*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Fix and Flip Loans: The Ultimate Guide for Real Estate Investors

Investing in real estate can be a lucrative venture, but securing the right financing is often a challenge, especially for short-term projects like fix-and-flip properties. That's where DSCR (Debt Service Coverage Ratio) fix and flip loans come into play. These specialized loans are designed to help investors quickly acquire and renovate properties, focusing on the property's potential rather than the borrower's personal income.

Unlike traditional financing, DSCR fix and flip loans cater to investors looking to maximize returns in a competitive market. They’re tailored for speed and flexibility, allowing borrowers to focus on their projects without the usual hurdles of conventional loans. Whether it's purchasing a distressed property or funding renovations, these loans provide the financial support needed to turn opportunities into profits. Understanding how they work can be the key to unlocking success in the fast-paced world of real estate investing.

What Are DSCR Fix And Flip Loans?

DSCR fix and flip loans are financing solutions tailored for real estate investors targeting short-term property renovations. These loans rely on the Debt Service Coverage Ratio (DSCR) to evaluate eligibility, prioritizing the potential cash flow of the property instead of the borrower's personal income or credit history. This approach offers flexibility for borrowers focused on project profitability.

Designed for purchasing and rehabbing distressed or undervalued properties, these loans provide quick access to capital. Investors use the funds to address repairs, upgrades, or other modifications, aiming to increase the property's value before selling it for a profit. Because DSCR loans emphasize the expected returns, they suit investors pursuing time-sensitive opportunities.

Key features include competitive interest rates, shorter repayment terms, and options for financing up to a percentage of the after-repair value (ARV) of the property. These characteristics enable investors to align financial resources with project goals, reducing delays associated with traditional loans. By focusing on property potential, DSCR fix and flip loans streamline the investment process for successful outcomes.

Key Benefits Of DSCR Fix And Flip Loans

DSCR fix and flip loans offer essential benefits to real estate investors, enhancing their ability to execute short-term property projects efficiently. These loans streamline access to capital, prioritizing flexibility and speed over traditional lending methods.

Fast Approval Process

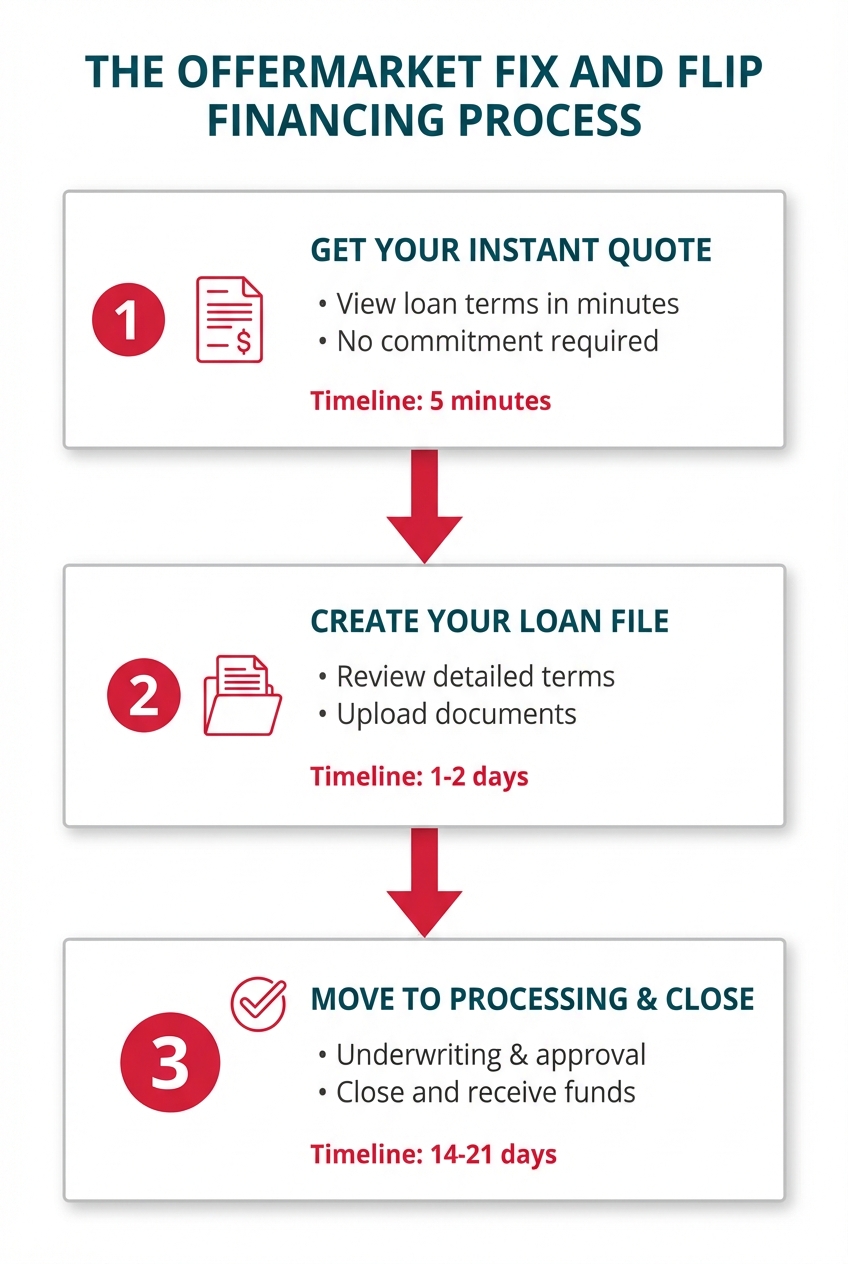

Lenders evaluate loan eligibility using the property's projected cash flow, not the borrower's income. This approach reduces documentation requirements, expediting approval timelines. Investors can secure funding in days rather than weeks, ensuring they don't lose opportunities in competitive markets.

Flexible Loan Terms

Flexible terms, like short repayment periods and ARV-based financing, cater to unique project needs. Loan structures adapt to the investor's strategy, whether focusing on upscale rehabilitation or quick property flips. This flexibility supports diverse property types and project scopes.

No Income Verification

Personal income isn't a limiting factor, as loan approval depends on the property's DSCR metrics. Investors with irregular or limited income streams benefit, including self-employed individuals. This feature broadens accessibility, especially for those focused on asset-driven real estate investments.

How DSCR Fix And Flip Loans Work

DSCR fix and flip loans focus on property performance and are tailored for investors undertaking short-term renovation projects. These loans streamline access to capital by assessing property cash flow rather than individual income.

Loan Qualification Requirements

Lenders assess the property's potential to generate sufficient cash flow to cover loan payments. The key factors include the property's purchase price, renovation budget, and the expected after-repair value (ARV). Borrowers typically provide detailed project plans, timelines, and cost estimates. Since personal income documentation isn't required, creditworthiness and equity contribution, such as a down payment of 15%-30%, are critical for eligibility.

Calculating Debt Service Coverage Ratio (DSCR)

DSCR measures the property's ability to generate income relative to debt obligations. It's calculated by dividing the net operating income (NOI) by the annual debt payments. A DSCR of 1 or higher indicates adequate income to cover loan payments. For fix and flip projects, projected NOI post-renovation is often considered, ensuring the loan aligns with anticipated profitability.

Typical Loan Duration

Loan durations are shorter, typically ranging from 6 to 18 months. This structure matches the temporary nature of fix and flip projects. Investors often aim to complete renovations and sell or refinance the property within this period. Some lenders offer options to extend terms if unforeseen delays arise, although shorter timelines are generally preferred.

Comparing DSCR Fix And Flip Loans With Traditional Loans

DSCR fix and flip loans differ significantly from traditional loans in terms of qualification criteria, approval speed, and project-specific flexibility. These variations make them more suitable for real estate investors with short-term projects.

Differences In Qualification Criteria

Lenders for DSCR fix and flip loans assess eligibility based on the property's projected cash flow rather than the borrower's personal income. They prioritize the property's details, such as the purchase price, renovation costs, and after-repair value (ARV). Borrowers with irregular income streams can still qualify as the focus is on the asset's potential.

In contrast, traditional loans require extensive income verification alongside a high credit score and employment stability. Personal debt-to-income (DTI) ratios and other financial markers heavily influence eligibility, often limiting access for investors without strong personal financial profiles.

Speed And Flexibility Comparison

DSCR fix and flip loans provide faster funding by utilizing streamlined documentation and focusing primarily on the property. Approval often takes days, enabling investors to act swiftly in competitive real estate markets. Flexibility in repayment terms, typically 6–18 months, aligns with the temporary nature of fix-and-flip projects.

Traditional loans tend to have slower approval processes due to more complex underwriting, often taking weeks or months. Their rigid structures and longer repayment periods may not suit short-term or project-based investments.

When To Consider DSCR Fix And Flip Loans

DSCR fix and flip loans suit specific investment objectives and strategic approaches in real estate. They align with short-term property projects where cash flow potential outweighs personal financial profiles.

Ideal Scenarios For Real Estate Investors

Distressed Property Purchases

Investors targeting undervalued, distressed properties benefit from quick funding. Fast capital enables timely property acquisition in competitive markets.Short-Term Renovation Projects

These loans are ideal for projects with defined timelines, ranging from 6 to 18 months. Investors can leverage funds for upgrades and resell properties at a profit based on improved ARV.Cash Flow-Driven Investments

Investors who prefer loans focused on the property's cash flow rather than personal income find DSCR loans advantageous. Eligibility depends on projected post-renovation income (e.g., NOI exceeding loan costs).Irregular Income Situations

Real estate professionals or gig workers without consistent income streams may qualify due to minimal income verification requirements.Market Fluctuations

Property values can vary during the loan term. Negative market shifts might impact ARV, reducing the expected profit margin.Renovation Delays

Unexpected construction delays risk exceeding repayment deadlines, incurring penalties or necessitating loan extensions that increase costs.Insufficient Project ROI

Repayment features tied to property performance make low or negative cash flow a risk. Inaccurate cost estimations could hinder profit.Higher Interest Rates

DSCR loans often carry elevated rates compared to traditional loans. Borrowers must factor increased costs into their profit analysis.

Conclusion

DSCR fix and flip loans offer real estate investors a powerful financing tool tailored to the unique demands of short-term property projects. By focusing on property potential rather than personal income, these loans provide the speed, flexibility, and accessibility needed to succeed in a competitive market.

With features like ARV-based financing, streamlined approval processes, and shorter terms, DSCR loans cater to investors aiming to maximize returns on distressed properties. While they come with risks, understanding how these loans work and leveraging their benefits can significantly enhance efficiency and profitability in real estate ventures.

Frequently Asked Questions

What are DSCR fix and flip loans?

DSCR fix and flip loans are short-term financing solutions designed for real estate investors to purchase and renovate undervalued properties. These loans focus on the property's projected cash flow and after-repair value (ARV) rather than the borrower's personal income, offering fast approval and flexibility for quick property turnover.

How do DSCR fix and flip loans differ from traditional loans?

Unlike traditional loans that require extensive income verification, DSCR fix and flip loans evaluate the property's cash flow potential. They offer faster approval processes, shorter repayment terms, and flexibility, making them ideal for short-term renovation projects.

Who should consider using DSCR fix and flip loans?

Investors targeting distressed properties, undertaking short-term renovation projects, or relying on cash flow-driven investments should consider DSCR fix and flip loans. These loans are particularly beneficial for borrowers with irregular income streams or those focused on asset-based financing.

How is the Debt Service Coverage Ratio (DSCR) calculated?

DSCR is calculated by dividing the property’s net operating income (NOI) by the loan’s debt payments. A DSCR of 1 or higher indicates the property generates enough income to cover loan payments, typically based on projected earnings after renovation.

What are the key benefits of DSCR fix and flip loans?

Key benefits include a fast approval process, ARV-based financing, flexible repayment terms, and reduced income verification. These features streamline capital access, allowing investors to focus on maximizing project returns efficiently.

What are the typical loan terms of DSCR fix and flip loans?

Loan terms usually range from 6 to 18 months, aligning with short-term investment timelines. Some lenders may offer extensions in case of unexpected delays, ensuring project flexibility.

What expenses can DSCR fix and flip loans cover?

DSCR fix and flip loans typically cover the property's purchase price, renovation costs, and sometimes additional expenses based on the after-repair value (ARV). These funds help investors complete necessary upgrades quickly.

Are there risks associated with DSCR fix and flip loans?

Yes, potential risks include market fluctuations affecting property values, renovation delays exceeding repayment periods, higher interest rates, and inaccurate cost estimations leading to lower-than-expected ROI. Proper planning can mitigate these risks.

Do I need a strong credit score to qualify for a DSCR fix and flip loan?

While creditworthiness is considered, eligibility primarily depends on the property's purchase price, renovation budget, and expected after-repair value (ARV). Lenders may allow more flexibility for credit compared to traditional loans.

How do DSCR fix and flip loans streamline the funding process?

These loans focus on property performance and projected cash flow, reducing documentation requirements and income verification. This tailored approach speeds up underwriting and ensures faster access to necessary capital.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull