*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Private Individuals That Loan Money: Your Guide to Safe Borrowing and Personalized Terms

Among all this jugglery of finance, private individuals that loan money are becoming the more prominent figures. Quite often, these lenders enter areas that banks may not prefer; thus, they become immensely important to those seeking quick cash. Whether for personal expenses, business ventures, or emergencies, they can offer flexible terms and a more personalized approach.

With the recent rise of peer-to-peer lending platforms to more informal practices of taking loans from private individuals, it has become more critical than ever to understand the dynamics here. It is not all about how to secure an advance, but rather in identifying the risks and benefits emanating from such arrangements. The justification for private lending, the disadvantages, and how to enter these transactions with wisdom are discussed here.

Who Are Private Individuals That Loan Money?

Private individuals that loan money play a significant role in the financial ecosystem, especially when traditional lending institutions decline applications. These lenders often provide enhanced flexibility, allowing borrowers to negotiate tailored payment plans and interest rates.

Types of Private individual That Loan Money

- Friends and family provide informal loans based on personal relationships.

- Peer-to-peer lending platforms connect individual investors with borrowers.

- Private investors or venture capitalists fund business ventures with an interest in returns.

Motivations for Lending

- Personal financial gain motivates many private lenders to lend out money with interest.

- Emotional connections often drive family or friends to support personal needs or ventures.

- Investment opportunities attract people who would want to diversify their portfolios.

Benefits of Borrowing from Private Individuals That Loan Money

- Faster approval processes are available, bypassing the longer paperwork common with banks.

- Customized terms mean flexibility in repayment and interest rates accordingly.

- Financial privacy is maintained, and, therefore, transactions are discrete and less scrutinized.

Risks Involved

- Defaulting on a private loan can strain personal relationships, particularly with family or friends.

- Unregulated contracts may lack protections typically found in formal loans.

- High-interest rates could impose significant financial burdens over time.

Navigating Private Lending

- Clear communication establishes expectations for repayment and interest.

- These written agreements must clearly state the amount lent, the date of repayment, and penalties, if any, for late payment.

- Legal advice will help in explaining responsibilities and protecting both parties involved in the loan.

Understanding the dynamics of private lending enhances the borrowers' capability of making informed decisions and dealing with the relationship with their lenders.

Private Money Lenders & Online Platforms for Real Estate Investors

- OfferMarket.us – Competitive rates starting at 6.5%, fast funding for fix-and-flip, rental, and commercial projects.

- BiggerPockets Money Marketplace – Connects borrowers with private lenders for hard money and long-term loans.

- Groundfloor – Short-term, high-yield loans for residential rehabbers (non-accredited investors welcome).

- PeerStreet – Marketplace for real estate debt investments (fix-and-flip, rental loans).

- LendingHome – Hard money lender with rates from 7%, specializing in rental and flip financing.

- Patch of Land – Fast private loans for ground-up construction and rehabs.

- Fund That Flip – Short-term bridge loans (rates from 8%).

- Kiavi (formerly LendingOne) – Fix-and-flip loans with quick approvals.

- Private Lender Link – Matches borrowers with individual/hard money lenders.

- CrowdStreet – Commercial real estate debt/equity investments.

Private Individuals & Local Options

- Hard Money Meetups (Local REIA groups) – Find lenders at real estate networking events.

- Facebook Groups (e.g., "Private Money Lending USA") – Direct deals with investors.

- LinkedIn – Search "private money lender real estate" for individual contacts.

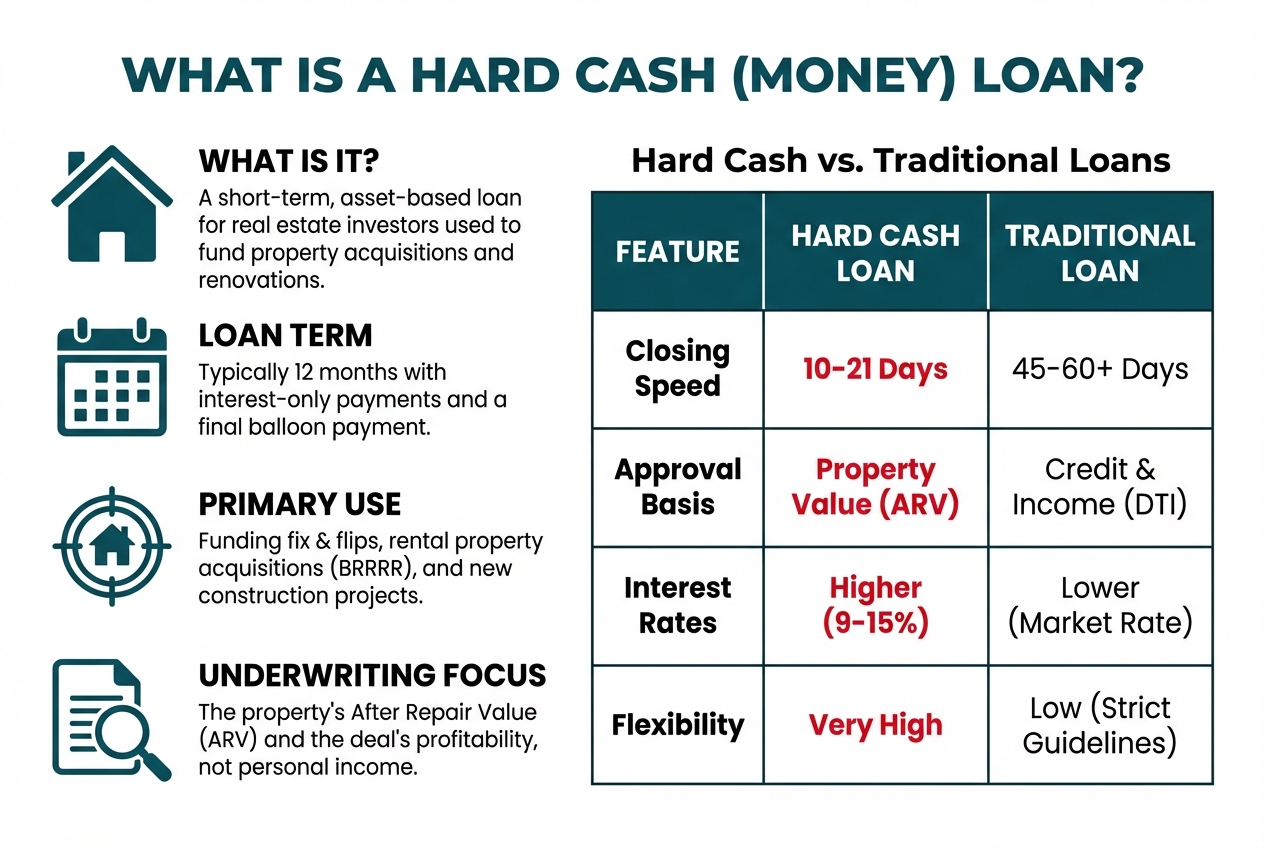

Tip: Always verify lender terms—rates vary by loan type (12–15% common for hard money).

Types of Loans Offered by Private Individuals That Loan Money

Private individuals provide loans for various purposes, which may be broadly categorized into personal loans and business loans.

Personal Loans

Personal loans from private individuals are generally used for personal needs, such as covering medical bills, financing education, or even emergency funding. The loan usually has flexible repayment terms that fit the borrower's financial capacity.

Interest rates may vary greatly depending on the assessment of the borrower's creditworthiness and relationship with the lender. Possible documentation may include proof of income and a written agreement that details terms and conditions.

Business Loans

Private individual business loans are meant for starting an entrepreneurial venture or expanding a small business. These types of loans may be needed for certain needs: to buy inventory, finance equipment, or meet operational costs. The private lenders will most likely go through the business plan regarding its viability for returns and then decide on the quantum and rate of interest.

Unlike traditional lenders, private individuals may rely more on either a personal connection or an understanding of the business rather than a strict credit evaluation. A detailed proposal that outlines the business model and repayment strategy often helps to secure such loans.

Benefits of Borrowing from Private Individuals That Loan Money

Private individual lending has a number of advantages that are quite beneficial to the borrowers. The benefits include flexibility in terms and quick access to funds.

Flexible Terms

Flexible terms characterize loans from private individuals, with the leeway to negotiate conditions that suit specific circumstances. Many private lenders will also offer customized repayment schedules based on individual financial situations.

Borrowers are often able to secure lower interest rates compared to traditional banks, especially when the lender prioritizes relationship over profit. Furthermore, private lending does not typically involve strict qualification criteria. This flexibility makes private borrowing an attractive option for those with unique financial needs.

Quick Access to Cash

Quick access to money is also another great benefit of borrowing from private individuals that loan money. The processes of approving loans through private lenders are mostly shorter than those from any other conventional facility. Fund availability can generally be arranged within 24 to 48 hours in most instances, after an agreement is reached on terms.

This goes a long way to ensure speed in certain emergencies, like bills from hospital emergencies, renovation works that cannot wait, and new business opportunities where timely movement ensures a kill. This process simplifies communication directly between the borrower and the lender, thus eliminating a lot of the time-consuming paperwork and requirements common with bank loans.

Risks and Considerations

Some aspects that are very important, though, are various risks and considerations involved when borrowing from private individuals; these are issues a borrower should, at least, be aware of. Each one of these aspects may make a big difference in the whole experience of borrowing and financial health for both parties.

High Interest Rates

Private loans usually have high interest rates. Generally speaking, private individuals that loan money measure risk in a different way from banks, a fact that drives up their interest rates. Very often, rates can range between 10% and 30%, depending on how they judge the borrower's creditworthiness and on what terms of the deal have been brokered.

For such rates, borrowers will weigh up whether their need for cash is urgent; failing to consider these rates could easily push the borrowers into insurmountable debt.

Absence of Regulation

Most private lending occurs without much regulation and can carry increased risks for the borrower. Private lenders are not traditional banks, of course, and as such, they have a leeway that the banks could only dream of because of all the strict guidelines on money dealing. This makes them susceptible to a set of unofficial, unstandardized practices in which transparency and consumer rights are minimal.

Borrowers should know that drawing up formal written agreements on clear, pre-agreed terms may protect their rights. Where an informal agreement is made with no papers or documentation of the contract, disputes arise quite frequently which may be entangled in legal tussles.

Legal Considerations When Dealing with Private Individuals That Loan Money

Borrowing from private lenders might feel less formal than dealing with a bank, but the legal aspects are just as important—if not more. A clear understanding of the legal framework is essential to protect both you and the lender from potential disputes.

1. Draft a Comprehensive Loan Agreement

Every private loan should start with a detailed written agreement. This document should outline all critical details, including the loan amount, interest rate, repayment schedule, penalties for late payments, and any collateral involved. Both parties should review the agreement thoroughly before signing, ensuring everyone is on the same page.

2. Understand State Regulations

Lending laws vary by state, and it’s crucial to know how they apply to private loans. For instance, most states have usury laws that cap the maximum interest rates lenders can charge. Ignoring these regulations could render your agreement invalid or leave you vulnerable to legal action. Research the rules in your area or consult with a legal expert to ensure compliance.

3. Include Collateral Terms

If the loan is secured with collateral, such as a property or other asset, the agreement should clearly state what happens if you default. For example, does the lender take ownership of the asset immediately, or is there a grace period? Specifying these terms upfront protects both parties and avoids confusion.

4. Seek Legal Advice

Before finalizing any loan agreement, consult with an attorney who specializes in real estate or finance. They can review the terms to ensure they’re fair, legal, and aligned with your financial goals. This step might seem like an extra expense, but it’s a worthwhile investment in avoiding costly disputes later.

5. Ensure Proper Documentation

All aspects of the transaction—payments, interest calculations, and any changes to the agreement—should be documented and signed by both parties. Keeping detailed records protects you from potential misunderstandings and provides evidence if a dispute arises.

6. Consider Mediation Clauses

Including a mediation or arbitration clause in your agreement can provide a structured way to resolve conflicts without resorting to costly litigation. This approach can save time, money, and strain on personal relationships.

How to Negotiate Terms with Private Lenders That Loan Money

Negotiating with a private lender doesn’t have to feel intimidating—it’s about finding common ground and building trust. With the right approach, you can create a fair agreement that benefits both sides and sets you up for success.

1. Come Prepared

Imagine yourself in the lender’s shoes. Wouldn’t you want to see a clear plan? Before the conversation, outline exactly how much you need, how you’ll use the funds, and your strategy for paying it back. A detailed repayment plan shows you’re serious and reduces any doubts about your ability to follow through.

2. Aim for a Win-Win Outcome

Lenders want to feel confident their money is secure, and you want terms that fit your goals. Focus on creating an agreement that works for both of you. Be flexible, but don’t agree to terms that stretch you too thin. A fair deal strengthens trust and builds a long-term relationship.

3. Back Up Your Requests with Research

Know your market. Before negotiating, research typical private lending terms in your area. What are the usual interest rates? How are repayment schedules structured? Use this information to show your lender that your proposals are reasonable and based on solid facts.

4. Be Transparent

Honesty goes a long way. If there are risks—like unexpected delays or challenges—acknowledge them upfront. Explain how you’ll manage those situations. Transparency shows your lender you’re trustworthy, which is often just as valuable as a good credit score.

5. Treat it Like a Business Deal

Even if your lender is a friend or family member, keep things professional. Draft a formal agreement, clearly define repayment terms, and ensure everything is in writing. This eliminates misunderstandings and keeps the relationship intact.

Conclusion

Funds from private individuals that loan money come with both benefits and challenges.. Borrowers from private lenders should ensure clear communication with the other party and thoroughly documented agreements to protect the borrower's interests. While it is true that the flexibility of private loans, along with speed, can instantly alleviate financial burdens, the corresponding risks cannot be ignored either.

Understanding the motives for private lending and the possible pitfalls may further equip borrowers with the ability to make informed decisions. A private lending relationship can be productive and respectful, provided advantages are weighed against risks carefully. The balance between urgency and prudence lies in meeting financial needs without sacrificing personal relationships or long-term stability.

Frequently Asked Questions About Private Individuals That Loan Money

Who are private lenders?

Private lenders are those individual lenders or groups that extend loans outside of conventional banks. These may include friends, relatives, or even investors across a peer-to-peer platform. Moreover, they also offer more flexible terms and quicker access to funds.

What are the benefits of borrowing from private individuals?

Borrowing from private individuals can provide quicker approval, customized repayment plans, and greater financial privacy. It's often easier to negotiate terms that suit your needs, making it ideal for urgent or unique financial situations.

What types of loans do private lenders offer?

Private lenders typically offer personal loans for expenses like medical bills and education, as well as business loans for entrepreneurial ventures. Each type may have varying terms based on the lender’s assessment of the borrower's situation.

What are the risks of private lending?

The risks include high interest rates from 10% to 30%, and the strain of personal relationships. Private lending is also not regulated, making clear written agreements important between the parties.

How can I effectively navigate private lending?

To navigate private lending effectively, maintain clear communication with your lender, create written agreements outlining loan terms, and seek legal advice if needed. This helps clarify responsibilities and protects both lenders and borrowers from potential disputes.

How can I find private money lenders for real estate?

You can find private money lenders through networking in real estate circles by attending meetings, seminars, or workshops. Other online platforms include LendingHome and PeerStreet, which introduce different types of lenders. The more you build a relationship and present your investment plan, the higher your chances of becoming a borrower.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull