*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Private Mortgage: Pros, Cons, and How to Choose the Right Lender for Your Investment

Last Updated: March 20, 2025

If you're a real estate investor looking to grow your business, understanding private mortgages can open up new opportunities. Whether you're focused on rental properties or flipping homes, private mortgages offer a flexible alternative to traditional bank loans. They can be an excellent solution when speed or unique financing terms are crucial to closing a deal.

Private mortgages are loans provided by individuals or private lenders, making them ideal for investors who may not meet strict bank requirements. This article will guide you through the basics, benefits, and potential risks of using private mortgages in your real estate ventures. By the end, you'll have the insights needed to decide if this financing option aligns with your investment goals.

What Is A Private Mortgage?

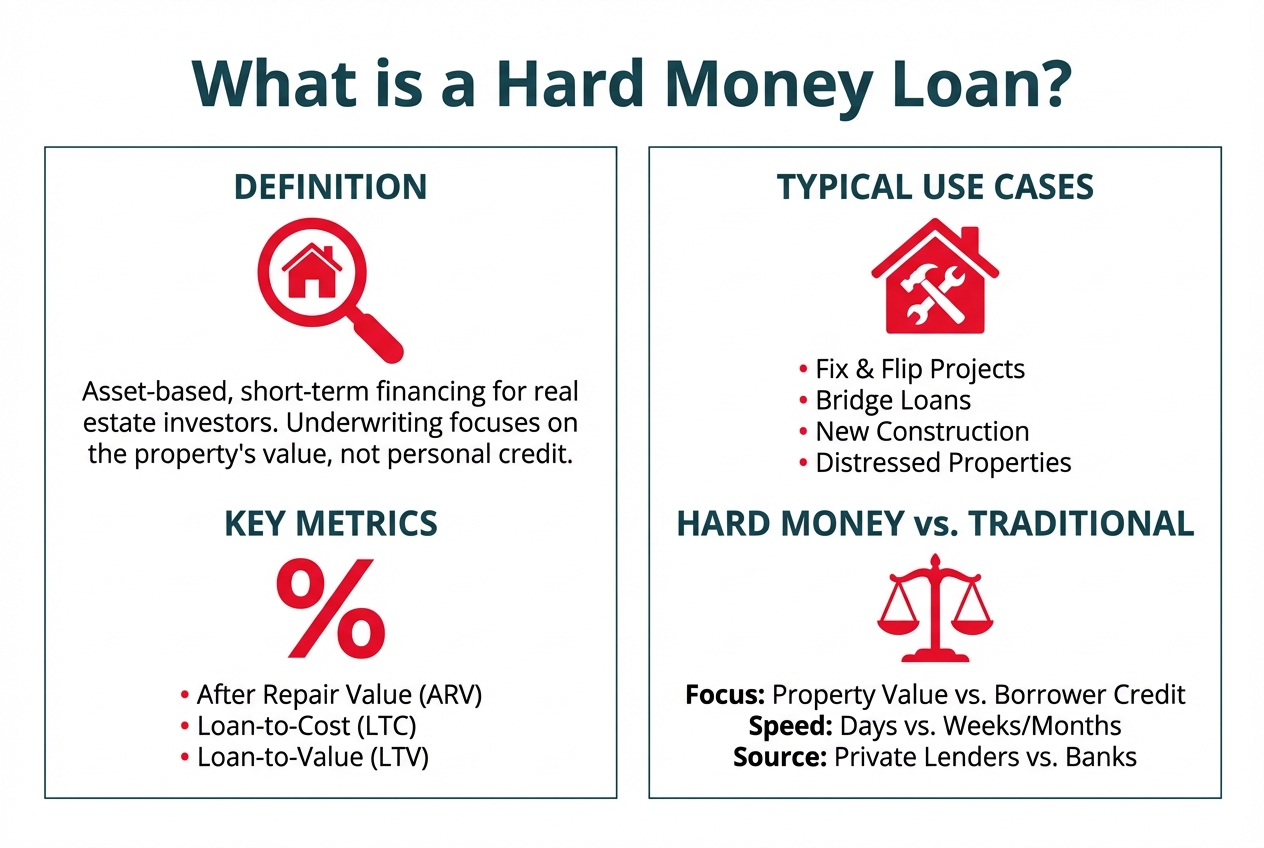

A private mortgage is a loan provided by a private individual or company instead of a traditional financial institution like a bank or credit union. This type of financing is common among real estate investors, particularly those investing in rental properties or house flipping. A private mortgage offers flexible terms and quicker access to funds, which can be beneficial when conventional lending options aren't available.

Private lenders, including private money lenders and hard money lenders, fund these loans. They base their decisions on the property's value rather than your credit score or income. Hard money loans, a subset of private mortgages, often include higher interest rates but shorter repayment terms, making them ideal for short-term investments or time-sensitive transactions like property auctions.

Private mortgages are structured based on mutual agreement between you and the lender. This can involve interest-only payments, repayment schedules tailored to your financial goals, or even balloon payments at the loan's end. For example, if you're purchasing a property to flip, a short-term private mortgage could cover renovation costs and allow repayment after selling the property.

Unlike traditional mortgages, private mortgages can close quickly, sometimes within days. Hard money lenders focus on the collateral—the property itself—rather than your financial background. This makes private mortgages accessible if you lack a strong credit history or if standard underwriting processes don't meet your timeline.

Keep in mind that private mortgages typically require higher down payments, ranging from 20% to 30% or more. The approval process is less regulated, which can result in more flexible terms but also higher risks. If you default on the loan, the private lender can seize the property to recover their investment.

Private mortgages fill a critical gap in financing for investors who need alternative solutions. Their quick processing and lenient approval criteria make them a popular choice for those pursuing real estate opportunities that demand speed and adaptability.

How Does A Private Mortgage Work?

A private mortgage operates as an alternative form of real estate financing. In this setup, a private lender, such as an individual or company, provides funds secured by the property instead of relying on stringent bank regulations.

Key Features Of Private Mortgages

1. Flexible Terms: Private mortgages often include customized repayment schedules tailored to your investment strategy. For instance, interest-only payments might be an option for short-term projects like home flipping.

2. Asset-Based Decisions: Instead of analyzing your credit score or financial history, private lenders focus on the property's value. This makes private mortgages attractive to borrowers with lower credit scores.

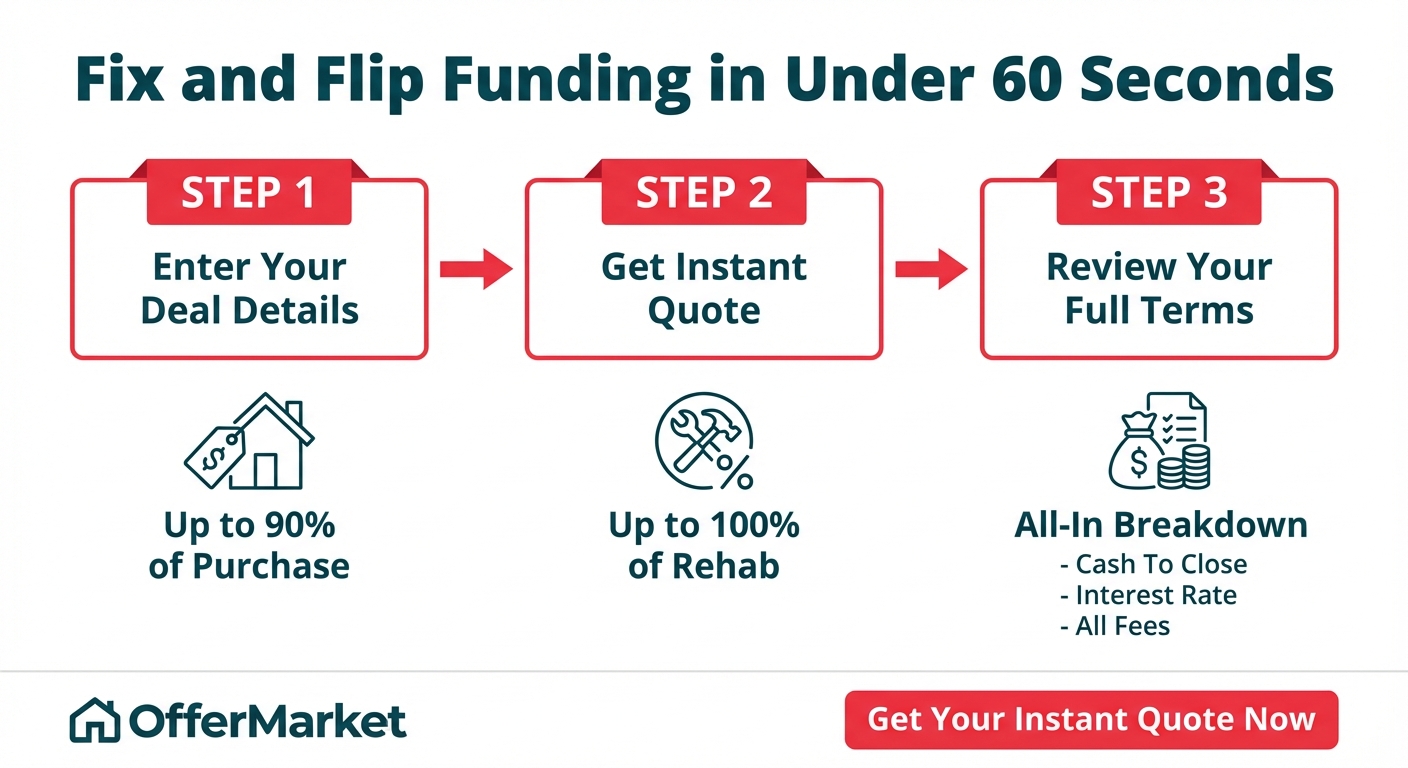

3. Quick Approval Process: Private mortgages can close in a matter of days, offering faster access to funds. This expedited process is ideal for competitive scenarios, such as real estate auctions.

4. High Interest Rates: Private lenders charge higher interest rates than traditional loans to offset the increased risk. Rates may range from 8% to 15%, depending on the lender and property.

5. Larger Down Payments: You’re typically required to provide a down payment of 20%-30% or more, particularly if the borrower-risk profile is higher than standard.

Private mortgages cater to unique financial needs, such as funding renovations or acting as bridge financing, offering solutions traditional lending fails to support.

Differences Between Private Mortgages And Traditional Mortgages

1. Approval Requirements: Traditional mortgages rely heavily on your credit score, income, and debt-to-income ratio. Private mortgages prioritize the value of the property over these factors.

2. Interest Rates: While traditional mortgage rates range from 4%-7%, private mortgage rates are significantly higher, often between 8% and 15%, reflecting the additional lender risk.

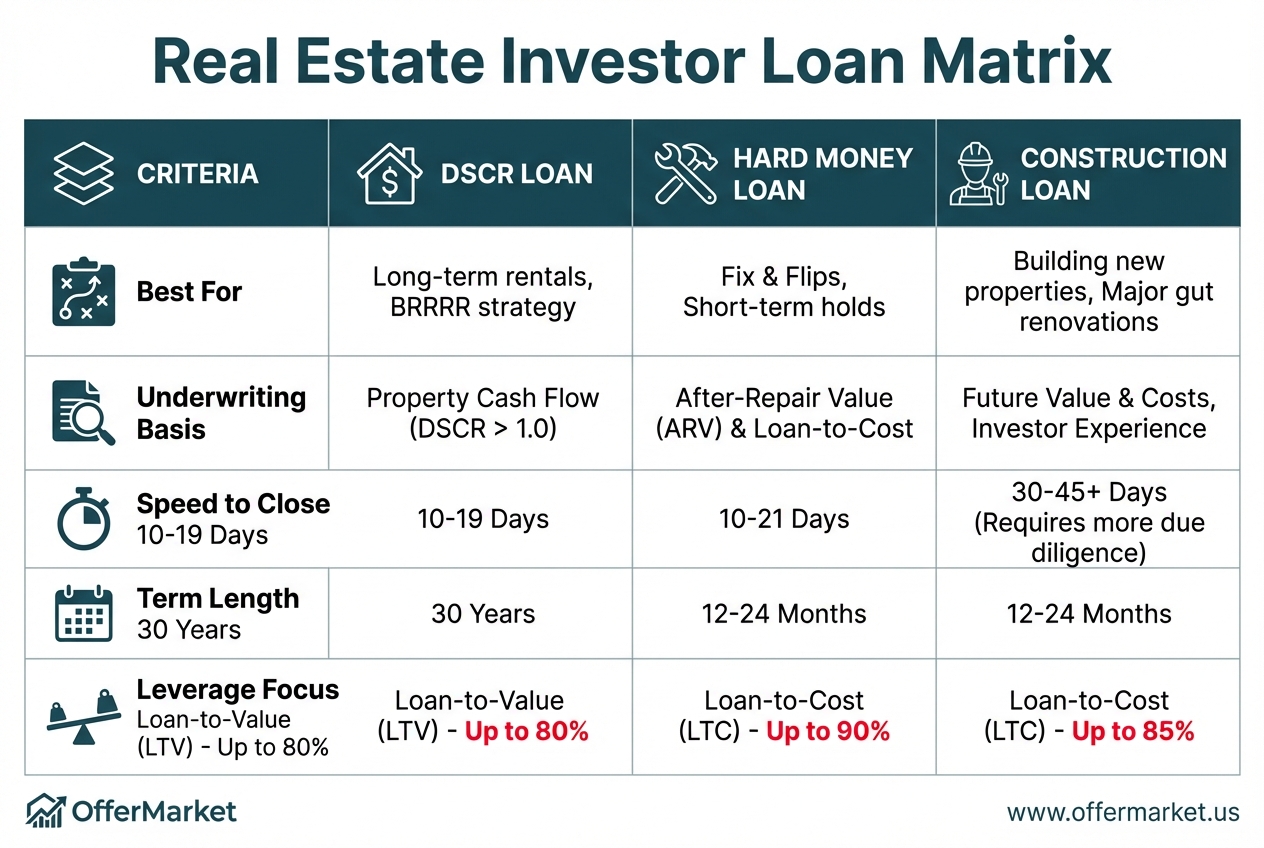

3. Loan Term: Traditional mortgages typically span 15-30 years, while private mortgage terms are shorter, lasting 6-36 months, aligning with short-term investment goals.

4. Funding Speed: It can take weeks or months to secure traditional financing, while private lenders, including hard money lenders, can fund loans within days.

5. Regulations: Traditional mortgages follow strict industry regulations. Private lenders operate more flexibly, making it easier to negotiate terms based on your requirements.

Private mortgages are ideal for real estate investors or borrowers dealing with slower traditional loan approvals and strict qualification criteria.

| Feature | Private Mortgage | Traditional Mortgage |

|---|---|---|

| Approval time | Days | Weeks–Months |

| Down payment | 20–30%+ | 3–20% |

| Interest rate | 8–15% | 4–7% |

| Loan length | 6–36 months | 15–30 years |

| Credit needed | Low | High |

| Eligible properties | Distressed, commercial, vacant | Standard residential |

Pros And Cons Of Private Mortgages

Understanding the benefits and drawbacks of private mortgages helps you make informed financial decisions when considering alternative funding options.

Advantages Of Private Mortgages

1. Flexible Terms

Private lenders, including private money and hard money lenders, offer customized loan terms not bound by traditional banking regulations. This flexibility enables adjustments to repayment schedules and interest structures to suit your investment strategy, like interest-only payments for short-term needs.

2. Quick Approval And Funding

Private mortgages provide faster access to funds, often closing within days compared to weeks or months for traditional loans. This speed makes them ideal for real estate investors in competitive markets or those purchasing properties at auctions.

3. Asset-Based Lending

Your loan approval relies on the property's value rather than your credit score or income. For instance, hard money loans from a private lender consider the after-repair value (ARV) of a property, making them attractive for home flipping projects.

4. Opportunities For Non-Traditional Borrowers

You can secure private mortgages even with poor credit history or inconsistent income, provided sufficient down payments or collateral are provided. This creates possibilities for borrowers excluded by conventional lenders.

5. Broad Property Eligibility

Unlike traditional loans, private mortgages often apply to diverse property types such as distressed properties, vacant land, or commercial buildings, which banks may avoid financing.

Potential Downsides To Consider

1. Higher Interest Rates

Interest rates for private mortgages typically range from 8-15%, exceeding those of traditional loans. For example, hard money loans often have rates significantly higher to compensate for the risks taken by private lenders.

2. Shorter Loan Terms

Most private mortgages have repayment periods under one year, requiring you to secure refinancing or sell the property quickly to meet these deadlines. Failure to do so might result in financial strain.

3. Larger Down Payments

Private lenders generally ask for 20-30% as a down payment to reduce their risk. In some cases, such as hard money loans, it may go beyond 30%, making these loans less accessible for those lacking substantial upfront cash.

4. Risk Of Property Seizure

If you default, there’s a high chance of losing the collateral property without leniency, since private mortgages prioritize protecting the lender’s interests.

5. Limited Regulatory Protection

Private money lending operates with minimal government oversight. You’ll bear the responsibility for thoroughly assessing the agreement since you won’t receive the same consumer protections as traditional financing.

Understanding these factors positions you to weigh the benefits against the risks and choose the most suitable private mortgage solution for your situation.

Who Should Consider A Private Mortgage?

Private mortgages are an option for specific borrowers who require fast funding or do not meet traditional mortgage requirements. These individuals benefit from the flexibility and fast approval processes that private lenders, including private money lenders and hard money lenders, offer.

Real Estate Investors

As a real estate investor, you might find private mortgages suited to your needs, especially for short-term projects. If you’re focused on house flipping, buying undervalued properties, or rental property investments, private funding offers quick access to capital. A private mortgage provides significant speed advantages when competing in a dynamic real estate market.

Borrowers With Poor Credit

If you have poor credit but own substantial equity in a property, a private mortgage can provide financing where traditional lenders decline. Unlike traditional loans, private mortgage approvals are based more on property value and less on credit scores or financial history. Hard money loans, a subtype of private mortgages, are ideal for individuals with limited credit options, offering funding despite unconventional borrower profiles.

Self-Employed Borrowers

Self-employed individuals often encounter difficulties qualifying for conventional mortgages due to inconsistent income verification. Private lenders rely on asset-based considerations, helping you bypass the stringent income documentation requirements tied to traditional mortgages, making this type of loan appealing if you're self-employed.

Buyers Requiring Quick Closings

If timing is critical, such as purchasing auctioned properties or seizing time-sensitive opportunities, private mortgages deliver. With faster approval processes compared to traditional mortgages, you gain access to funds within days, avoiding the delays normal lending processes entail. This is often the case for hard money loans, which focus on closing speed.

Individuals With Unique Property Types

If you’re investing in non-traditional or unconventional property types that don’t meet conventional mortgage criteria, private money lenders may be more accommodating. Properties such as mixed-use buildings, unconventional residences, or off-grid homes often fall outside the scope of traditional lending requirements but remain viable for private mortgages.

High-Net-Worth Buyers Seeking Customized Terms

As a high-net-worth buyer, private mortgages can offer customized terms like tailored repayment schedules or interest-only options. You may leverage this flexibility for personal or investment purposes, benefiting from terms specifically suited to your financial strategy.

Borrowers Unable to Meet Down Payment Standards

If you face challenges meeting the down payment standards of traditional loans, private lenders might offer alternative arrangements suited to your financial situation. Although private loans involve higher risk and often require a significant equity stake, tailored terms can still make them viable in unique circumstances.

How To Find A Private Mortgage Lender

Searching for a private mortgage lender requires research and a thorough understanding of their practices. You can find a lender that fits your needs by focusing on their reliability, terms, and experience.

Questions To Ask A Private Mortgage Lender

1. What types of loans do you offer?

Ask about the specific types of loans they provide, such as private money loans or hard money loans. This helps you determine if their offerings match your needs.

2. What are your interest rates and fees?

Understand the interest rates, repayment terms, and fees involved. Private lenders often charge higher rates than traditional institutions.

3. What is your approval process?

Ask about the timeframe for approval and the criteria they use. Private lenders typically base decisions on the property's value.

4. What are your loan terms?

Inquire if they provide short-term loans, interest-only payments, or other repayment options. Tailored terms may cater to different investment strategies.

5. Do you have experience with similar projects?

Choose a lender who’s familiar with your type of property or investment. This can ease communication and understanding throughout the process.

Tips For Ensuring A Safe Agreement

1. Verify licensing and track record.

Check if the private lender or hard money lender holds proper licensing and has positive reviews or references. A reputable lender builds trust.

2. Have an independent appraisal.

Ensure the property’s value is independently verified. This protects you from overfinancing or inflated costs.

3. Get legal advice before signing.

Hire a real estate attorney to review the agreement for clauses that might increase risks, such as unfavorable repayment schedules or unclear penalties.

4. Understand the loan terms fully.

Break down and analyze repayment schedules, interest rates, and penalties. Verbal guarantees should match what's documented.

5. Set realistic repayment expectations.

Only agree to payments and terms you’re confident your investment income or budget can cover. Avoid risk of default.

Key Takeaways

- Private mortgages provide flexibility in terms and faster approval than traditional loans, making them ideal for real estate investors and non-traditional borrowers.

- Approval focuses on property value rather than credit history, making private mortgages accessible for those with poor credit or inconsistent income.

- Higher costs and risks are involved, including higher interest rates (8%-15%), larger down payments (20%-30%), and stricter default penalties such as property seizure.

- Private mortgage terms are shorter, typically ranging from 6-36 months, aligning with short-term investment strategies like home flipping or renovations.

- Unique properties are eligible, including distressed or unconventional properties that may not qualify for traditional loans.

- Choosing a reliable private lender is crucial—ensure proper licensing, experience with similar projects, and legal review of terms before committing.

Conclusion

Private mortgages can be a powerful tool for real estate investors or buyers with unique financial needs. Their flexibility, speed, and tailored terms make them an attractive option when traditional financing isn't feasible. However, they require careful consideration due to higher costs and risks.

By understanding how private mortgages work and evaluating lenders thoroughly, you can make informed decisions that align with your goals. Whether you're pursuing short-term investments or need quick funding, a private mortgage could be the solution you're looking for—if approached wisely.

Frequently Asked Questions

What is a private mortgage?

A private mortgage is a loan provided by a private individual or company, rather than a traditional bank. It offers faster approval processes, more flexible terms, and is primarily based on the value of the property instead of the borrower's credit score or income.

Who can benefit from a private mortgage?

Private mortgages are ideal for real estate investors, individuals with poor credit but significant equity, self-employed borrowers with income verification challenges, and buyers needing quick closings or financing for unique property types.

How are private mortgages different from traditional mortgages?

Unlike traditional mortgages, private mortgages have quicker approval, more flexible terms, and less regulatory oversight. However, they typically come with higher interest rates, larger down payments, and shorter loan terms.

What are the advantages of private mortgages?

Key benefits include flexible repayment options, fast funding, no reliance on traditional credit checks, accommodation of unique property types, and tailored loan terms for specific borrower needs.

What are the disadvantages of private mortgages?

Downsides include higher interest rates, larger required down payments, the risk of property seizure in case of default, shorter repayment periods, and limited regulatory protections.

How quickly can a private mortgage be approved?

Private mortgages can often be approved within days, thanks to their less regulated and streamlined process, making them suitable for time-sensitive investment opportunities.

What questions should I ask a private mortgage lender?

Ask about loan types offered, interest rates and fees, required down payments, the approval process, loan terms, and any penalties for early repayment.

How do I find a reliable private mortgage lender?

Research the lender’s experience, reputation, and licensing. Verify their loan offerings, terms, and fees, and check for reviews or referrals from other investors.

What steps should I take to ensure a safe private mortgage agreement?

To ensure safety, verify the lender’s licensing, obtain an independent property appraisal, consult legal professionals, fully understand the loan terms, and ensure realistic repayment expectations.

Are private mortgages suitable for long-term investments?

Private mortgages are generally better for short-term investments due to their higher interest rates and shorter loan terms. Long-term projects might be better suited for traditional financing.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull