*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Understanding DSCR Loan Credit Scores

Last updated: Jan 7, 2025

Navigating the real estate market can be complex. Especially when it comes to financing options like DSCR loans.

Understanding the intricacies of these loans is crucial. It can make or break your investment strategy.

One key factor in securing a DSCR loan is your credit score. It plays a significant role in determining your eligibility and loan terms.

But what exactly is a DSCR loan? How is your credit score factored in? And how can you improve your credit score to secure better loan terms?

This article aims to answer these questions. It provides a comprehensive guide to understanding DSCR loans and the impact of credit scores.

Whether you're an aspiring real estate investor or a real estate agent looking to enhance your advisory skills, this guide is for you.

By the end, you'll have a deeper understanding of DSCR loans, credit scores, and how to optimize your investment strategy. Let's dive in.

What is a DSCR Loan?

A DSCR loan is a type of financing based on a property's cash flow rather than the borrower's income. DSCR stands for Debt Service Coverage Ratio, a metric lenders use to assess financial health.

In simple terms, DSCR loans focus on the property's ability to cover its debt obligations. This makes them appealing for investors who rely on rental income to pay the mortgage.

Unlike traditional loans, where personal income plays a significant role, DSCR loans shift the focus to the investment property's income. This can be particularly beneficial for real estate investors with fluctuating personal incomes.

How DSCR is Calculated

The DSCR is calculated by dividing Net Operating Income (NOI) by total debt service. NOI is the property's revenue minus operating expenses.

To simplify, if a property generates $100,000 in income and costs $80,000 in operating expenses, the NOI is $20,000. If annual debt payments are $10,000, the DSCR is 2.0.

A DSCR greater than 1 indicates the property generates more income than its debt obligations. Lenders prefer higher ratios as they imply lower default risks.

The Relevance of DSCR Loans in Real Estate Investing

DSCR loans hold special significance in real estate investing. They allow investors to leverage rental income instead of personal financial statements to obtain financing. This can open up opportunities for those with modest incomes but profitable rental properties.

Another advantage is the potential for better loan terms with a strong DSCR. Investors might secure lower interest rates and reduced down payment requirements, increasing overall investment profitability.

DSCR loans also accommodate investors whose income sources fluctuate. By focusing on property performance, these loans provide a flexible financing solution. They can be a powerful tool for building and expanding a rental property portfolio.

The Role of Credit Scores in DSCR Loans

Credit scores play a crucial role in securing DSCR loans. They reflect an individual's creditworthiness, impacting loan approval and terms.

Lenders consider credit scores to assess risk. A higher score suggests reliable repayment behavior, while a lower score may indicate potential default.

For DSCR loans, credit scores influence the interest rates offered to borrowers. A better score often results in lower rates, reducing overall loan costs.

Moreover, credit scores can affect the required down payment. Borrowers with higher scores might enjoy more favorable down payment terms. This advantage boosts cash flow, aiding in quicker portfolio expansion.

Understanding Credit Score Factors

Credit scores depend on various factors, each carrying different weights. Payment history is vital, showing timely bills and debt repayments.

Another significant factor is the amount owed. High credit card balances relative to limits can harm scores.

The length of credit history also matters. Longer credit histories often result in better scores, reflecting experience in managing credit. Understanding these factors helps in boosting and maintaining a strong credit score.

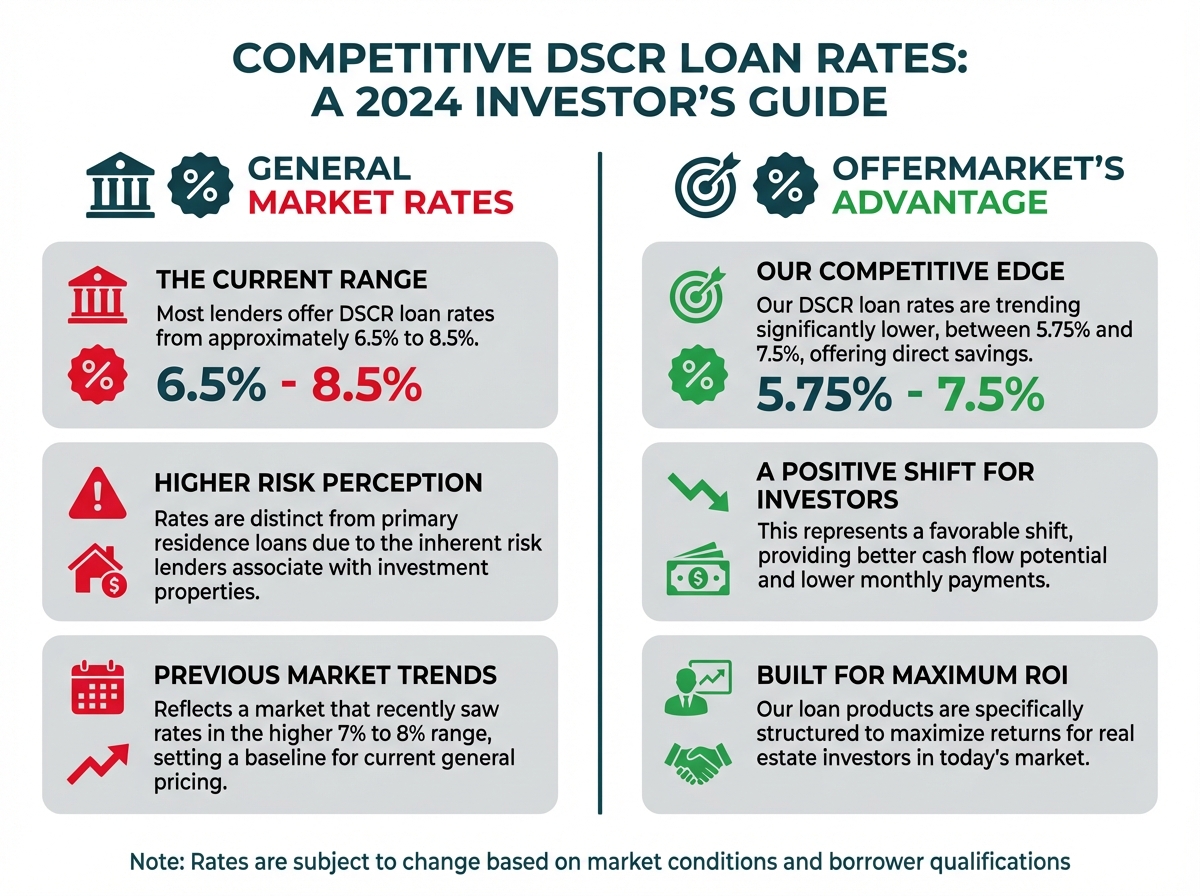

Typical Credit Score Requirements for DSCR Loans

To qualify for DSCR loans, most lenders set minimum credit score thresholds. Typically, a score above 620 is required.

However, requirements can vary between lenders. Some may offer flexibility based on other strengths, like a strong DSCR.

Higher scores may lead to enhanced loan terms. Borrowers with scores over 700 often receive more favorable interest rates and down payment conditions.

Lenders aim to balance risk and reward. Thus, understanding the specific score requirements of different lenders can open up better opportunities in securing a DSCR loan.

How a Higher Credit Score Can Improve Loan Terms

When you improve credit score, you can significantly enhance DSCR loan terms. A key benefit is securing lower interest rates.

This reduction in interest translates to lower monthly payments, freeing up cash for other investments. Furthermore, a robust credit score can lead to reduced down payment requirements.

A smaller down payment means investors can allocate funds more efficiently, perhaps acquiring additional properties. Additionally, higher credit scores can simplify the loan approval process.

Lenders view high scores as less risky, making approvals faster and less cumbersome. Ultimately, working to improve your credit score is a strategic move to optimize DSCR loan conditions.

Strategies to Boost Credit Score

Improving your credit score requires strategic actions and consistent effort. The first step is understanding the factors influencing your score.

Once you know these factors, focus on areas needing improvement. Payment history is a significant factor, so ensure all bills are paid on time.

Consider setting up automatic payments or reminders. Another key strategy is managing your debt-to-income ratio.

Reducing outstanding balances and avoiding new debt can lead to a healthier credit profile. Patience is essential as scores do not improve overnight.

Aim for gradual, steady progress rather than quick fixes. Regularly monitor your credit report to track improvements and spot potential discrepancies.

Steps to Boost Your Credit Score

Boosting your credit score can open doors to better financial opportunities. Here are actionable steps to help you achieve this goal:

- Pay Bills on Time: Late payments can severely impact your score.

- Reduce Credit Card Balances: Aim to keep balances below 30% of your credit limit.

- Avoid New Credit Requests: Applying for new credit generates hard inquiries, which can lower your score.

- Increase Credit Limits: If possible, request a credit limit increase to improve your utilization ratio.

- Maintain Old Accounts: Longer credit histories often benefit scores.

Implementing these steps requires dedication but can significantly enhance your credit profile over time. Stay disciplined and committed to maintaining good credit habits.

Disputing Errors on Credit Reports

Errors on credit reports can damage your credit score. Identifying and disputing these inaccuracies is essential for score improvement.

First, obtain your credit report from major bureaus. Thoroughly review the report, checking for unfamiliar accounts, incorrect balances, and inaccurate payment records.

If you identify errors, dispute them promptly. Contact the credit bureau with a detailed explanation and any supporting documents. Most disputes are investigated within 30 days.

A corrected report can lead to a higher score. Regularly checking your credit report helps catch errors early and maintains your credit health.

The Impact of Credit Utilization Ratios

Credit utilization ratios are crucial in determining your credit score. This ratio compares your credit card balances to your available credit.

Keeping this ratio low, ideally below 30%, can positively impact your score. High utilization suggests over-reliance on credit, which lenders see as risky.

To lower your ratio, pay down balances strategically. Also, consider spreading your debt across multiple accounts. Regularly reviewing utilization ratios as part of credit management helps maintain a healthy credit profile.

Maintaining a low credit utilization showcases financial discipline and can improve your chances of favorable loan terms. Understanding this factor is key to managing and enhancing your credit score.

DSCR Loan Requirements and How to Meet Them

Here’s a table summarizing DSCR loan requirements and strategies to meet them:

| Requirement | Explanation | Strategies to Meet Requirement |

|---|---|---|

| Debt Service Coverage Ratio (DSCR) | Lenders require rental income to sufficiently cover loan payments. | Maintain accurate financial records and calculate DSCR regularly. |

| Income Documentation | Accurate records of property income and expenses are necessary for approval. | Document all income and expenses thoroughly, including receipts and contracts. |

| Property Value | A higher property value improves the likelihood of meeting DSCR criteria. | Enhance property value through renovations or strategic rent increases. |

| Attractive Property for Tenants | A well-maintained property attracts quality tenants, ensuring steady income. | Invest in regular maintenance and upgrades to appeal to prospective tenants. |

| Robust Property Management | Effective management maximizes income and maintains property appeal. | Implement strong tenant screening and lease management practices. |

Calculating Potential Rental Income for DSCR Qualification

Calculating potential rental income is pivotal for DSCR loan qualification. Start by analyzing market trends and comparable properties.

This will provide insights into expected rental rates. Consider vacancy periods and operational costs as well. Accurate predictions help lenders assess the property's viability.

Focusing on realistic, data-driven projections can enhance your loan application. Also, provide any added benefits or unique features of your property that could attract higher rent.

These considerations build a strong case for potential earnings, supporting your DSCR loan eligibility.

The Importance of Property Cash Flow

Property cash flow is a crucial component in securing a DSCR loan. Lenders evaluate cash flow to ensure sustainability of property payments.

Positive cash flow indicates that a property can support its debt. Therefore, managing your property's income and expenses is vital.

Focus on maintaining efficient operations and minimizing costs. This will allow you to improve margins.

Ensure rent collection processes are smooth to secure steady revenue. A strong cash flow reflects well on loan applications and can help achieve favorable terms.

Advantages of DSCR Loans Over Traditional Financing

DSCR loans offer unique benefits compared to traditional financing. They primarily focus on the property's ability to generate income.

This focus can be advantageous for investors with irregular personal income streams. DSCR loans often have more lenient underwriting requirements.

This flexibility can be critical for growing a real estate portfolio. Additionally, these loans can provide larger funding amounts.

This makes it easier to capitalize on lucrative opportunities. Leveraging a DSCR loan allows investors to scale their investments while taking advantage of unique financial circumstances.

Case Studies: Successful DSCR Loan Applications

Real-life examples provide invaluable insights into the DSCR loan process. Consider the case of an investor with a duplex in a thriving neighborhood.

This investor leveraged the property's strong rental history to secure a DSCR loan. By presenting detailed financial records, they highlighted consistent income and low vacancy rates. The bank appreciated the property's positive cash flow.

This resulted in favorable loan terms and minimal down payment requirements. Another example involves a real estate investor expanding their portfolio to include a triplex.

The investor focused on properties with potential for rent increases through minor upgrades.

By demonstrating projected rental income growth, they successfully secured a DSCR loan. This approach helped them take advantage of rising market values.

Finally, an ambitious investor used DSCR loans to refinance existing properties.

They showcased enhanced property management practices leading to improved income streams. With the loan, they refinanced at a lower interest rate and expanded their investments.

These cases highlight the strategic use of DSCR loans in diverse scenarios. Success depends on presenting detailed financial data and understanding market dynamics.

Additional Considerations for Real Estate Investors

Investing in real estate involves more than securing the right financing. Savvy investors understand the importance of comprehensive risk management strategies.

A solid financial cushion is essential for unexpected repairs or vacancies. Beyond finances, maintaining good tenant relationships can enhance property stability.

Networking with other investors can provide valuable insights and opportunities. Joining real estate clubs or forums can expand your knowledge and connections.

Additionally, keeping abreast of market trends helps in making informed decisions. Understanding local regulations and market dynamics is crucial for success.

These additional considerations help investors navigate challenges more effectively.

The Importance of Landlord Insurance

Landlord insurance protects your investment from potential losses. It covers property damage, liability claims, and lost rental income.

Standard homeowner's insurance may not cover these situations. Therefore, specialized coverage is crucial for rental properties.

Insurance mitigates financial risks associated with unforeseen events. It helps maintain cash flow stability and protects your assets.

Choosing the right policy and coverage level is essential. Consult with an insurance specialist to tailor a plan to your needs.

Finding Off-Market Properties

Off-market properties often present unique investment opportunities. They are properties not listed on public multiple listing services.

These properties might be sold directly by the owner or through private auctions. Finding them requires diligent networking and research.

Real estate agents, local connections, and investment groups can assist. Off-market deals can often be negotiated at better prices.

Understanding the seller's motivation can be key to successful negotiations. This approach can expand your portfolio with less competition.

Real Estate Wholesaling and DSCR Loans

Wholesaling can be a strategic approach for real estate investors. It involves securing properties at discounted prices to resell quickly.

This method does not typically involve owning the property long term. However, DSCR loans can support expanding a wholesaling business.

For investors using rentals to bolster their wholesaling ventures, DSCR loans offer flexibility. They enable the temporary holding of properties.

Understanding both strategies helps leverage financial and market opportunities. This multifaceted approach can optimize overall investment strategies.

Conclusion: Optimizing Your Investment Strategy with DSCR Loans

DSCR loans provide an advantageous financing option for savvy real estate investors. Their flexibility caters to both seasoned and aspiring investors.

Integrating DSCR loans into your strategy can enhance your investment potential. They offer significant benefits compared to traditional financing.

Understanding credit score impacts and improving these scores is crucial for better loan terms. A higher credit score can lead to reduced interest rates.

By optimizing your credit standing and financial practices, you can unlock superior investment opportunities. This preparedness secures more favorable loan conditions.

Applying these insights can yield growth in your rental property portfolio. Diversifying your strategies with DSCR loans can lead to long-term success.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.