*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Understanding DSCR Lending: A Comprehensive Guide

Last update: March 16, 2025

Whether you're just starting out or already managing a portfolio of rental properties, understanding how to leverage financing options can make all the difference in growing your investments. A DSCR loan (Debt Service Coverage Ratio loan) is a powerful tool designed specifically for real estate investors like you. Unlike traditional loans that focus on personal income, DSCR loans evaluate the cash flow generated by your rental property, making them an ideal solution for investors with variable income or those looking to expand their portfolio.

This article dives into how DSCR loans work, their benefits, and why they might be the right fit for your investment strategy. You'll discover how this financing option can help you manage risk, optimize cash flow, and unlock opportunities to grow your rental property portfolio. Let’s explore how you can make the most of DSCR loans to achieve your real estate goals.

Understanding DSCR Lending

DSCR loans provide a unique financing solution for real estate investors by focusing on rental income rather than personal income. These loans streamline the application process and offer flexibility for expanding investment portfolios.

What is a DSCR Loan?

A DSCR loan, or Debt Service Coverage Ratio loan, is a financing option designed for real estate investors. It qualifies borrowers based on the cash flow generated by their rental property, not their personal income. This makes it ideal for investors who lack traditional income documentation, such as W2s or tax returns. DSCR loans are commonly used to purchase or refinance income-generating properties, including single-family rentals and multi-unit buildings. They eliminate the need for personal income verification, focusing solely on the property's ability to cover debt obligations.

How Does a DSCR Loan Work?

DSCR loans calculate eligibility using the property's rental income compared to its debt obligations. Lenders evaluate the Debt Service Coverage Ratio, which measures whether the property's income can cover its mortgage payments, taxes, and insurance. A DSCR of 1.0 or higher typically indicates sufficient cash flow. For example, if a property generates $10,000 in monthly rental income and has $8,000 in monthly debt obligations, the DSCR is 1.25. Lenders may also consider factors like credit score, down payment, and reserves. These loans often feature faster processing times, as they bypass personal income verification, making them a practical choice for investors seeking quick financing.

Why Debt Service Coverage Matters in Real Estate

Debt Service Coverage Ratio (DSCR) is a critical metric in real estate financing, as it evaluates a property's ability to generate enough income to cover its debt obligations. For investors, understanding DSCR ensures better financial planning and risk management.

Who are they for?

DSCR loans are designed for real estate investors, including first-time buyers and seasoned professionals. They’re ideal if you’re purchasing income-generating properties like rental homes or multi-unit buildings. These loans are particularly beneficial if you lack traditional income documentation, such as tax returns or pay stubs, or if you’re expanding your portfolio. Investors with variable income, self-employed individuals, or those with multiple properties often find DSCR loans advantageous. They allow you to qualify based on rental income rather than personal earnings, making them a flexible financing option.

What is a Non-QM loan?

A DSCR loan falls under the category of Non-QM (non-qualified mortgage) loans, which cater to borrowers who don’t meet traditional mortgage criteria. Unlike conventional loans, Non-QM loans don’t require standard income verification, making them accessible for self-employed individuals, gig workers, or foreign nationals. DSCR loans specifically focus on the property’s cash flow, using the rental income to determine eligibility. This makes them a popular choice among real estate investors, as they provide an alternative route to financing without the need for personal income documentation.

Pros and cons of a DSCR loan

DSCR loans provide a unique financing solution for real estate investors, offering flexibility and accessibility. However, they also come with specific pros and cons that require careful consideration.

Pros

DSCR loans simplify the financing process for real estate investors. They eliminate the need for personal income verification, making them easier to qualify for compared to conventional loans. The streamlined approval process requires less documentation, ensuring faster processing times.

These loans allow unlimited cash-out options and have no limit on the number of properties you can finance, making them ideal for multi-property owners. They also support jumbo loans for high-end real estate investments. Additionally, DSCR loans accommodate all types of rental properties, including those owned under an LLC, providing flexibility for investors.

Cons

DSCR loans often require higher down payments, typically 20% or more, which can be a barrier for some investors. Lenders may also impose strict credit score requirements, limiting accessibility for borrowers with lower scores.

Since these loans are designed for investors, they aren’t suitable for primary residences or fixer-upper properties. The reliance on rental income means that any fluctuations in cash flow can impact loan eligibility. Additionally, the higher interest rates associated with DSCR loans reflect the increased risk to lenders, potentially raising overall borrowing costs.

How to Calculate DSCR

The Debt Service Coverage Ratio (DSCR) is a critical metric for evaluating a property's ability to generate enough income to cover its debt obligations. Calculating DSCR helps you determine whether a property's cash flow aligns with your investment goals and lender requirements. Essentially, it evaluates whether the income generated by your investment property is sufficient to cover the debts incurred from loans taken to finance that property.

Formula:

DSCR = Rent ÷ PITIA

Where PITIA stands for Principal, Interest, Taxes, Insurance, and Association Dues.

You can use OfferMarket's DSCR Calculator for more practical guidance over this area.

What is a Good Debt Service Coverage Ratio?

A good DSCR typically starts at 1.0 or higher, indicating that the property generates enough income to cover its debt payments. For example, a DSCR of 1.25 means the property produces 25% more income than needed to cover its debt obligations. Lenders often prefer a DSCR of 1.2 or higher, as it reduces their risk and ensures sufficient cash flow for loan repayment.

A higher DSCR, such as 1.5 or above, signals strong financial health and makes the property more attractive to lenders. However, a DSCR below 1.0 indicates negative cash flow, meaning the property doesn't generate enough income to cover its debt, which can disqualify you from a DSCR loan.

When evaluating a property, consider factors like rental income stability, operating expenses, and potential vacancies, as these directly impact the DSCR. For instance, if a property generates $6,700 in annual net operating income and has $5,000 in annual debt payments, the DSCR is 1.34, showing positive cash flow.

Understanding and maintaining a strong DSCR is essential for securing financing and ensuring your investment remains profitable.

Key Differences Between DSCR Loans and Traditional Mortgages

DSCR loans and traditional mortgages differ significantly in their qualification criteria, documentation requirements, and target audiences. Understanding these distinctions helps you determine which financing option aligns with your investment goals.

Qualification Criteria

DSCR loans focus on the property's cash flow, using the Debt Service Coverage Ratio (DSCR) to assess eligibility. A DSCR of 1.0 or higher indicates sufficient rental income to cover debt obligations. Traditional mortgages, however, rely on personal income verification, including tax returns, pay stubs, and a Debt-to-Income (DTI) ratio. This makes DSCR loans ideal for self-employed individuals or those with irregular income streams.

Documentation Requirements

DSCR loans require minimal personal financial documentation. Lenders evaluate the property's rental income potential rather than your personal finances, eliminating the need for tax returns or proof of income. Traditional mortgages demand extensive documentation, including W-2 forms, bank statements, and employment verification, which can slow down the approval process.

Target Audience

DSCR loans cater exclusively to real estate investors purchasing income-generating properties, such as rental homes or multi-unit buildings. They cannot be used for primary residences or fixer-upper properties. Traditional mortgages, on the other hand, are designed for owner-occupied homes, making them unsuitable for investment properties.

Loan Terms and Flexibility

DSCR loans offer flexible terms, including interest-only payment options and no limit on the number of properties financed. Traditional mortgages adhere to stricter guidelines, often limiting the number of properties you can finance and requiring fixed or adjustable-rate terms.

Down Payment and Credit Requirements

DSCR loans typically require a higher down payment, often 20% or more, and may have stricter credit score requirements, such as a minimum of 680. Traditional mortgages may offer lower down payment options, sometimes as low as 3%, and have more lenient credit score thresholds.

Processing Time

DSCR loans often have faster processing times due to the absence of personal income verification. Traditional mortgages involve a more thorough review of personal finances, which can extend the approval timeline.

By understanding these key differences, you can choose the financing option that best supports your real estate investment strategy.

DSCR Loan Requirements

DSCR loans have specific eligibility criteria that focus on the property's income potential rather than your personal financial history. These requirements ensure the property generates enough cash flow to cover its debt obligations, making them ideal for real estate investors.

Can You Get a DSCR Loan with a Low Personal Credit Score?

Yes, you can qualify for a DSCR loan with a low personal credit score, as these loans primarily evaluate the property's income-generating potential. Most lenders require a minimum credit score of 620, though higher scores (680 or above) often secure better terms and interest rates. Since DSCR loans rely on rental income rather than personal income, your credit score plays a secondary role in the approval process. However, a lower credit score may result in less favorable loan terms, such as higher interest rates or stricter down payment requirements.

Can I Use a DSCR Loan to Purchase a New Property or Only to Refinance?

DSCR loans can be used for both purchasing new investment properties and refinancing existing ones. These loans are designed for income-generating properties, such as single-family rentals, multi-family units, or short-term rental properties. When purchasing a new property, the loan amount typically ranges from $100,000 to $20,000,000, depending on the property's value and rental income potential. For refinancing, you can access equity to fund additional investments or improve cash flow. However, DSCR loans cannot be used for primary residences or fixer-upper properties.

Loan-to-Value Ratios in DSCR Lending Explained

Loan-to-Value (LTV) ratios play a critical role in DSCR lending, determining the loan amount relative to the property's value. Lenders use LTV to assess risk, ensuring the loan aligns with the property's income potential and market worth.

How to Get a DSCR Loan

To secure a DSCR loan, you must meet specific criteria based on the property's cash flow rather than personal income. Start by evaluating the property's rental income potential, as lenders use this to calculate the Debt Service Coverage Ratio (DSCR). A DSCR of 1.0 or higher is typically required, indicating sufficient income to cover debt payments.

Next, prepare for the down payment, which usually ranges from 20% to 25% of the property's value, as DSCR loans rarely exceed 80% LTV. Ensure you have at least three months of reserves to cover potential vacancies or unexpected expenses. While personal income isn't a factor, lenders may still review your credit score, with a minimum of 620 often required.

Finally, gather documentation such as rental income statements, property appraisals, and proof of reserves. Submit your application to a lender specializing in DSCR loans, and expect faster processing times compared to traditional mortgages.

By focusing on the property's income potential and meeting lender requirements, you can successfully obtain a DSCR loan to finance your real estate investment.

Request access to our DSCR Loan Calculator Excel Formula Google Sheet

Economic Influences on DSCR Lending

Economic conditions significantly impact DSCR lending, as they directly affect rental income, property values, and borrowing costs. Understanding these influences helps you make informed decisions when securing a DSCR loan for your investment properties.

Interest Rate Fluctuations

Interest rates play a critical role in DSCR lending. Higher interest rates increase borrowing costs, which can reduce the property's cash flow and lower its DSCR. For example, if interest rates rise by 2%, your monthly debt obligations increase, potentially pushing the DSCR below the lender's required threshold of 1.0 or higher. Conversely, lower interest rates improve cash flow, making it easier to qualify for a DSCR loan.

Rental Market Trends

The rental market's performance directly impacts your property's income potential. In a strong rental market with high occupancy rates and rising rents, your property generates more income, improving its DSCR. However, during economic downturns or in oversaturated markets, vacancies and declining rents can reduce cash flow, making it harder to meet loan obligations. For instance, a 10% drop in rental income could lower your DSCR from 1.3 to 1.1, increasing the risk of loan disqualification.

Property Value Changes

Economic factors like inflation, supply and demand, and local market conditions influence property values. Rising property values can enhance your borrowing power, as lenders may offer larger loan amounts based on the property's increased worth. Conversely, declining property values reduce equity, potentially requiring a larger down payment or stricter loan terms. For example, a 15% decrease in property value might necessitate a 25% down payment instead of 20%.

