*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Loan Qualifications: Essential Requirements for Real Estate Investors in 2024

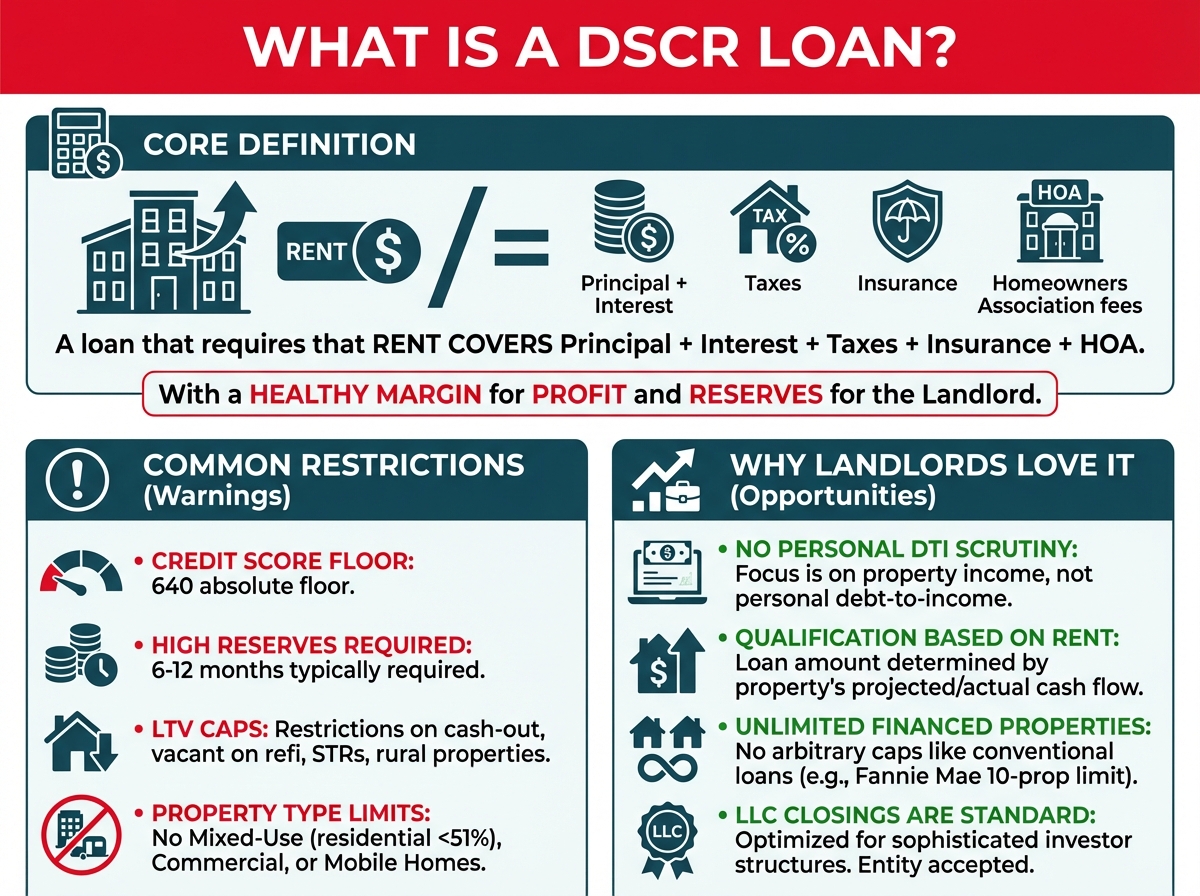

Navigating the world of real estate investment often requires creative financing solutions, and DSCR loans have become a popular choice for many investors. These loans, based on a property's Debt Service Coverage Ratio (DSCR), offer a unique approach by focusing on the cash flow generated by the property rather than the borrower’s personal income. This makes them an attractive option for those looking to expand their portfolio without traditional income verification hurdles.

Understanding the qualifications for a DSCR loan is essential for securing the funding needed to grow investments. Lenders assess specific criteria, including the DSCR calculation, credit score, and property performance, to determine eligibility. For investors, knowing what it takes to qualify can simplify the process and increase the chances of approval. Whether you're a seasoned investor or just starting out, grasping these requirements is the first step to leveraging this powerful financing tool.

What Are DSCR Loan Qualifications?

DSCR loan qualifications emphasize property cash flow and borrower creditworthiness. Meeting these criteria is essential for obtaining approval.

Debt Service Coverage Ratio (DSCR): Lenders evaluate the DSCR, which compares rental income to debt obligations. A DSCR of 1.0 or higher typically indicates the property generates enough income to cover its loan payments. For many lenders, a preferred DSCR ranges from 1.2 to 1.5.

Credit Score: Borrowers generally need a minimum credit score of 620, though some lenders may require 680 or higher for favorable terms. Strong credit profiles can result in lower interest rates and better loan conditions.

Property Type and Condition: Eligible properties often include residential rentals, multifamily units, and commercial spaces, provided they're in good condition and meet lender requirements.

Down Payment: Borrowers usually provide a down payment between 20% and 30%, reflecting the lender's risk reduction preferences. Properties with higher DSCR may qualify for smaller down payment requirements.

Cash Reserves: Lenders expect borrowers to maintain cash reserves equivalent to six months of loan payments, ensuring financial stability during potential vacancies or unexpected costs.

Accurately assessed DSCR loan qualifications improve approval likelihood and help investors understand loan terms tailored to their needs.

Key Factors Lenders Consider

Lenders use specific criteria to evaluate a borrower's eligibility for a DSCR loan. These factors help determine the risk and feasibility of approving the loan.

Debt Service Coverage Ratio

Lenders prioritize the Debt Service Coverage Ratio (DSCR) when assessing loan eligibility. This ratio measures rental income against the property's debt obligations, including principal and interest. Ratios between 1.2 and 1.5 often meet approval standards, as they indicate positive cash flow. A higher DSCR can strengthen a borrower's application, showcasing the property's financial stability.

Credit Score Requirements

Borrowers require a credit score of at least 620, though higher scores may unlock better interest rates and terms. Lenders consider credit history to assess financial reliability and repayment ability. Scores above 700 can contribute to more favorable loan evaluations, reducing perceived lending risk.

Income Documentation

Traditional income verification isn't necessary for DSCR loans, making them attractive to investors with non-conventional income sources. Lenders focus on the property's income potential instead of personal earnings. Borrowers bypass tax returns, pay stubs, or W-2 forms while providing property-related financial details like rent rolls or lease agreements.

Property Eligibility Criteria

Property eligibility plays a critical role in securing a DSCR loan, as lenders heavily evaluate the type, location, and market value of the property. These factors directly impact the property's ability to generate sufficient cash flow.

Types Of Properties Acceptable

Lenders approve a variety of property types for DSCR loans, provided they exhibit income-generating potential. Commonly accepted properties include:

- Residential Rentals: Single-family homes or condos leased to tenants.

- Multifamily Units: Duplexes, triplexes, or larger apartment complexes housing multiple tenants.

- Commercial Spaces: Office buildings, retail shops, or warehouses generating rental income.

- Short-Term Rentals: Properties listed on platforms like Airbnb, subject to lender-specific guidelines.

Properties should be in good condition and meet the lender's appraisal requirements for occupancy and market rent potential.

Location And Market Value

Location determines a property's likelihood of generating profitable rental income. Properties in areas with high rental demand or economic growth often receive stronger lender approval.

Market value influences both the loan amount and the DSCR calculation. Lenders rely on appraisals to confirm current market conditions and ensure the property supports the requested loan. Borrowers may face stricter eligibility for properties in rural or low-demand regions due to perceived risks of limited occupancy or declining values.

By addressing these criteria, borrowers can position their properties as viable investments under DSCR loan programs.

Common Challenges In Meeting DSCR Loan Qualifications

Securing a DSCR loan can present several challenges for borrowers focused on property investments. These challenges commonly stem from financial metrics, documentation issues, or property constraints, impacting approval prospects.

Low DSCR Scores

Low DSCR scores, typically below 1.2, restrict eligibility for DSCR loans. Lenders rely heavily on this ratio, as it demonstrates a property's ability to cover its debt obligations. A low ratio signals insufficient cash flow to meet loan payments, making the lender perceive higher risk. Borrowers with underperforming properties or properties in less competitive rental markets often face this issue. Resolving such concerns could involve increasing rental income, refinancing existing debt, or reducing operating expenses to boost the DSCR.

Insufficient Documentation

While traditional income verification isn't required for DSCR loans, missing property-related documents can impede loan approval. Essential documents, such as rent rolls, current lease agreements, or property management history, provide evidence of reliable property performance. Borrowers without these records appear less credible to lenders evaluating potential risk. Ensuring thorough preparation, including accurate financial statements and complete rental histories, can mitigate these challenges significantly.

Tips For Improving Your DSCR Loan Application

Optimizing your DSCR loan application can increase approval odds and secure more favorable loan terms. Focus on improving financial metrics and ensuring documentation accuracy to strengthen your application.

Enhancing Financial Ratios

Improving the Debt Service Coverage Ratio (DSCR) boosts loan eligibility. Borrowers can achieve this by increasing rental income or reducing operational expenses. For instance, revising rent agreements to reflect market rates or upgrading property conditions to attract premium rents can elevate income figures. Lowering costs, such as negotiating more affordable property management fees or utility expenses, also improves cash flow. Maintaining a DSCR of 1.2 or higher aligns with most lenders' requirements, with 1.4 or higher offering stronger leverage during negotiations.

Organizing Required Documents

Accurate documentation expedites DSCR loan evaluations. Documents like rent rolls, lease agreements, operating expense reports, and property appraisals provide key information for lenders. Rent rolls should outline tenant payments and property vacancy details, while lease agreements confirm ongoing rental income. Providing a detailed expense sheet ensures transparency in financial obligations. Property appraisals, confirming market value, contribute to precise DSCR calculations. Submitting these in an organized format reduces processing delays and solidifies the application.

Conclusion

DSCR loans offer a powerful financing option for real estate investors seeking flexibility and a focus on property performance. By understanding the key qualifications and preparing thoroughly, borrowers can position themselves for success. Strong financial metrics, well-documented property details, and strategic planning can significantly enhance approval chances. With the right approach, investors can leverage DSCR loans to expand their portfolios and achieve long-term growth.

Frequently Asked Questions

What is a DSCR loan?

A DSCR loan, or Debt Service Coverage Ratio loan, is a type of real estate financing that evaluates a property's cash flow rather than the borrower's personal income. It’s ideal for investors who want to expand their portfolios without relying on traditional income documentation.

What credit score is required for a DSCR loan?

Most lenders require a minimum credit score of 620 for a DSCR loan. However, a higher credit score, typically above 700, can help you qualify for more favorable terms.

What properties are eligible for a DSCR loan?

Eligible properties include residential rentals, multifamily units, commercial spaces, and short-term rentals. These properties must be in good condition and demonstrate income-generating potential.

What is the minimum Debt Service Coverage Ratio (DSCR) required?

Lenders generally prefer a DSCR of at least 1.2. A higher ratio, such as 1.4 or above, can provide better loan terms and approval chances.

Is personal income verification required for a DSCR loan?

No, personal income verification is not required for DSCR loans. Instead, the focus is on the property’s financial performance, such as rental income and debt obligations.

What is the typical down payment for a DSCR loan?

Borrowers are usually required to provide a down payment of 20% to 30% for DSCR loans. Higher down payments may lead to better loan terms.

How can I improve my chances of qualifying for a DSCR loan?

To improve your chances, maintain a DSCR of at least 1.2, optimize rental income, reduce operational expenses, and prepare thorough documentation like rent rolls, lease agreements, and property appraisals.

What challenges might I face when applying for a DSCR loan?

Common challenges include low DSCR scores (below 1.2), underperforming properties, or incomplete documentation such as missing rent rolls or lease agreements. Proper preparation can help mitigate these issues.

Why is location important for a DSCR loan?

Location plays a key role in determining a property's rental income potential. Lenders prefer properties in high-demand areas, as these are more likely to generate stable cash flow.

Are DSCR loans suitable for beginner investors?

Yes, DSCR loans can be a great option for beginner investors as they focus on property performance rather than personal income. However, understanding the requirements and preparing accurate documentation is crucial.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull