*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Loans: Navigating DSCR Loan Guidelines for Optimal Financing

Last Updated: 16 January, 2025

Purchasing a home or expanding a real estate investment portfolio is a significant financial undertaking. Securing the right mortgage loan can profoundly impact your financial stability and investment success. Among the various metrics lenders use to assess loan applications, the Debt Service Coverage Ratio (DSCR) emerges as a crucial indicator of financial health. Understanding DSCR home loans and their guidelines can empower you to make informed decisions, secure favorable loan terms, and ensure long-term financial prosperity.

This comprehensive guide delves into DSCR home loans, focusing on DSCR loan guidelines, benefits, qualification criteria, and strategies to optimize your DSCR for better loan outcomes.

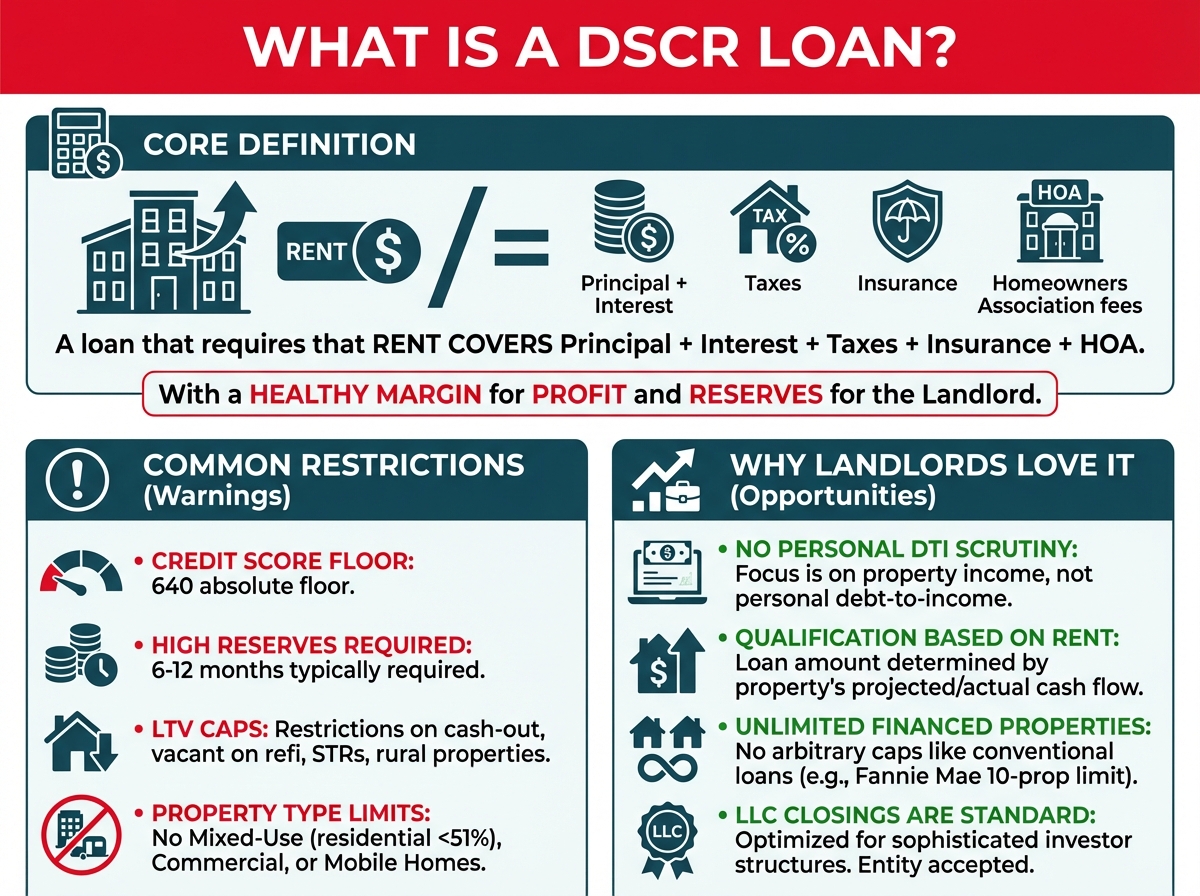

Understanding DSCR Loans

A DSCR Home Loan is a specialized mortgage product that evaluates a borrower's ability to manage mortgage payments based on their Debt Service Coverage Ratio. Unlike traditional home loans that primarily consider credit scores and income levels, DSCR home loans focus on the ratio of your income relative to your debt obligations.

This focus makes DSCR home loans particularly relevant for real estate investors and individuals with multiple income streams or existing debts.

The Importance of Debt Service Coverage Ratio (DSCR)

What is DSCR?

The Debt Service Coverage Ratio (DSCR) is a financial metric used to assess an individual's or property's ability to cover debt payments with its income. It is calculated by dividing the Net Operating Income (NOI) by the Total Debt Service (TDS).

DSCR Formula

DSCR = Net Operating Income (NOI) / Total Debt Service (TDS)

- Net Operating Income (NOI): NOI is calculated by total income generated minus operating expenses (excluding interest and taxes).

- Total Debt Service (TDS): The total of all debt obligations, including mortgage payments, car loans, and credit card debts.

Why DSCR Matters

- Risk Assessment: DSCR provides lenders with a clear picture of a borrower's ability to meet debt obligations, reducing the risk of default.

- Loan Approval: A higher DSCR increases the likelihood of loan approval and can lead to more favorable loan terms.

- Financial Health: Maintaining a healthy DSCR ensures that borrowers can manage their debts without financial strain.

DSCR Loan Guidelines: Key Criteria

Understanding the guidelines that govern DSCR home loans is essential for both borrowers and lenders. These guidelines help ensure that borrowers can manage their debt obligations without financial strain and that lenders minimize the risk of default.

Minimum DSCR Requirements

Most lenders set a minimum DSCR requirement to qualify for a DSCR home loan. Typically, this minimum ratio is around 1.2, meaning the property's income should be at least 1.2 times its debt obligations. However, higher ratios may be required for more favorable loan terms or for properties with higher risk profiles.

Credit Score Considerations

While DSCR is a critical metric in DSCR home loans, lender also consider the borrower's credit score. A higher credit score can enhance loan approval chances and may lead to better interest rates. Generally, lenders look for a credit score of 680 or above for DSCR home loans, though this can vary based on the lender and the specific loan product.

Income Stability and Sources

Lenders assess the stability and diversity of a borrower's income sources. Consistent and reliable income streams, such as steady rental income from multiple properties or additional business ventures, can positively influence the DSCR and improve loan approval odds. Borrowers with diversified income sources are seen as less risky, as they are less likely to default if one income stream falters.

Property Appraisal Standards

The property's value and income-generating potential are critical factors in DSCR home loans. Lenders require a thorough property appraisal to ensure that the property's market value and rental income are sufficient to cover the debt service. The appraisal assesses the condition, location, and comparable property values to determine the property's ability to generate consistent income.

Down Payment and Equity

Down payment requirements for DSCR home loans can vary. While traditional mortgages might require a down payment of 20%, DSCR home loans, especially for investment properties, might necessitate a higher down payment, ranging from 25% to 30%. A substantial down payment reduces the lender's risk and demonstrates the borrower's commitment to the investment.

Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) Ratio is another important guideline. It represents the loan amount as a percentage of the property's appraised value. For DSCR home loans, lenders often prefer a lower LTV ratio, typically 75% to 80%, ensuring that borrowers have significant equity in the property.

Below is a comprehensive table outlining key DSCR loan guidelines:

| Guideline | Description |

|---|---|

| Minimum DSCR Ratio | Lenders typically require a DSCR of at least 1.2. Higher ratios may qualify borrowers for better loan terms and lower interest rates. |

| Credit Score Threshold | A credit score of 680 or above is generally preferred. Some lenders may accept lower scores if the DSCR is significantly high. |

| Income Documentation | Comprehensive documentation is required, including tax returns, bank statements, and proof of rental income or other income sources. |

| Property Appraisal | A professional appraisal assesses the property's market value and income-generating potential to ensure it meets lender standards. |

| Down Payment Requirement | Down payments for DSCR home loans typically range from 25% to 30% for investment properties, demonstrating significant equity. |

| Loan-to-Value (LTV) Ratio | Lenders prefer an LTV ratio of 75% to 80%, ensuring borrowers have substantial equity in the property. |

| Debt-to-Income (DTI) Ratio | While DSCR is the primary focus, lenders also consider the overall DTI ratio, which should generally be below 40%. |

| Loan Term Options | DSCR home loans may offer various loan terms, including 15, 20, or 30-year periods, and may include interest-only periods during initial years. |

| Property Type Eligibility | Eligible property types include single-family rentals, multifamily units (duplexes, triplexes), and certain commercial properties. |

| Occupancy Requirements | For investment properties, lenders may require a minimum occupancy rate (e.g., 85%) to ensure stable rental income. |

| Additional Income Streams | Borrowers with multiple income sources, such as business income or additional rental units, can leverage these to enhance their DSCR. |

Benefits of DSCR Home Loans

DSCR home loans offer distinct advantages for both borrowers and lenders, making them an attractive option in specific financial scenarios.

Advantages for Real Estate Investors

- Higher Loan Amounts: DSCR home loans can qualify investors for larger loan amounts based on the property's income, enabling them to purchase more valuable or multiple properties.

- Competitive Interest Rates: A higher DSCR often results in lower interest rates, reducing overall borrowing costs and enhancing investment profitability.

- Flexible Terms: DSCR home loans may offer more flexible repayment options, such as interest-only periods or extended loan terms, catering to the specific income patterns of rental properties.

Benefits for Homeowners

- Access to Larger Properties: Homeowners can leverage DSCR home loans to secure financing for larger or more expensive homes by demonstrating strong income relative to their debt obligations.

- Better Loan Terms: A healthy DSCR can lead to more favorable loan terms, such as lower interest rate and reduced down payment requirements, making homeownership more affordable.

- Improved Financial Stability: Maintaining a strong DSCR ensures that homeowners can manage their mortgage payments without undue financial strain, promoting long-term financial health.

Who Should Consider a DSCR Loan?

DSCR home loans are particularly beneficial for specific groups of borrowers. Understanding whether you fall into one of these categories can help you determine if a DSCR home loan is the right choice for your financial needs.

- Real Estate Investors: Ideal for those looking to purchase rental properties or expand their investment portfolios.

- Individuals with Multiple Income Streams: Suitable for borrowers with additional income sources beyond their primary job, such as business income or side ventures.

- Owners of Multifamily Units: Beneficial for those owning duplexes, triplexes, or apartment buildings where rental income can cover debt obligations.

- Borrowers with Existing Debts: Helps individuals manage multiple debts by focusing on the income generated by their properties.

Calculating Your DSCR

Accurately calculating your DSCR is essential for understanding your loan eligibility and financial health. Follow these steps to determine your DSCR:

Step 1: Determine Your Net Operating Income (NOI)

NOI = Total Income - Operating Expenses

Example:

- Total Income: $150,000 (from rental income)

- Operating Expenses: $50,000 (maintenance, property management fees, taxes)

NOI = $150,000 - $50,000 = $100,000

Step 2: Calculate Your Total Debt Service (TDS)

TDS = Principal + Interest Payments

Example:

- Annual Mortgage Payments: $80,000

TDS = $80,000

Step 3: Apply the DSCR Formula

DSCR = NOI / TDS

Calculation:

DSCR = $100,000 / $80,000 = 1.25

A DSCR of 1.25 signifies that your income generates 25% more than your debt obligations, indicating a manageable debt load.

Strategies to Improve Your DSCR

Enhancing your DSCR can lead to better loan terms, increased approval chances, and overall financial health. Here are effective strategies to improve your DSCR:

1. Enhancing Net Operating Income (NOI)

Boosting your NOI directly improves your DSCR. Consider the following approaches:

- Raise Rental Rates: If market conditions permit, increasing rental rates can enhance your income without a proportional rise in expenses.

- Add Revenue Streams: Introduce additional services or amenities, such as laundry facilities, parking fees, or premium amenities, to generate extra income.

- Improve Occupancy Rates: Implement effective marketing and tenant retention strategies to minimize vacancies and ensure consistent income.

2. Reducing Operating Expenses

Lowering your operating expenses contributes to a higher NOI, thereby improving your DSCR. Here’s how:

- Optimize Maintenance Costs: Regular maintenance can prevent costly repairs in the future. Additionally, negotiating better rates with service providers can reduce expenses.

- Implement Energy Efficiency Measures: Investing in energy-efficient appliances and systems can lower utility costs, contributing to reduced operating expenses.

- Streamline Property Management: Efficient management practices can eliminate unnecessary expenses and enhance operational efficiency.

3. Refinancing Existing Debts

Refinancing your existing debt can lead to lower interest rates or extended loan terms, reducing your Total Debt Service and improving your DSCR.

- Secure Lower Interest Rates: Refinancing to a lower interest rate decreases your debt service payments, enhancing your DSCR.

- Extend Loan Terms: Spreading debt over a longer period can reduce annual debt service, providing a more manageable DSCR.

4. Property Upgrades and Enhancements

Enhancing the value of your property can justify higher rents or prices, thereby increasing your income.

- Renovations and Upgrades: Investing in property improvements can lead to higher rental rates and increased property value.

- Strategic Market Positioning: Positioning your property effectively within the market can boost demand and rental income.

5. Debt Restructuring

Restructuring your debt can provide more favorable terms and improve your DSCR.

- Adjust Loan Terms: Negotiate more flexible loan terms, such as interest-only periods or flexible repayment schedules, to improve cash flow.

- Consolidate Debt: Combining multiple debts into a single, more manageable loan can streamline payments and potentially lower overall debt service.

Conclusion

Mastering your Debt Service Coverage Ratio (DSCR) is fundamental to securing and optimizing DSCR home loans. A strong DSCR not only enhances your chances of loan approval but also secures more favorable loan terms, reducing borrowing costs and increasing your investment's profitability.

By focusing on strategies to increase your Net Operating Income, reduce operating expenses, and manage debt responsibly, you can maintain a healthy DSCR that supports your investment goals. Additionally, avoiding common mistakes such as overestimating income or misusing loan funds ensures that your financial health remains robust, positioning you for long-term success.

As the financial landscape evolves, staying informed about emerging trends and adapting your strategies accordingly will be key to maximizing the benefits of DSCR home loans. Whether you're expanding your real estate portfolio, refinancing existing debt, or optimizing property value, mastering DSCR empowers you to make informed, strategic decisions that drive your investments forward.

Embrace the insights and strategies outlined in this guide to harness the full potential of DSCR home loans, ensuring your investments are financially healthy, resilient, and poised for enduring success.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.