Economic Stability and Risk

Lenders assess economic stability when approving DSCR loans. In stable economies, lenders may offer more favorable terms due to lower perceived risk. During periods of economic uncertainty, such as recessions, lenders may tighten underwriting standards, requiring higher DSCRs or additional reserves. For instance, lenders might increase the required DSCR from 1.2 to 1.5 during economic instability to mitigate risk.

Inflation and Operating Costs

Inflation affects operating expenses like maintenance, utilities, and property taxes, which can reduce net rental income. Higher operating costs lower the property's cash flow, potentially decreasing its DSCR. For example, a 5% increase in property taxes and maintenance costs could reduce your DSCR by 0.1, impacting loan eligibility.

By monitoring these economic factors, you can better anticipate how they influence your property's cash flow and DSCR, ensuring you maintain strong financial health and meet lender requirements.

Current Interest Rates and Housing Market Dynamics

DSCR loan interest rates typically range between 150 to 300 basis points higher than consumer mortgage rates due to the increased risk associated with investment properties. These rates fluctuate based on market conditions, impacting your borrowing costs and overall cash flow.

Are there Any Prepayment Penalties for DSCR Loans?

Most DSCR loans include prepayment penalties to protect lenders from early loan payoffs, which can result in lost interest revenue. These penalties often follow a "54321" structure, where you pay a 5% fee in the first year, 4% in the second, and so on, decreasing annually. Some lenders may offer a flat 3% penalty for the first year, with no penalty afterward. Prepayment terms vary by lender, so reviewing your loan agreement is essential to avoid unexpected costs. While these penalties are common, they rarely affect long-term investors who hold properties for more than 3 to 5 years.

Tips for Enhancing Property NOI for DSCR Lending

Improving your property's Net Operating Income (NOI) directly impacts your Debt Service Coverage Ratio (DSCR), making it easier to qualify for DSCR loans. By focusing on strategies to maximize rental income and minimize expenses, you can strengthen your financial position and secure better loan terms.

How to Improve Your DSCR

Increase Rental Income

Conduct regular market research to ensure your rental rates align with current trends. Raise rents for new tenants or during lease renewals if the market supports it. Invest in property upgrades like modern appliances or added amenities to justify higher rents.

Reduce Vacancies

Implement effective marketing strategies to attract tenants quickly. Maintain your property in excellent condition to retain tenants and address tenant concerns promptly. Offering incentives like move-in specials can also minimize downtime between leases.

Lower Operating Expenses

Negotiate better rates with service providers for maintenance, utilities, and insurance. Consider landlord insurance with dwelling coverage, general liability coverage, and loss of rent coverage to protect against unexpected costs.

Refinance Existing Loans

Explore refinancing options to secure lower interest rates or longer repayment terms. Reducing your monthly debt obligations improves your DSCR by increasing cash flow available for loan payments.

Optimize Property Management

Streamline property management processes to reduce overhead costs. Use technology for rent collection, maintenance requests, and tenant communication to improve efficiency and lower expenses.

By implementing these strategies, you can enhance your property's NOI, boost your DSCR, and improve your eligibility for DSCR loans.

Property Management Strategies and DSCR Loans

Effective property management plays a crucial role in maximizing the benefits of a DSCR loan. By optimizing rental income and minimizing expenses, you can improve your Debt Service Coverage Ratio (DSCR) and secure better loan terms. Here are key strategies to enhance your property's financial performance:

Increase Rental Income

- Upgrade Property Features: Invest in renovations like modern kitchens, energy-efficient appliances, or smart home technology to attract higher-paying tenants.

- Conduct Market Research: Adjust rental rates based on local market trends to ensure competitive pricing without sacrificing income.

- Offer Value-Added Services: Provide amenities such as laundry facilities, parking, or storage to justify higher rents.

Reduce Vacancies

- Implement Marketing Strategies: Use online listings, social media, and professional photography to showcase your property effectively.

- Retain Tenants: Build strong tenant relationships through timely maintenance and responsive communication to encourage lease renewals.

- Offer Incentives: Provide move-in specials or referral discounts to attract new tenants quickly.

Lower Operating Expenses

- Negotiate Vendor Contracts: Secure better rates for maintenance, landscaping, and utility services by negotiating with vendors.

- Implement Energy-Efficient Upgrades: Install LED lighting, programmable thermostats, or solar panels to reduce utility costs.

- Outsource Maintenance: Partner with reliable property management companies to streamline operations and reduce overhead.

Refinance Existing Loans

- Improve Loan Terms: Refinance with a DSCR loan to lower interest rates or access equity for property improvements.

- Optimize Cash Flow: Use refinancing to reduce monthly payments, freeing up funds for additional investments.

Optimize Property Management Processes

- Leverage Technology: Use property management software to automate rent collection, maintenance requests, and financial tracking.

- Monitor Financial Performance: Regularly review income and expenses to identify areas for improvement and ensure a strong DSCR.

By implementing these strategies, you can enhance your property's Net Operating Income (NOI), improve your DSCR, and position yourself for long-term success in real estate investing.

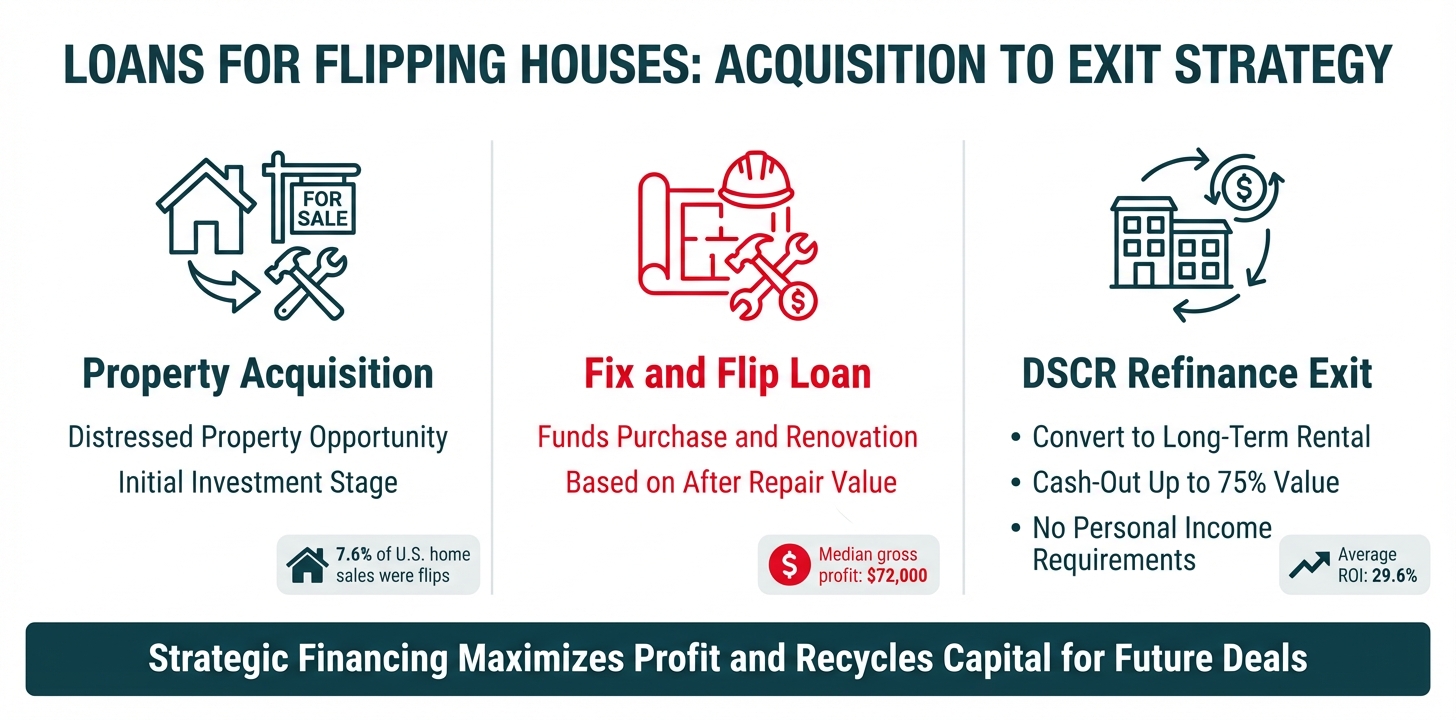

Using DSCR Loans for Fix and Flip Investments

DSCR loans are designed for income-generating properties, making them less suitable for fix-and-flip investments. These loans rely on rental income to determine eligibility, which doesn't align with the short-term nature of fix-and-flip projects. Instead, alternative financing options may better suit your needs.

Alternatives to DSCR Loans

For fix-and-flip investments, consider short-term financing solutions like hard money loans or bridge loans. These options provide faster funding and greater flexibility, allowing you to purchase distressed properties, renovate them, and resell them quickly. Unlike DSCR loans, which require stable rental income, these alternatives focus on the property's potential resale value. Additionally, private money loans offer streamlined approval processes, making them ideal for time-sensitive projects. If you're looking for long-term financing after flipping, a fix-and-rent loan could be a viable option to transition the property into a rental. Always evaluate your project timeline and financial goals to choose the most suitable financing method.

The Relationship Between DSCR Loans and Landlord Insurance

Landlord insurance plays a critical role in securing and maintaining a DSCR loan, as it directly impacts the property's ability to generate consistent rental income. Lenders often require proof of insurance, including dwelling coverage, general liability coverage, and loss of rent coverage, to ensure the property is protected against potential risks. These insurance components safeguard your investment and provide lenders with confidence in the property's financial stability.

Dwelling coverage protects the physical structure of the property from damage caused by events like fires, storms, or vandalism. General liability coverage shields you from legal claims if a tenant or visitor is injured on the property. Loss of rent coverage compensates for rental income lost due to unforeseen circumstances, such as property damage or tenant defaults. This coverage is particularly important for DSCR loans, as it ensures the property's cash flow remains stable even during vacancies or repairs.

When applying for a DSCR loan, lenders assess the property's ability to generate sufficient rental income to cover debt obligations. Landlord insurance, especially loss of rent coverage, helps maintain a strong DSCR by mitigating income disruptions. A DSCR of 1.0 or higher is typically required, and insurance ensures that unexpected events don't negatively impact this ratio. For example, if a property suffers damage and becomes uninhabitable, loss of rent coverage ensures you continue receiving rental income while repairs are made, preserving your DSCR.

Additionally, landlord insurance aligns with the risk management strategies essential for real estate investors. By protecting your property and rental income, you reduce the likelihood of financial distress, which could otherwise jeopardize your ability to meet loan obligations. This proactive approach not only strengthens your DSCR but also enhances your credibility with lenders, making it easier to secure future financing for additional properties.

Locating Off-Market Properties for DSCR Financing

Finding off-market properties can give you a competitive edge when securing DSCR financing. These properties, not listed on public platforms, often present unique opportunities for investors. Here’s how to identify and evaluate off-market properties for DSCR loans:

Networking with Real Estate Professionals

- Connect with agents and brokers specializing in investment properties. They often have access to off-market listings before they hit public platforms.

- Attend local real estate events to build relationships with wholesalers and developers who may have exclusive deals.

- Join investor groups or online forums where members share off-market opportunities.

Direct Outreach to Property Owners

- Send direct mail campaigns to property owners in your target area, expressing interest in purchasing their properties.

- Use skip-tracing tools to identify absentee owners who may be open to selling.

- Leverage social media platforms to connect with potential sellers directly.

Evaluating Off-Market Properties for DSCR Loans

- Assess rental income potential by analyzing comparable properties in the area. A strong DSCR requires sufficient cash flow to cover debt obligations.

- Verify property condition to ensure it’s move-in ready, as DSCR loans don’t finance fixer-uppers.

- Review local market trends to confirm the property’s long-term income stability.

Leveraging Technology

- Use property data platforms to identify underutilized or distressed properties that may be available off-market.

- Analyze zoning changes or development plans that could increase a property’s value and rental income potential.

By focusing on off-market properties, you can uncover hidden gems that align with DSCR loan requirements, ensuring a strong cash flow and a competitive edge in your real estate portfolio.

The Connection Between Real Estate Wholesaling and DSCR Loans

Real estate wholesaling and DSCR loans share a unique synergy, particularly for investors aiming to scale their portfolios. Wholesaling involves identifying off-market properties, securing them under contract, and assigning the contract to another buyer for a fee. DSCR loans, which focus on a property's cash flow rather than personal income, can complement this strategy by providing financing for the end buyer or the wholesaler transitioning into a buy-and-hold investor.

When you wholesale a property, the end buyer often seeks financing to complete the purchase. DSCR loans are ideal for these buyers, especially if the property generates rental income. Since DSCR loans evaluate the property's income potential, they allow buyers to secure financing without relying on personal income documentation. This makes the transaction smoother and faster, aligning with the quick turnaround times typical in wholesaling.

For wholesalers looking to transition into long-term investing, DSCR loans offer a pathway to acquire and hold income-generating properties. By leveraging the cash flow from these properties, you can qualify for financing to expand your portfolio. For example, if you assign a contract on a multi-unit property, you can use a DSCR loan to purchase it, ensuring the rental income covers the debt obligations.

Additionally, DSCR loans provide flexibility for wholesalers who want to diversify their investments. Whether you're targeting single-family homes, multi-unit properties, or commercial real estate, these loans allow you to scale your portfolio without the constraints of traditional financing. The absence of personal income verification and the focus on property cash flow make DSCR loans a practical choice for investors navigating the dynamic real estate market.

By combining real estate wholesaling with DSCR loans, you can create a streamlined process for acquiring and financing properties. This approach not only enhances your investment opportunities but also positions you to build a resilient and diversified real estate portfolio.

Collaborating with Private Lenders for DSCR Financing

Private lenders play a pivotal role in securing DSCR loans, offering tailored solutions for real estate investors. Unlike traditional banks, private lenders specialize in non-QM loans, providing flexibility in underwriting and faster approval processes. Their expertise in evaluating property cash flow and income potential ensures a streamlined experience for investors.

Private lenders focus on the property's financial performance rather than personal income documentation. They assess the Debt Service Coverage Ratio (DSCR) to determine loan eligibility, ensuring the rental income covers debt obligations. This approach benefits investors with variable income or those expanding their portfolios, as it eliminates the need for personal income verification.

Key advantages of working with private lenders include:

- Flexible qualifying criteria: Private lenders often accommodate lower credit scores or smaller down payments if the property demonstrates strong cash flow.

- Access to diverse funding sources: They leverage multiple funding channels, including private equity and securitization, to offer competitive terms for various property types.

- Efficient approval process: Their familiarity with investment property underwriting reduces delays, enabling quicker loan funding.

When selecting a private lender, prioritize those with a proven track record in DSCR loans. Look for lenders offering comprehensive property analysis, including cash flow projections and income potential evaluations. This ensures accurate DSCR calculations and aligns loan terms with your investment strategy.

Private lenders also provide options like temporary rate buydowns, which reduce monthly payments and improve cash flow. This feature is particularly beneficial for investors managing multiple properties or those seeking to optimize their financial performance.

By collaborating with private lenders, you gain access to specialized financing solutions that align with your real estate investment goals. Their expertise and flexibility make them an ideal partner for securing DSCR loans and expanding your portfoli

Conclusion

DSCR loans offer a streamlined financing solution for real estate investors, focusing on rental income rather than personal income. These loans are ideal for investors targeting income-generating properties, as they eliminate the need for traditional income verification and provide faster processing times. By leveraging the property's cash flow, you can secure financing even with variable income or limited documentation, making DSCR loans a practical choice for expanding your portfolio.

Landlord insurance plays a critical role in maintaining a strong DSCR, ensuring consistent rental income and protecting your investment. Coverage options like dwelling coverage, general liability coverage, and loss of rent coverage safeguard against unforeseen events, preserving cash flow and meeting lender requirements. This protection enhances your credibility with lenders, improving your chances of securing future financing.

For fix-and-rent strategies, DSCR loans are a viable option, but they are not suitable for fix-and-flip projects due to their reliance on stable rental income. Instead, alternative financing methods like hard money loans or bridge loans are better suited for short-term renovation projects. By aligning your financing strategy with your investment goals, you can maximize returns and maintain financial stability.

Private lenders often provide more flexible qualifying criteria for DSCR loans, accommodating lower credit scores and smaller down payments if the property demonstrates strong cash flow. Their efficient approval processes and diverse funding sources make them valuable partners for investors seeking tailored financing solutions. Collaborating with private lenders can help you achieve long-term portfolio growth while maintaining a strong DSCR.

Key Takeaways

- DSCR loans focus on rental income: Unlike traditional loans, DSCR loans evaluate a property's cash flow rather than personal income, making them ideal for real estate investors with variable income or limited documentation.

- Streamlined approval process: DSCR loans require minimal personal financial documentation, offering faster processing times compared to conventional mortgages.

- Flexibility for portfolio growth: These loans allow unlimited cash-out options and no limit on the number of properties financed, making them suitable for multi-property investors.

- Higher down payments and interest rates: DSCR loans typically require a 20% or higher down payment and may have higher interest rates due to the increased risk for lenders.

- Landlord insurance is crucial: Coverage like loss of rent and liability insurance helps maintain a strong DSCR by protecting rental income and ensuring financial stability.

- Not suitable for fix-and-flip projects: DSCR loans are designed for income-generating properties, so alternative financing like hard money loans is better for short-term renovation investments.

Frequently Asked Questions

How do DSCR loans differ from traditional mortgages?

Unlike traditional mortgages, DSCR loans focus on the property's cash flow rather than your personal income. This makes them ideal for investors with variable income or those looking to expand their portfolios without extensive personal documentation.

What's a good DSCR ratio?

A DSCR of 1.0 or higher is typically required, but lenders often prefer 1.2 or above to ensure sufficient cash flow. A higher ratio not only improves your chances of approval but also signals strong financial health for the property.

Can you use a DSCR loan for fix-and-flip projects?

No, DSCR loans aren't suitable for fix-and-flip investments since they rely on stable rental income. For such projects, you might explore alternatives like hard money loans or bridge loans.

What is the DSCR term loan?

A Debt Service Coverage Ratio (DSCR) term loan measures a borrower's ability to cover debt obligations. It compares net operating income to total debt service, helping lenders assess risk.

What is a good DSCR for a loan?

A good DSCR for a loan is typically 1.25 or higher, indicating that the borrower generates sufficient income to cover debt payments comfortably.

What does a DSCR of 1.25 mean?

A DSCR of 1.25 means the borrower earns 1.25 times their debt obligations, suggesting a healthy financial position and lower risk for lenders.

What is the downside to a DSCR loan?

The downside to a DSCR loan includes potential rejection if the ratio is too low, limiting borrowing capacity and increasing scrutiny from lenders.

What is the minimum DSCR loan amount?

The minimum DSCR loan amount varies by lender, but many require a DSCR of at least 1.0 to qualify for financing.

Is a 1.5 DSCR good?

Yes, a 1.5 DSCR is considered excellent, indicating the borrower generates 1.5 times the income needed to cover debt obligations, reducing lender risk.

How is DSCR calculated?

DSCR is calculated by dividing net operating income by total debt service. The formula is: DSCR = Net Operating Income / Total Debt Service.

What is the gearing ratio formula?

The gearing ratio formula is: Gearing Ratio = (Total Debt / Total Equity) x 100. It measures financial leverage and risk.

What is DSR in loans?

DSR, or Debt Service Ratio, measures the proportion of income used to cover debt payments. A lower DSR indicates better financial health.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.