*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Loans for Short Term Rentals

Last updated: Jan 8, 2025

DSCR loans for short-term rentals might sound like a mouthful. But don't let the jargon intimidate you.

In the world of real estate investing, these loans are a game-changer. They're a financial tool that can help you grow your rental property portfolio.

But what exactly are DSCR loans?

DSCR stands for Debt Service Coverage Ratio. It's a type of loan that's specifically designed for rental property investors.

Unlike traditional mortgages, DSCR loans focus on the income your rental property generates. This makes them a great fit for short-term rentals, which can often bring in higher income than long-term leases.

In this guide, we'll demystify DSCR loans for short-term rentals. We'll break down how they work, their benefits, and how you can use them to your advantage.

Whether you're an aspiring real estate investor or a seasoned professional, this guide will provide you with valuable insights. So, let's dive in and explore the world of DSCR loans for short-term rentals.

Understanding DSCR Loans

Diving into DSCR loans requires grasping what they fundamentally represent. In essence, they offer a specialized financing path for real estate investors. Primarily, these loans hinge on the property's cash flow rather than the borrower’s income.

The focus here is on the Debt Service Coverage Ratio itself. Lenders use DSCR as a key metric to determine loan eligibility. By examining this ratio, they can assess how well the property's income covers its debt obligations.

A higher DSCR indicates a stronger ability to meet debt payments. This measurement provides lenders confidence in the property's ability to generate enough revenue. Let’s delve deeper into the specifics of DSCR loans.

Key Features of DSCR Loans:

- Primarily evaluate property income

- Suitable for multiple-unit properties

- Less reliance on borrower's personal income

- Considered advantageous for high-income rentals

These characteristics set DSCR loans apart from typical financing options. The focus on property income can accommodate more ambitious investment strategies. This is particularly enticing for properties with lucrative short-term rental potentials.

The DSCR loan structure streamlines the process for investors aiming at revenue-rich properties. Understanding how DSCR is calculated can further illuminate the benefits it offers.

What is a DSCR Loan?

A DSCR loan, or Debt Service Coverage Ratio loan, is distinct in real estate financing. It caters to properties that generate income, particularly through rentals.

Unlike traditional loans, it measures the income generated by the property, not the individual's salary. This makes them suitable for investors who have multiple income-generating properties.

Such loans emphasize the ratio between income and debt obligations. The higher the ratio, the more appealing the loan terms could be. This focus shifts the assessment from personal creditworthiness to property performance.

Calculating Your DSCR

Calculating your DSCR is crucial to understanding your loan eligibility. The formula is simple: divide the net operating income by the total debt service.

For example, if your property generates $100,000 and debt payments are $75,000, your DSCR is 1.33. This figure means the property generates 1.33 times the income required to cover its debts.

A DSCR of over 1.0 is often required by lenders. The higher the DSCR, the less risky your investment appears. Therefore, boosting your property's net operating income can significantly improve your loan prospects.

The Appeal of Short Term Rentals for Investors

Short-term rentals present a dynamic and profitable opportunity for real estate investors. These properties can generate significant rental income, often outpacing long-term rental rates. The flexibility to adjust pricing based on demand further enhances profitability.

Investors can capitalize on peak tourist seasons, leveraging higher nightly rates. This ability to fluctuate pricing based on occupancy and market trends offers a compelling advantage. It allows for strategic financial planning and maximized revenue streams.

Additionally, short-term rentals provide diverse tenant profiles, reducing dependency on long-term tenants. This diversity can stabilize revenue streams even if one market segment softens. Moreover, it's easier to maintain the property due to frequent cleaning schedules.

The growing popularity of platforms like Airbnb has simplified the management of these rentals. Investors enjoy increased exposure to a global audience, leading to higher booking rates. This trend underscores the sustained demand for short-term accommodations.

Ultimately, short-term rentals cater to changing traveler preferences, particularly those seeking unique and flexible lodging options. As travel norms evolve, these properties can adapt swiftly to meet diverse needs. This adaptability solidifies their position as an appealing investment.

Why Choose Short Term Rentals?

Investing in short-term rentals can be significantly more lucrative than traditional rentals. The potential to earn higher income from nightly rates is a primary draw. You can adjust rates to reflect demand, maximizing income during peak seasons.

Short-term rentals also offer flexibility in tenant selection. Investors aren't tied to long leases, allowing for frequent occupancy adjustments. This frequent turnover ensures consistent attention to property upkeep and maintenance.

Additionally, these rentals appeal to a wide audience—business travelers, vacationers, and more. The variety of potential guests can lead to more consistent occupancy rates. In turn, this consistency often translates to steadier financial returns.

Economic Factors Affecting Short Term Rentals

The success of short-term rentals is closely linked to economic trends. Local and global economic conditions can significantly influence demand and pricing strategies. In thriving economic times, travel increases, boosting short-term rental demand.

When economic downturns occur, discretionary spending can decrease, impacting bookings. Investors must be astute, leveraging economic indicators for proactive management. For example, strategies might include adjusting rates or targeting different traveler segments.

Additionally, location plays a crucial role in resilience against economic shifts. Properties in sought-after, tourist-heavy areas may weather economic fluctuations better. Understanding these economic factors enables savvy investors to optimize rental performance.

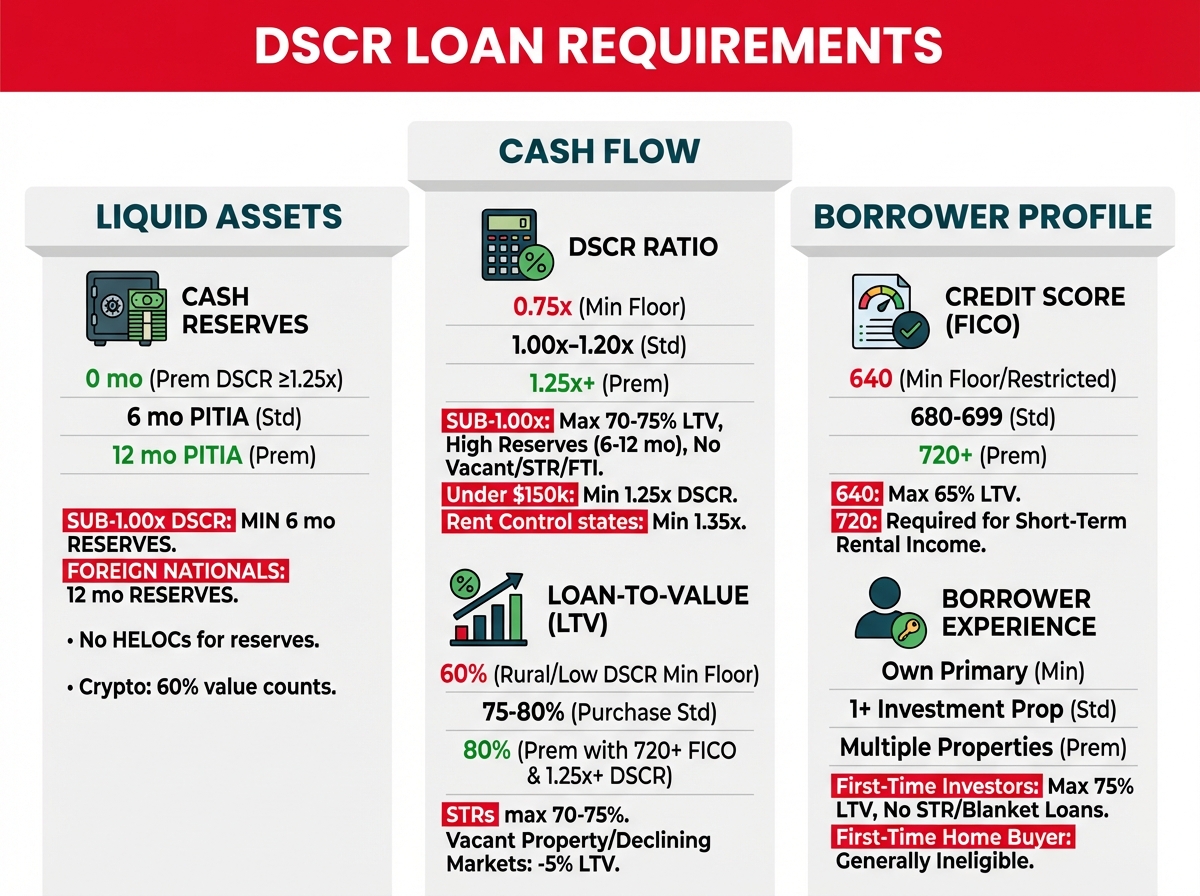

Qualifying for a DSCR Loan

Qualifying for a DSCR loan requires understanding key criteria that lenders consider essential. Unlike traditional loans, DSCR loans focus on the property’s income potential rather than the borrower's personal income. This aspect makes them particularly appealing to investors with multiple properties.

Lenders assess the property's Debt Service Coverage Ratio, ensuring it adequately covers loan obligations. A higher DSCR indicates a property's strong earning potential, easing the lender's concerns. Typically, a DSCR of 1.25 or higher is preferred to ensure expenses are comfortably met.

Applicants must provide detailed financial projections, showcasing expected rental income and operating costs. Accurate and realistic projections are crucial, as they directly impact loan approval. It's also important to maintain comprehensive records of current and projected rental income.

Common lender requirements include:

- A comprehensive business plan detailing income strategies and property management.

- Thorough documentation of rental income history or market analysis for new properties.

- Proof of ability to meet ongoing property expenses and loan repayments.

Many lenders also require evidence of property insurance and compliance with local regulations. Ensuring all legal and safety requirements are met minimizes risk in the lender's eyes. These requirements ultimately protect both lender and borrower, fostering a smoother loan approval process.

Lender Requirements for DSCR Loans

Lenders prioritize specific criteria to assess the risk associated with DSCR loans. The property's income potential often takes precedence over traditional credit metrics. Thus, borrowers should focus on showcasing robust, consistent rental income streams.

A key requirement is demonstrating sufficient cash flow to comfortably cover loan payments. Lenders typically require proof of a DSCR ratio that exceeds 1.25. This ratio indicates that rental income surpasses debt obligations by at least 25%.

Additionally, a comprehensive rental history or market analysis may be needed. This information helps to justify predicted income figures and supports the loan application. Accuracy and transparency in these reports enhance credibility and improve approval odds.

The Role of Credit Scores and Rental Income

Though DSCR loans emphasize property income, credit scores still play a significant role. They reflect the borrower’s financial management skills and overall creditworthiness. A strong credit score can facilitate favorable loan terms and smoother approval processes.

Lenders often consider the consistency and reliability of rental income as crucial metrics. Predictable income streams suggest a lower risk profile, enhancing loan appeal. It's vital for borrowers to maintain thorough documentation, such as lease agreements and occupancy records.

Finally, borrowers should strive to maximize rental income through effective management strategies. This can include optimizing occupancy rates, competitive pricing, and value-adding amenities. Doing so not only boosts loan approval chances but also strengthens long-term investment viability.

Benefits of DSCR Loans for Short Term Rentals

DSCR loans offer a range of advantages for investors in short-term rental markets. They present a unique financing option that focuses on the potential rental income rather than personal income. This is particularly beneficial for those who possess significant property experience but may not have traditional income documentation.

One of the standout benefits is the flexibility they provide. Investors can fund multiple properties, facilitating the expansion of their real estate portfolio without being constrained by traditional financial benchmarks. This freedom enables creative financial maneuvers which can yield high returns.

Moreover, DSCR loans often offer more lenient terms compared to conventional mortgages. This includes options like interest-only payments which can aid in managing cash flows during initial investment phases. Such features are invaluable when planning long-term, sustainable investment growth.

Key benefits of DSCR loans include:

- Focus on rental income rather than personal income.

- Ability to fund multiple properties simultaneously.

- Availability of interest-only payment options.

Additionally, DSCR loans can be an attractive choice for refinancing existing properties. This can lower overall costs and unlock equity to reinvest in other opportunities. It's a tool that not only supports investment diversification but also fortifies financial stability in varying market conditions.

Investors willing to capitalize on these benefits must also consider the attendant responsibilities. Effective property management and strategic market analysis remain crucial for maximizing the loan's potential. Aligning loan benefits with calculated investment strategies enhances returns while mitigating risks.

Flexibility and Portfolio Growth

DSCR loans grant a remarkable degree of flexibility, vital for proactive real estate investors. By evaluating a property's income potential, these loans align seamlessly with dynamic investment strategies focused on short-term rentals.

Their flexibility enables investors to acquire multiple properties efficiently, avoiding the limitations of traditional income verification. This frees up resources to diversify holdings, crucial for managing risk in fluctuating markets. A diversified portfolio is often more resilient, spreading potential risk across various investments.

Portfolio growth is further supported through the possibility of reinvesting cash flows. Positive cash flow resulting from strategic short-term rentals can be redirected towards new acquisitions. This process establishes a cycle of growth, enhancing both portfolio size and investment knowledge.

Refinancing and Diversification Opportunities

Refinancing through a DSCR loan can be a game-changer for short-term rental investors. It provides a pathway to restructure existing debt, usually resulting in more favorable terms. This can decrease ongoing costs, boosting profitability and freeing capital.

Access to additional capital serves as a catalyst for diversification. By tapping into the equity of current properties, investors can explore varied market segments or emerging locations. This approach enhances the breadth of an investment strategy, potentially increasing overall returns.

Furthermore, diversification through refinancing aids in mitigating risk. By spreading investments across different property types or regions, the volatility of any single market can be balanced. This strategic spread provides financial security, especially in unpredictable economic climates.

Risks and Mitigation Strategies

While DSCR loans offer numerous benefits, investors must remain vigilant about potential risks. Unforeseen market shifts or property-specific issues can impact short-term rental performance and, by extension, loan viability. Understanding these risks and preparing to counter them is crucial for any savvy investor.

Understanding the Risks

One primary risk is the fluctuating demand for short-term rentals. Factors such as seasonal tourism trends and economic downturns can drastically affect occupancy rates. High vacancy periods reduce income, which might strain a DSCR loan reliant on steady rental income.

Another risk involves regulatory changes. Local governments may alter short-term rental laws, impacting profitability or even legality. Sudden legislative changes can disrupt expected cash flows, posing financial challenges.

Property-specific risks are also significant. Maintenance issues, unexpected repairs, or poor management can negatively influence revenue. Investors must account for these inevitable risks in their financial planning to maintain stability and returns.

How to Mitigate Potential Risks

Mitigation strategies should focus on extensive research and planning. Understanding local market dynamics and potential regulatory changes is essential. Investors should remain informed about local ordinances and emerging trends that could impact their properties.

Diversifying income streams can safeguard against economic shifts. This involves not relying solely on income from short-term rentals. Exploring long-term rental options or investing across various regions can provide a buffer during market downturns.

Additionally, developing a solid financial cushion is wise. Reserves for repairs or unexpected vacancies offer peace of mind and financial stability. Having contingency plans ensures you can weather unforeseen disruptions without jeopardizing your investment’s viability.

Implementing these strategies can help investors minimize risks associated with DSCR loans. With a proactive approach, the advantages of short-term rental investments can be fully leveraged while mitigating potential downsides.

Risks and Mitigation Strategies for DSCR Loans in Short-Term Rentals

| Risk | Description | Mitigation Strategy |

|---|---|---|

| Fluctuating Demand | Seasonal trends and economic downturns can reduce occupancy rates and income. | Conduct market research and forecast demand patterns to prepare for slow seasons. |

| Regulatory Changes | Local laws may restrict or ban short-term rentals, impacting profitability. | Stay informed about local ordinances and consider alternative uses like long-term rentals. |

| Property-Specific Issues | Unexpected repairs, maintenance issues, or poor management can reduce revenue. | Maintain a financial cushion for unexpected costs and prioritize proactive property management. |

| Economic Downturns | Broader economic challenges can reduce travel demand and rental income. | Diversify income streams by investing in multiple properties or offering both short- and long-term rentals. |

| High Vacancy Periods | Periods of low occupancy may strain loan repayment. | Build a reserve fund to cover expenses during low-income months. |

Maximizing Your Short Term Rental Success

Successfully managing a short-term rental involves several key factors. It's not just about owning a property; it's about making it desirable and accessible. Ensuring your property stands out can lead to increased occupancy and profitability.

Location, Amenities, and Marketing

Location is critical in real estate, especially for short-term rentals. Properties near tourist attractions, business districts, or scenic areas often see higher demand. When selecting a property, consider the ease of access to these locations.

Amenities also play a vital role. Today's guests expect more than just a place to sleep. Consider offering high-speed internet, smart home features, and comfortable furnishings to enhance the guest experience.

Effective marketing elevates your property in a crowded market. Utilize high-quality images and compelling property descriptions to attract potential guests. Leverage online platforms and social media to reach a broader audience and showcase your unique offerings.

Managing Occupancy Rates and Guest Experience

Maximizing occupancy rates requires strategic planning. Pay attention to local events, holidays, and seasons that might influence demand. Adjusting pricing accordingly can attract more bookings and fill vacancies during off-peak times.

Guest experience is paramount for repeat business and positive reviews. Ensure smooth check-in and check-out processes, maintain cleanliness, and provide excellent customer service. Personal touches, like a welcome note or local guide, can enhance guest satisfaction.

Listening to guest feedback is another crucial aspect. Regularly update your property based on reviews and trends. By continuously improving the guest experience, you foster loyalty and encourage positive online testimonials, essential for a thriving short-term rental business.

Conclusion: Is a DSCR Loan Right for Your Investment Strategy?

DSCR loans can offer unique opportunities for short-term rental investors. Their flexibility and focus on rental income make them ideal for expanding portfolios. Evaluate your specific goals, market conditions, and risk tolerance to determine if this financing option aligns with your investment strategy.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull