*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Why Choose a Home Equity Loan from a Private Lender for Your Needs?

Last Updated: February 11, 2025

For homeowners looking to tap into their property's value, a home equity loan from a private money lender can be an appealing option. These loans allow individuals to borrow against the equity they've built up, providing them with funds for various needs like home improvements, debt consolidation, or unexpected expenses. Unlike traditional lenders, private lenders often offer more flexible terms and quicker approval processes, making it easier for borrowers to access the cash they need.

Understanding the intricacies of home equity loans is crucial for making informed financial decisions. With the right information, homeowners can leverage their equity to enhance their financial stability and achieve their goals. This article explores the benefits and considerations of choosing a private lender for a home equity loan, helping readers navigate their options with confidence.

Understanding Home Equity Loans

Home equity loans provide homeowners a way to borrow against the value of their property. These loans enable access to funds for various needs, such as home repairs or consolidating existing debt.

What is a Home Equity Loan?

A home equity loan is a type of loan where the borrower uses the equity in their home as collateral. Equity refers to the difference between the home's market value and the outstanding mortgage balance. Homeowners can typically borrow a percentage of their equity to access cash, often at lower interest rates compared to personal loans.

Key Features of Home Equity Loans

- Fixed Rates: Many home equity loans offer fixed interest rates, providing consistent monthly payments.

- Lump Sum Payment: Borrowers receive a one-time payment, making budgeting straightforward.

- Tax Benefits: Interest paid on home equity loans may be tax-deductible, depending on the purpose of the loan and IRS guidelines.

- Long-Term Repayment: Loan terms generally range from 5 to 30 years, allowing for manageable repayment schedules.

- Varied Uses: Borrowers can use funds for home improvements, education, or debt consolidation.

Understanding these features helps borrowers make well-informed financial choices when considering a home equity loan.

Comparing Private Lenders vs. Traditional Lenders

| Feature | Private Lenders | Traditional Lenders |

|---|---|---|

| Approval Speed | Fast (days) | Slow (weeks/months) |

| Credit Requirements | Flexible | Strict |

| Loan-to-Value Ratio (LTV) | Higher (up to 90%) | Lower (usually 80%) |

| Loan Terms | Customizable | Fixed, standardized |

| Paperwork & Requirements | Minimal | Extensive |

| Regulatory Oversight | Less regulated | Heavily regulated |

Private lenders provide speed and flexibility, while traditional lenders offer more stability and lower interest rates. Borrowers must weigh these factors when choosing the right lender.

The Role of Private Lenders

Private lenders play a significant role in the home equity loan market. They provide options that can benefit homeowners seeking quick access to funds based on their property's value.

How Private Lenders Work

Private lenders offer home equity loans by assessing the value of a homeowner's property. After determining the equity available, they provide loans against that equity. The process typically involves less red tape than traditional banks, enabling faster approvals. Borrowers submit required documents, such as proof of income and an appraisal of the home, for review. Once approved, the funds are available for use, allowing homeowners to finance various projects or consolidate debt.

Advantages of Using Private Lenders

- Flexible Terms: Private lenders often allow more flexibility in loan amounts and repayment periods. Borrowers can tailor their loans to fit their financial needs.

- Faster Approvals: The approval process with private lenders generally takes less time. Borrowers can often receive funds within a few days.

- Accessibility for More Borrowers: Private lenders may consider borrowers with lower credit scores than traditional lenders. This helps individuals who may not qualify for bank loans.

- Personalized Service: Many private lenders offer more direct communication and personalized attention, simplifying the borrowing experience.

- Potential for Competitive Rates: Some private lenders offer competitive interest rates, especially for borrowers with strong equity in their homes.

Comparing Private Lenders to Traditional Lenders

Private lenders offer unique features compared to traditional lenders for home equity loans. Understanding these differences helps borrowers make informed choices.

Interest Rates and Terms

Interest rates from private lenders often vary widely. These lenders may provide flexible terms that meet specific borrower needs. Homeowners could find lower rates or better repayment options depending on the lender's policies. Conversely, traditional lenders might offer more standardized rates, which may not fit every applicant's situation. Both types of lenders may charge fees, so understanding the total cost is crucial.

Application Process and Approval Times

Private lenders typically have a faster application process. Homeowners often complete applications in a few hours and receive approval in days. This speed benefits those needing urgent access to funds. Traditional lenders tend to have a more complex process, often requiring several weeks for approvals. Borrowers should assess their time frame when choosing between the two options.

Important Considerations

Considering a home equity loan from a private lender involves several key factors. Homeowners should understand both the costs associated with these loans and the potential risks involved.

Fees and Costs Associated with Loans

Fees for home equity loans can vary. Common costs include:

- Application Fee: Some lenders charge a fee to process the loan application.

- Appraisal Fee: An appraisal may be needed to determine the home's value.

- Closing Costs: These may cover various expenses like title searches and recording fees.

- Monthly Payments: Fixed interest rates typically lead to consistent monthly payments over the loan's life.

Checking these costs and comparing them with different lenders helps ensure better financial planning.

Potential Risks of Private Home Equity Loans

Before applying for a private home equity loan, homeowners should carefully evaluate potential risks. While private lenders offer quick access to funds, there are important financial implications that borrowers must consider.

1. Higher Interest Costs

Private lenders often charge higher interest rates compared to traditional banks. These rates reflect the increased risk that private lenders take by offering more flexible terms and approvals. While homeowners benefit from faster access to funds, they must calculate the total cost of borrowing to ensure it aligns with their financial goals. Borrowers should compare multiple lenders to find the most competitive rates and avoid loans with unreasonably high fees.

2. Risk of Foreclosure

Since home equity loans are secured by the borrower’s home, failing to repay the loan could lead to foreclosure. This means that if a borrower defaults on their payments, the private lender has the legal right to seize and sell the home to recover the loan amount. To minimize this risk, homeowners should borrow only what they can afford and have a clear repayment plan in place before signing any agreement.

3. Predatory Lending Practices

Not all private lenders operate ethically. Some may engage in predatory lending practices, such as:

- Charging excessive fees and penalties

- Hiding unfavorable terms in fine print

- Pushing borrowers into unaffordable loans

To avoid falling victim to such practices, borrowers must review all loan terms carefully, ask questions, and seek legal advice before finalizing an agreement.

4. Market Fluctuations

Real estate markets are subject to economic changes, and home values can decline. If a borrower takes out a large home equity loan and home prices drop, they could end up owing more than their home is worth (a situation known as negative equity). This can make it difficult to sell or refinance the home in the future. Homeowners should carefully assess market conditions and loan-to-value ratios (LTVs) before borrowing.

By understanding these risks, homeowners can make informed decisions about whether a private home equity loan is the right financial move.

Step-by-Step Guide to Securing a Home Equity Loan from a Private Lender

Securing a home equity loan from a private lender requires careful planning and strategic decision-making. Follow these steps to ensure you get the best terms and protect your financial interests.

1. Determine Your Equity

Before applying, homeowners must calculate how much equity they have in their home. The formula is simple:

Home Equity = Home’s Market Value - Remaining Mortgage Balance

Most private lenders allow borrowers to access up to 75-90% of their equity. Knowing your equity will help you set realistic borrowing expectations and avoid excessive debt.

2. Research Private Lenders

Not all private lenders offer the same interest rates, loan terms, or lending practices. Researching multiple lenders ensures you find the best possible deal. Here’s what to look for:

- Lender Reputation – Check reviews, testimonials, and Better Business Bureau (BBB) ratings.

- Interest Rates & Fees – Compare loan costs, origination fees, and penalties.

- Loan Flexibility – Look for lenders who customize repayment terms based on borrower needs.

3. Prepare Required Documents

Private lenders still require basic documentation to approve loans. Typical documents include:

- Proof of Income – Pay stubs, tax returns, or bank statements

- Property Valuation – Home appraisal or market assessment

- Mortgage Details – Information about existing loans on the property

Having these documents ready in advance speeds up the approval process and improves your chances of getting a better loan offer.

4. Negotiate Loan Terms

Many private lenders allow borrowers to negotiate interest rates, repayment terms, and fees. Key points to discuss include:

- Loan-to-Value Ratio (LTV) – Higher LTV means higher risk, which may lead to higher interest rates.

- Interest Rate Type – Fixed vs. variable rates; fixed rates provide stability, while variable rates may offer lower initial costs.

- Prepayment Penalties – Some lenders charge fees for paying off loans early—be sure to clarify these terms.

5. Get Legal Advice

Before signing any loan agreement, it’s essential to consult a financial advisor or real estate attorney. They can help review the contract, identify hidden fees, and negotiate better terms on your behalf.

6. Finalize the Loan and Use Funds Wisely

Once the loan is approved and funded, borrowers should use the money strategically—whether for home improvements, debt consolidation, or investment purposes. Responsible financial planning ensures that the loan serves as a beneficial financial tool rather than becoming a burden.

Following these steps will help homeowners secure the best possible home equity loan from a private lender while minimizing risks.

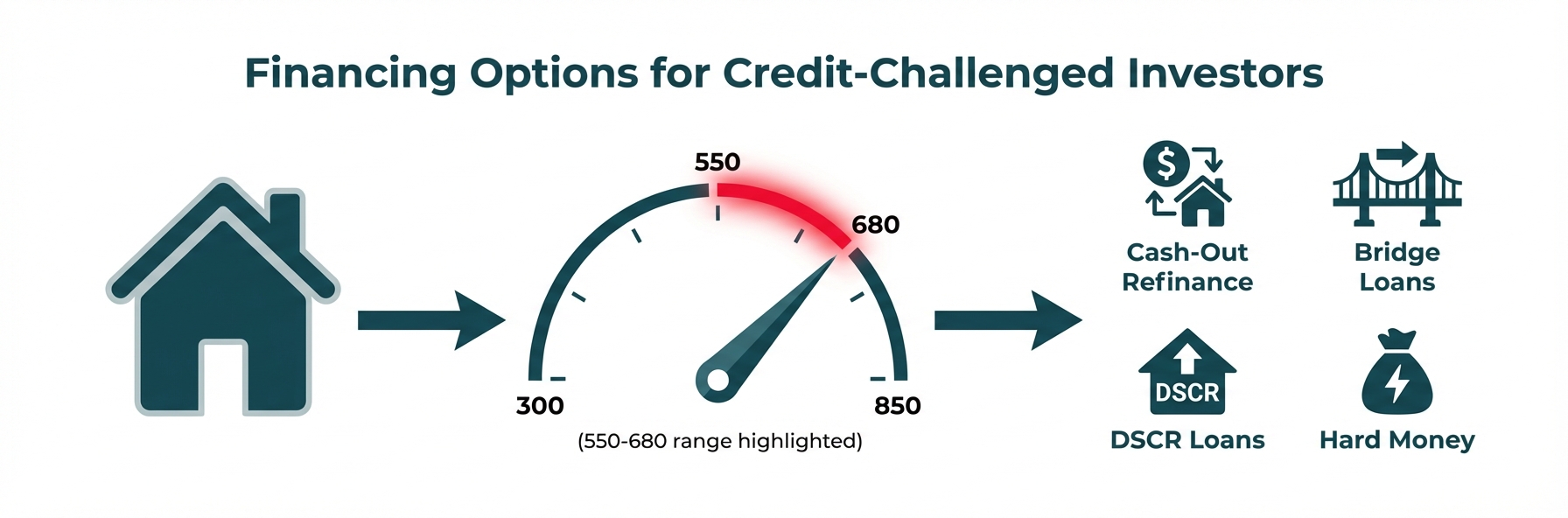

Alternatives to Private Home Equity Loans

A private home equity loan is not the only financing option available to homeowners. Depending on individual financial needs and circumstances, there may be better alternatives.

1. Home Equity Line of Credit (HELOC)

A HELOC is a revolving credit line that allows homeowners to borrow as needed, rather than receiving a lump sum upfront. Key benefits include:

- Flexible borrowing limits – Borrow what you need, when you need it.

- Lower interest rates – HELOCs usually have lower interest rates than home equity loans.

- Draw Period – Borrowers can withdraw funds for a set period (e.g., 10 years) before repayment begins.

A HELOC is ideal for ongoing expenses like home renovations, tuition payments, or emergency funds.

2. Cash-Out Refinancing

With cash-out refinancing, homeowners replace their existing mortgage with a new, larger loan. The difference between the new mortgage amount and the previous loan is given to the homeowner as cash.

Pros:

- Lower interest rates compared to private loans

- Potential tax benefits

- Longer repayment terms (up to 30 years)

Cons:

- Higher closing costs

- Risk of increasing long-term debt

- Longer approval process than private lending

Cash-out refinancing is best for homeowners who want to lock in a low-interest rate while accessing equity.

3. Personal Loans

For homeowners who need a smaller loan amount and don’t want to use their home as collateral, a personal loan can be an alternative.

Pros:

- No risk of foreclosure

- Quick funding process

- Flexible use of funds

Cons:

- Higher interest rates than secured loans

- Lower borrowing limits

- Shorter repayment terms

Personal loans are best for smaller expenses, short-term financial needs, or borrowers with strong credit.

4. Government-Backed Home Loans

Some government programs offer home equity options with favorable terms:

- FHA Title I Loans – Government-backed loans for home renovations.

- VA Home Loans – Available to eligible military personnel with low interest rates.

- USDA Rural Home Loans – For homeowners in rural areas needing home improvements.

These programs provide low-interest options but may have specific eligibility requirements.

Which Alternative is Right for You?

| Financing Option | Best For | Key Benefits |

|---|---|---|

| HELOC | Ongoing expenses | Borrow as needed, lower rates |

| Cash-Out Refinance | Large expenses | Low interest, long repayment terms |

| Personal Loan | Small expenses | No collateral required |

| Government-Backed Loans | Eligible homeowners | Lower interest rates, special benefits |

Choosing the right alternative depends on financial needs, credit history, and risk tolerance. Homeowners should evaluate all options before committing to a private home equity loan.

Conclusion

Exploring home equity loans through private lenders offers homeowners a viable pathway to leverage their property's value. With the potential for flexible terms and quicker access to funds, these loans can meet diverse financial needs effectively.

Understanding the features and risks associated with these loans is essential for making informed decisions. By carefully evaluating options and considering personal circumstances, homeowners can navigate the lending landscape confidently. Ultimately, a home equity loan from a private lender could be the key to unlocking financial opportunities while enhancing one's home and overall well-being.

Frequently Asked Questions

What is a home equity loan?

A home equity loan is a type of loan that allows homeowners to borrow against the equity they've built up in their property. It uses the home as collateral and typically offers fixed interest rates and lump sum payments.

What are the benefits of using a private lender for a home equity loan?

Private lenders often provide more flexible terms, quicker approval processes, and personalized service than traditional banks. They are also more accessible for borrowers with lower credit scores and may offer competitive interest rates.

How does the approval process differ between private and traditional lenders?

Private lenders usually have a faster application process, often completing it within hours and providing approvals in days. In contrast, traditional lenders involve more complex and time-consuming procedures, which can take weeks.

Are there risks associated with home equity loans?

Yes, potential risks include foreclosure if you fail to repay the loan, market fluctuations that may lead to negative equity, and the implications of long-term debt on future financial health. Understanding these risks is essential for informed decision-making.

What fees should I expect with a home equity loan?

Common fees associated with home equity loans include application fees, appraisal costs, closing costs, and monthly payment structures. It’s important to review these fees to understand the total cost of the loan.

How long are the repayment terms for a home equity loan?

Repayment terms for home equity loans typically range from 5 to 30 years. Borrowers should choose a term that aligns with their financial situation and repayment abilities.

Can I use a home equity loan for purposes other than home improvements?

Yes, homeowners can use a home equity loan for various purposes, including debt consolidation, educational expenses, or funding major purchases. However, it's crucial to borrow responsibly and consider the long-term impact on finances.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.