*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Understanding The DSCR Loan Pre-Approval Process

Last updated: Jan 7, 2025

Navigating the world of real estate investment can be complex. Especially when it comes to financing options.

One such option is the DSCR loan.

DSCR, or Debt Service Coverage Ratio, is a key metric in real estate investing. It's used to assess the cash flow of rental properties.

Understanding DSCR loans and their pre-approval process is crucial for investors. It can open doors to lucrative investment opportunities.

This article aims to demystify the DSCR loan pre-approval process. It will guide you through the steps to obtaining pre-approval.

We'll delve into the requirements of DSCR loans. We'll also discuss how they differ from other investment property loans.

By the end, you'll have a comprehensive understanding of DSCR loans. You'll be equipped to leverage them for your investment strategies.

What is a DSCR Loan?

A DSCR loan is a financing option for real estate investors. It stands out from traditional loans.

The main focus of a DSCR loan is on rental property income. Lenders assess the property's ability to cover loan payments.

DSCR, or Debt Service Coverage Ratio, is a crucial metric. It indicates how well rental income can service debt obligations.

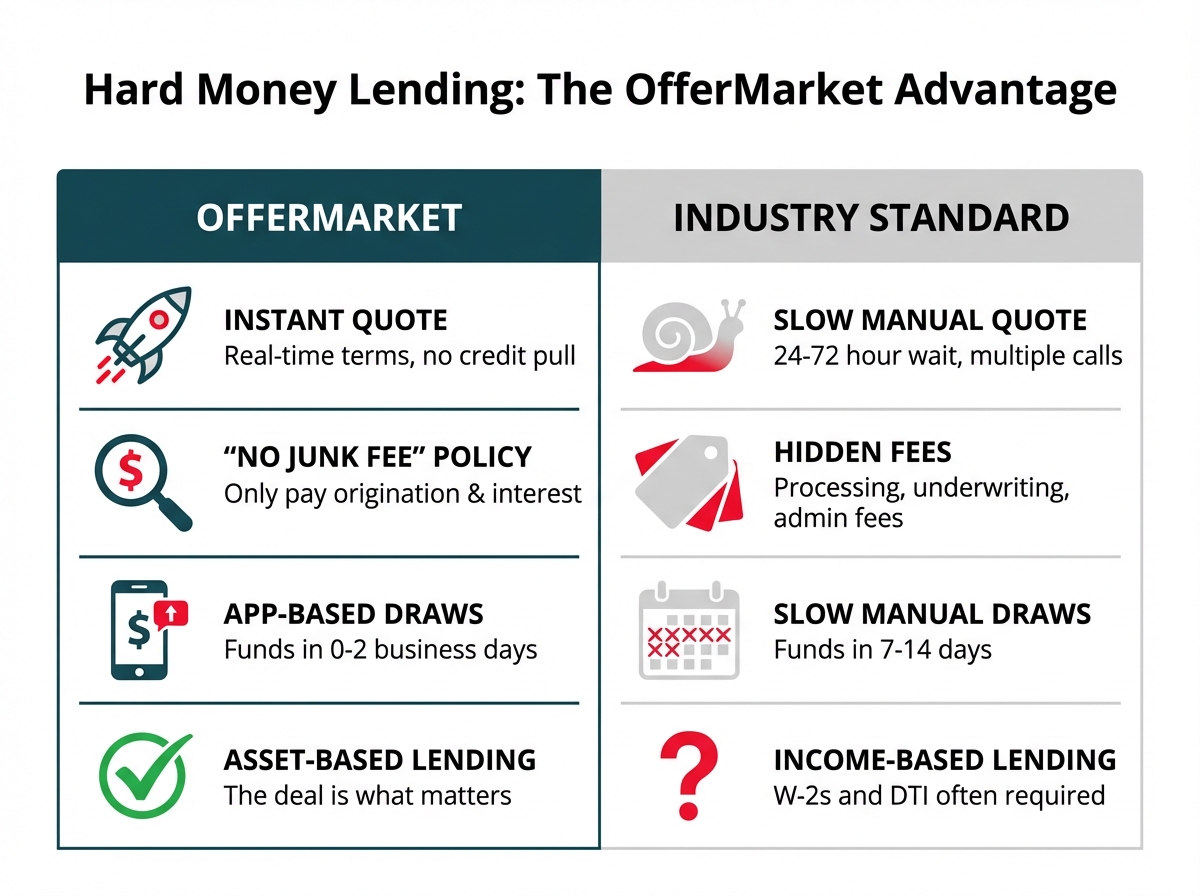

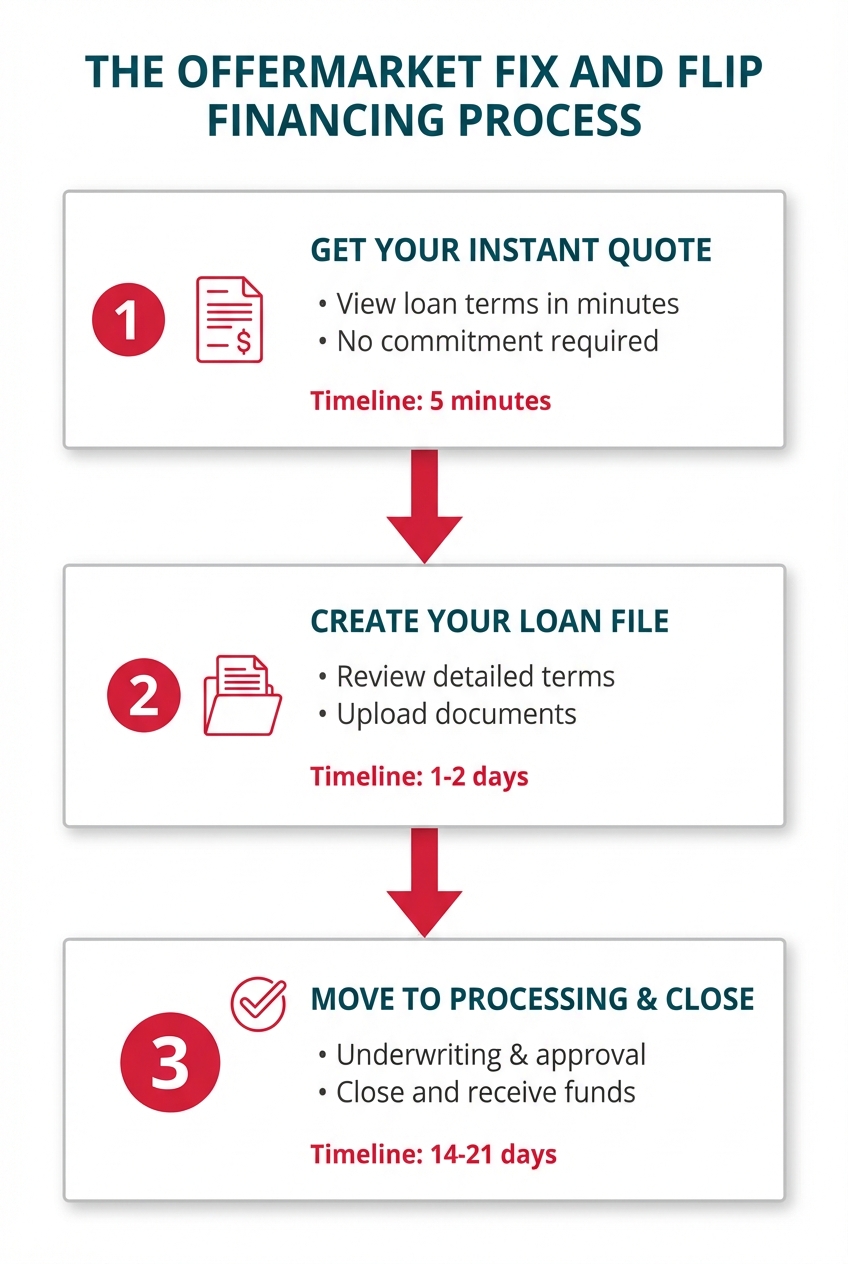

At OfferMarket, the process begins with an instant loan quote — not a full pre-approval. This quote takes less than 2 minutes and requires no credit pull. While traditional pre-approvals may involve a hard inquiry and deeper underwriting upfront, OfferMarket’s instant quote offers a fast, commitment-free estimate based on property and borrower details. Full pre-approval and funding decisions happen after underwriting review.

Investors often prefer DSCR loans for their flexibility. They don't rely heavily on personal income verification.

In real estate, cash flow is king. DSCR loans align perfectly with this principle. They emphasize the property's income-generating potential.

These loans are particularly attractive for both seasoned and new investors. They offer a unique approach to financing that emphasizes real cash flow.

The Importance of DSCR in Real Estate Investing

In real estate investing, the DSCR plays a critical role. It helps gauge a property's financial health. A strong DSCR indicates a reliable income stream.

Lenders value DSCR because it shows the ability to repay loans. A higher DSCR means less risk of default. This makes investing less risky for both parties involved.

Investors also rely on DSCR to assess property viability. A favorable DSCR suggests a property can sustain mortgage payments. It can also support other operational costs.

Understanding DSCR aids in investment decision-making. It allows investors to compare different properties. This comparison helps in choosing properties with better revenue potential.

For those using DSCR loans, this ratio is key. It determines the eligibility and favorable terms of the loan. Ultimately, it serves as a cornerstone of sound investment strategy.

Calculating Your Debt Service Coverage Ratio

Calculating the Debt Service Coverage Ratio is essential for potential investors. This ratio assists in evaluating a property's financial strength. A well-calculated DSCR reveals how comfortably debt obligations can be met.

To compute the DSCR, you need two main figures. First, determine the property's net operating income (NOI). The NOI is the total rental income minus operating expenses.

Next, calculate the total debt service. This includes all loan payments, both principal and interest. With these figures ready, you can proceed to the calculation.

The formula for DSCR is straightforward:

- DSCR = Net Operating Income / Total Debt Service

A DSCR greater than 1 signals good financial health. It means the property generates more income than needed for loan payments. This margin offers a safety net for unexpected costs.

Conversely, a DSCR below 1 suggests financial strain. It indicates the income doesn't fully cover debt costs. Such a situation poses a risk to both the investor and lender.

Evaluating DSCR also aids in financial planning. Investors can adjust expenses or seek higher rents. These adjustments improve DSCR, making investments more attractive and sustainable.

DSCR Loan Requirements: What You Need to Know

Understanding DSCR loan requirements is crucial for securing financing. These loans primarily focus on a property's income potential. Lenders assess this by examining the Debt Service Coverage Ratio, or DSCR.

First, the DSCR itself is a critical requirement. Lenders typically prefer a DSCR of at least 1.25. This ensures the property generates enough income to cover debt expenses. A higher DSCR often improves loan approval chances.

Next, documentation plays a vital role. You'll need proof of rental income. This may involve submitting lease agreements and bank statements. Lenders use these to verify consistent cash flow.

Additionally, credit history matters even in DSCR loans. While personal income isn't the main focus, lenders still consider credit scores. A favorable credit score can facilitate smoother approval.

The condition of the property also influences loan decisions. Properties in good repair are preferable. This reduces the risk of unexpected maintenance expenses impacting cash flow.

Lenders may also require a certain down payment. This typically ranges from 20% to 30%. The down payment acts as a buffer for the lender, reflecting the investor's commitment.

Finally, having a comprehensive property appraisal is often mandatory. An appraisal validates the property's value and income potential. This step reassures lenders about the investment's viability. Understanding these requirements streamlines the application process, increasing success likelihood.

What Is the DSCR Instant Quote Process?

Unlike traditional loan pre-approvals that involve lengthy paperwork and credit checks, OfferMarket’s DSCR loan journey begins with an instant quote. This step takes about 1–2 minutes and does not require a credit pull, making it ideal for real estate investors comparing financing options.

To receive your quote, you’ll typically need to input basic property details such as:

Property type and location

Estimated rental income

Estimated property value or purchase price

Desired loan amount

Your estimated credit score range

This instant quote provides a preliminary interest rate, loan-to-value ratio (LTV), and loan structure. It’s not a commitment to fund, but it gives you clear insight into whether the deal qualifies and what terms to expect.

The Pre-Approval Process for DSCR Loans

Navigating the pre-approval process for a DSCR loan requires preparation. The journey begins with understanding your financial standing. This includes evaluating your credit history and score.

To get started, prospective borrowers should gather essential documents. These typically include recent tax returns, bank statements, and proof of rental income. Lenders use these to assess financial stability.

Next, contacting a lender that specializes in DSCR loans is crucial. These lenders understand the nuances of investment property financing. They can provide guidance tailored to your situation.

During the initial discussions, lenders will evaluate your Debt Service Coverage Ratio (DSCR). A DSCR of at least 1.25 is usually necessary. This measures the property's cash flow against its debt obligations.

Lenders will also look at your investment property's appraisal. An accurate appraisal confirms the property's value. It assures the lender of the asset's worth and income potential.

Once your documentation is in order, the lender proceeds with the application. They will verify all submitted information. This ensures that you meet all DSCR loan requirements.

Upon successful verification, the lender grants pre-approval. Pre-approval gives you a clearer idea of how much you can borrow. This step is crucial for planning future investment opportunities in the real estate market.

Benefits of Obtaining DSCR Loan Pre-Approval

Securing a DSCR loan pre-approval offers several advantages. First, it gives you confidence. You know exactly how much you can borrow, which aids in setting realistic property buying goals.

Pre-approval also strengthens your negotiating position. Sellers view pre-approved buyers as serious contenders. It demonstrates commitment and financial readiness, which can help in competitive market conditions.

Additionally, pre-approval saves time. It streamlines the buying process, letting you focus on properties within your reach. This efficiency reduces stress and helps to narrow down property options quickly.

Lastly, having pre-approval helps in financial planning. It provides clarity on loan terms and potential monthly payments. You can better allocate resources knowing your borrowing limit, ultimately aiding in managing your investment returns.

Note: DSCR loan “pre-approval” with OfferMarket begins with an instant quote. Final approval is only granted after underwriting review, including documentation, appraisal, and committee sign-off. Loan terms may change based on this review.

How DSCR Loans Differ from Other Investment Property Loans

DSCR loans stand apart due to their unique approval criteria. Unlike traditional loans, they rely more on property cash flow rather than the borrower's personal income. This makes them ideal for investors with inconsistent personal earnings but strong rental property performance.

Another key difference is documentation. DSCR loans often require less personal financial paperwork. Lenders focus on the property's ability to cover its debt, streamlining the paperwork process compared to conventional loans.

Additionally, DSCR loans can be more flexible in terms of credit requirements. While good credit scores still matter, lenders prioritize the property's financial health. This focus can offer more borrowing opportunities for those with lower personal credit but lucrative rental prospects.

Preparing Your Documentation for DSCR Loan Pre-Approval

Getting pre-approved for a DSCR loan requires careful preparation. The documentation you provide plays a crucial role in the lender's decision. First, ensure you have detailed records of your rental property's financial performance. This includes rental income statements, expense reports, and any existing lease agreements.

Next, focus on property appraisals. An accurate appraisal of your property is vital. It helps lenders understand the property's current market value and potential rental income. Make sure your appraisal is recent and conducted by a certified professional.

Don't overlook your credit history. While DSCR loans emphasize property cash flow, your credit score still matters. Gather any documentation that showcases your credit health, such as credit reports or proof of timely payments on other debts.

Lastly, prepare a comprehensive property business plan. This plan should outline how you intend to manage and maximize the property's income. Include strategies for dealing with vacancy rates and maintenance costs. A well-structured plan can significantly strengthen your application, demonstrating to lenders your capability as a real estate investor.

What Affects Your Final DSCR Loan Terms?

While DSCR is the primary underwriting metric, your final rate and loan structure are also affected by:

Credit Score of Guarantor(s): Higher scores (720+) qualify for lower rates and higher LTV. OfferMarket’s minimum is generally 660.

DSCR Ratio: A ratio of 1.2+ is ideal; some capital providers require 1.25 for lower-credit borrowers.

LTV Ratio: Lower LTV generally reduces your rate.

Prepayment Penalty Structure: Longer penalties (e.g., 5-4-3-2-1) yield lower rates.

Property Type and Location: Single-family properties and non-rural areas are favored.

Common Misconceptions About DSCR Loans

Here’s a table summarizing common misconceptions about DSCR loans and the realities behind them:

| Misconception | Reality | |

|---|---|---|

| DSCR loans are only for large-scale investors. | DSCR loans are accessible to small investors, including those with single rental properties. | |

| DSCR loans always have high-interest rates. | Interest rates can be competitive and depend on market factors, lender policies, and property potential. | |

| Extensive property portfolios are required. | A single-family rental property can qualify if it meets the lender's income and cash flow criteria. | |

| Personal credit is the main qualifying factor. | While personal credit is considered, property cash flow is the primary determinant for approval. |

Tips for Improving Your DSCR for Loan Approval

Improving your Debt Service Coverage Ratio (DSCR) can help secure loan approval more easily. Start by examining your property's operating expenses. Reducing unnecessary costs will increase your net operating income.

Consider raising rent if the market allows. Competitive rental rates can boost your income and improve DSCR. Be sure to assess tenant agreements and market rates before making changes.

Increasing occupancy rates is also crucial. Filling vacancies quickly will enhance your property's revenue stream. Use effective marketing strategies to attract reliable tenants fast.

Lastly, work on improving the property's overall profitability. Implement energy-efficient solutions or enhance the property's appeal. These steps can increase property value, boosting both your DSCR and investment potential.

Finding the Right Lender for Your DSCR Loan

Choosing the right lender for your DSCR loan involves careful research and networking. Look for lenders with a strong reputation in the real estate industry. They should have experience specifically with DSCR loans.

Consider reaching out to other real estate investors for recommendations. Networking can provide valuable insights into which lenders excel in customer service and loan flexibility. Seasoned investors often have great referrals.

Also, assess the lender's loan terms and conditions. Compare interest rates, fees, and prepayment penalties across multiple lenders. Finding a lender who aligns with your financial goals is crucial for your investment success.

Conclusion: Leveraging DSCR Loans for Real Estate Investment Success

In conclusion, DSCR loans offer a distinct advantage for real estate investors focused on cash flow. By emphasizing rental income over personal earnings, they open up financing opportunities for a wider range of investors. Understanding the pre-approval process is crucial for taking advantage of these loans.

Aligning your investment strategy with DSCR loan benefits can significantly boost your property portfolio. These loans are particularly useful for scaling investments, allowing both new and seasoned investors to expand their holdings efficiently. With the right approach, DSCR loans can become a vital part of your investment toolkit.

Ultimately, success with DSCR loans requires due diligence, strategic planning, and informed decision-making. By keeping abreast of market trends and building strong relationships with lenders, you can harness DSCR loans to grow and optimize your investments effectively. This proactive approach can pave the way to long-term wealth and stability in real estate.

Ready to Get Started?

Get your instant DSCR loan quote in just 1 minute — no credit pull, no commitment.

Know your rate, loan size, and next steps upfront.

👉 Start Your Quote Now

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.