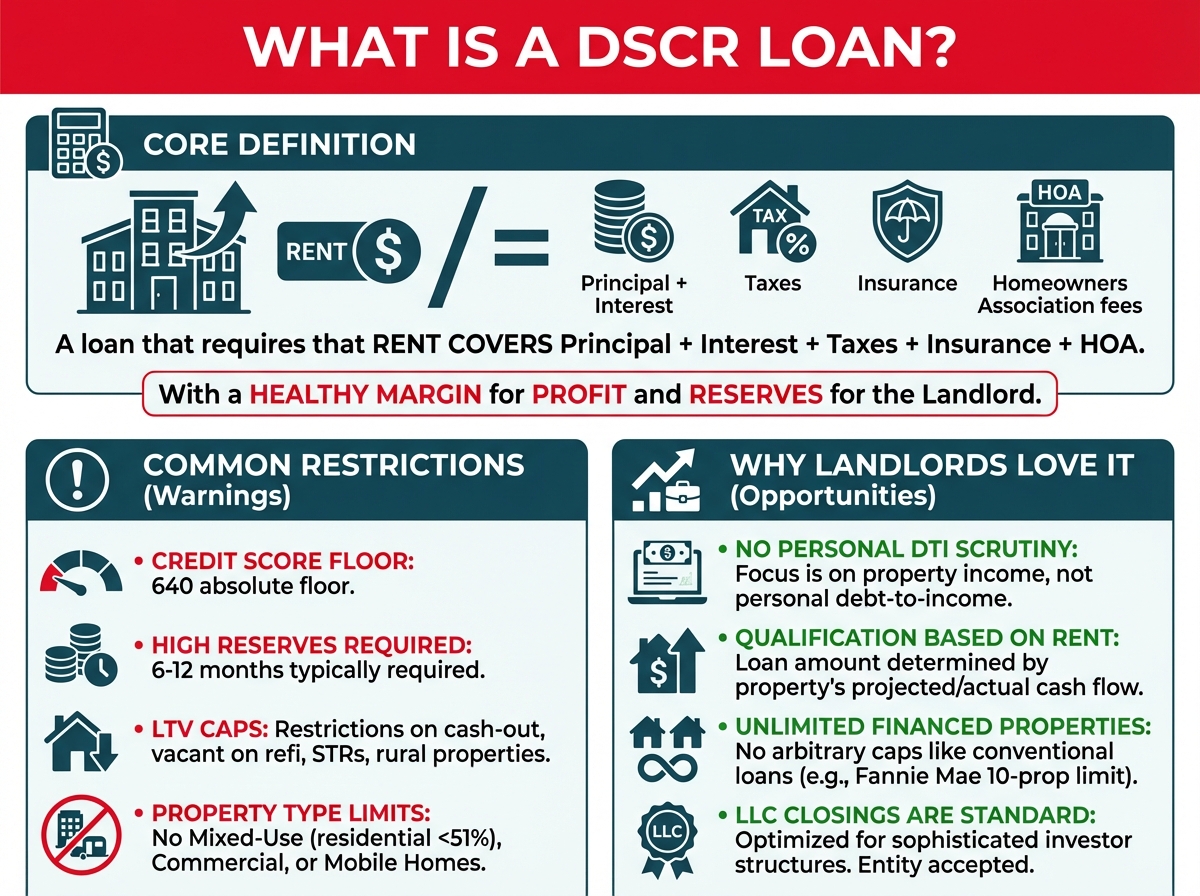

What is a DSCR Loan?

The DSCR loan is a fast-growing financing tool used by rental property investors, which bases qualification strictly on the DSCR of the property and the borrower's credit score, instead of the borrower's verifiable income (i.e. W-2, tax returns).

Instant DSCR Loan Quotes and more from OfferMarket

OfferMarket is a real estate investing platform focused on serving rental property investors, small builders and flippers. We focus exclusively on 1-4 unit residential properties in non-rural markets.

We hope you will accept our invitation to join us and over 20,000 registered members.

Membership is entirely free and comes with the following benefits:

🏚️ Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Market insights

Our mission is to help you build wealth through real estate and we look forward to contributing to your success!

OfferMarket Loans

Check your rate

60 seconds · no credit pull