*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

What is a DSCR Loan?

Last Updated: February 26, 2026

A Debt Service Coverage Ratio (DSCR) loan is a financing tool built specifically for real estate investors looking to purchase or refinance non-owner-occupied investment properties. Forget the traditional mortgage headaches—no digging through your personal income, tax returns, or employment history. With a DSCR loan, qualification comes down to one straightforward question: Can this property's rental income cover its own mortgage payment?

This approach to underwriting is a real breakthrough for investors dealing with complex tax situations, hefty write-offs, or anyone ready to grow their portfolio without bumping into the walls of conventional financing.

Benefits of DSCR Loans for Real Estate Investors

DSCR loans are changing the game for real estate investment financing. They offer advantages that directly address the most common obstacles you'll face when scaling your portfolio. Unlike conventional mortgages that box you in with strict qualification rules based on your personal income, DSCR loans zero in on what actually matters for investment properties: the cash flow they produce.

No Personal Income Verification Eliminates DTI Constraints

Here's the game-changer with DSCR loans: you can forget about personal income verification altogether. Traditional lenders want to see your W-2s, tax returns, pay stubs, and they'll calculate your Debt-to-Income (DTI) ratio—typically capping you at 43% to 50%. If you're self-employed or you're smart about maximizing tax deductions, this becomes a real roadblock. You could have a thriving rental portfolio throwing off serious cash flow, but on paper, your taxable income looks too slim to qualify for more financing.

DSCR loans cut right through this. The lender won't ask for your tax returns, won't calculate your DTI, and won't care about your personal earnings. What matters is one straightforward question: does the property's rental income cover its monthly debt payments? This frees you from the paperwork trap of personal income documentation, so your investment strategy—not your tax strategy—determines how much financing you can access.

This is especially powerful if you're:

- A real estate investor who invests for a living

- Self-employed and writing off business expenses that shrink your taxable income

- A high-net-worth individual with income spread across multiple entities

- Retired and living off investments instead of W-2 paychecks

- A commission-based earner whose income swings don't play nice with traditional underwriting

Unlimited Property Financing Removes Conventional Loan Caps

Here's where things get really interesting for serious investors. Conventional financing through Fannie Mae and Freddie Mac caps you at 10 financed properties. That's a hard ceiling that stops many investors in their tracks. Once you hit that limit, your options narrow: pay cash, hunt for portfolio lenders with less attractive terms, or simply stop growing.

DSCR loans? No property limits whatsoever. Whether you're financing 1 property or several properties, the question stays the same: does this property cash flow? That's it. This makes DSCR loans the go-to choice for investors serious about scaling their portfolios.

Let's break down what this means for your growth strategy:

| Financing Type | Property Limit | Scaling Potential |

|---|---|---|

| Conventional Mortgage | 10 properties maximum | Severely restricted beyond 10 units |

| DSCR Loan | No limit | Unlimited growth potential |

| Portfolio Lender | Varies (typically negotiated) | Dependent on relationship and terms |

| Commercial Loan | No limit (but different criteria) | Available but often requires larger properties |

This opens the door to a powerful "land and expand" approach—systematically acquiring cash-flowing properties across multiple markets, building wealth through appreciation and cash flow without running into artificial financing roadblocks.

Entity Vesting for Liability Protection and Asset Separation

With conventional mortgages, you usually have to close in your personal name, which means your personal assets are on the line if a tenant sues or something goes wrong at the property. DSCR loans let you—and often prefer you—close in the name of an LLC or Corporation. This gives you the liability protection that smart investors know is essential.

When you vest property in an LLC:

- Personal assets remain shielded from lawsuits related to the investment property

- Portfolio organization improves through separate entities for different properties or markets

- Tax planning flexibility increases with entity-level deductions and distributions

- Estate planning simplifies through transferable membership interests

- Professional credibility enhances when dealing with property managers, contractors, and tenants

Here's the bottom line: this structural advantage transforms real estate investing from a personal liability exposure into a properly insulated business operation. You can grow your portfolio without putting your primary residence, retirement accounts, or other personal wealth on the line if something goes sideways legally.

Short-Term Rental Income Qualification

The rise of platforms like Airbnb and VRBO has opened up exciting investment opportunities for savvy real estate investors. But here's the challenge: conventional lenders often don't know what to do with properties that lack traditional long-term leases. The good news? DSCR loan programs have evolved to meet you where you are, allowing you to qualify using projected short-term rental income instead of requiring those 12-month lease agreements.

Here's how lenders typically evaluate short-term rental income:

- Historical income documentation: 12-24 months of Airbnb/VRBO statements showing your actual rental receipts

- Market analysis: AirDNA reports or similar data demonstrating how comparable properties perform in your target area

- Appraisal projections: Form 1007 with short-term rental market analysis

- Hybrid approaches: A combination of your actual history and market projections

Keep in mind that most programs apply a 20% expense reduction to gross short-term rental income. This accounts for the higher operational costs you'll face—cleaning, utilities, maintenance, and platform fees—compared to traditional rentals. After this adjustment, your net income still needs to hit the required DSCR ratio, typically between 1.15x to 1.50x.

Key qualifications to know for short-term rental financing:

- Experience matters: If you're a first-time investor, you generally can't use STR income to qualify

- Minimum occupancy: AirDNA projections need to show at least 60% occupancy

- LTV restrictions: Expect caps at 60-75% rather than the standard 80%

- Property location: Rural properties are frequently excluded from STR programs

- Higher DSCR targets: Some lenders require minimum 1.15x rather than 1.00x for STR properties

This flexibility unlocks investment strategies that simply aren't possible with conventional financing. You can tap into vacation markets, urban short-term rental opportunities, and seasonal demand patterns that often generate significantly higher returns than traditional long-term rentals.

Scalability Advantages for Portfolio Growth

DSCR loans don't just remove the 10-property cap—they offer structural advantages that help you grow your portfolio faster:

Streamlined underwriting process: When you add a new property, you only need credit verification, a property appraisal, DSCR calculation and cash reserves (usually 3 to 9 months of PITIA). No complete financial review of your entire personal and business finances required.

This dramatically reduces the documentation burden and speeds up closing timelines.

Consistent qualification criteria: Here's something that'll make you smile—unlike conventional loans where each additional property triggers stricter scrutiny and higher reserve requirements, DSCR loans apply the same standards whether it's your first investment property or your fiftieth. If the property achieves the target DSCR, it qualifies. Simple as that.

Geographic diversification: Because qualification depends on individual property cash flow rather than your overall financial profile, you can expand into new markets without the headache of explaining unfamiliar locations to conventional underwriters. The property either cash flows or it doesn't—the market location becomes secondary.

Acquisition velocity: Here's where things get exciting for serious investors. Using DSCR loans, you can close multiple properties simultaneously or in rapid succession, limited only by available capital for down payments and reserves rather than waiting for income documentation updates or DTI recalculations.

| Scaling Metric | Conventional Financing | DSCR Financing |

|---|---|---|

| Maximum properties per year | Limited by DTI recalculation | Limited only by capital and deal flow |

| Documentation per property | Complete financial package | Property-specific only |

| Geographic restrictions | Lender comfort zones | None (property-driven) |

| Portfolio size ceiling | 10 financed properties | Unlimited |

| Time between acquisitions | 30-45 days minimum | 14-21 days possible |

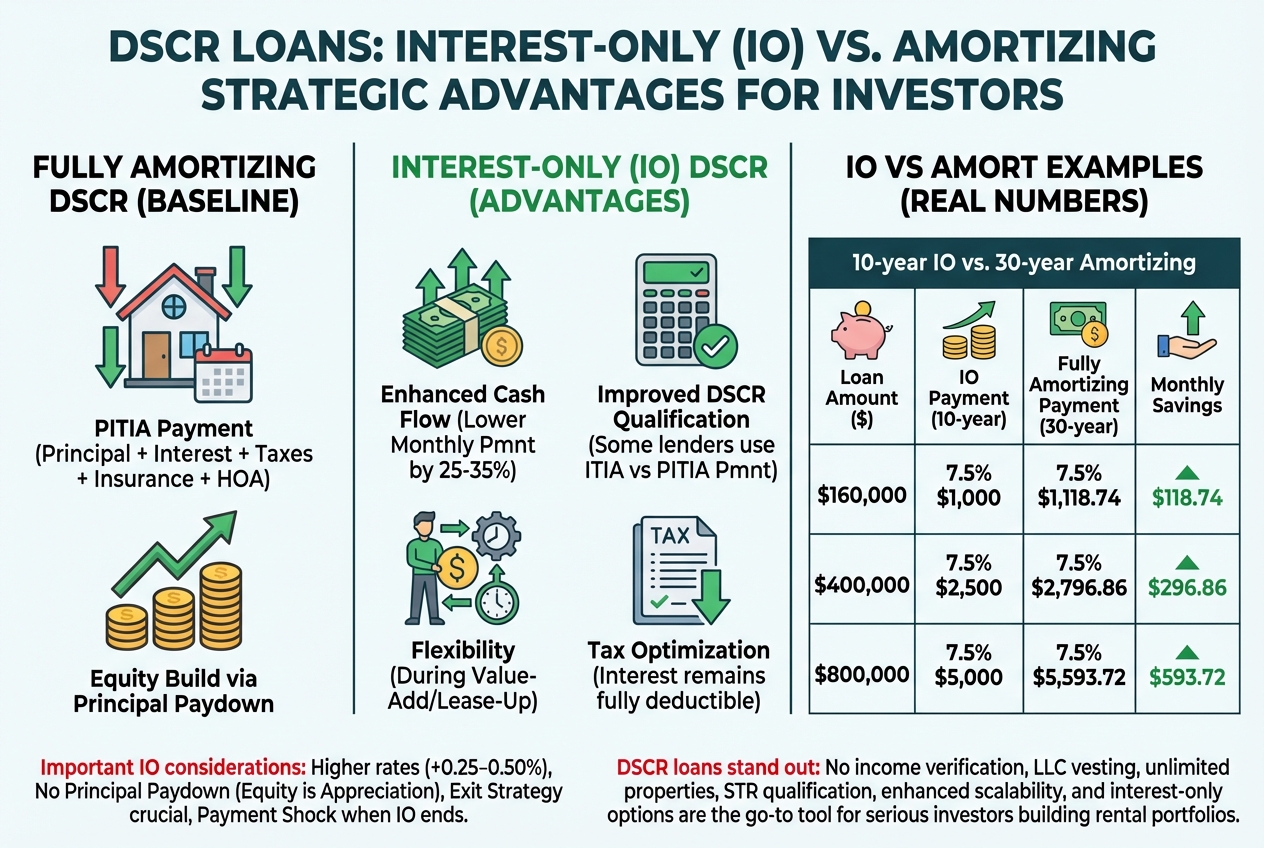

Interest-Only Payment Options for Cash Flow Maximization

Many DSCR loan programs offer interest-only payment structures, typically for the first 5 to 10 years of the loan term. This feature provides powerful cash flow advantages that conventional amortizing loans simply cannot match.

How interest-only payments work:

- You pay only the interest portion of the loan each month

- No principal reduction occurs during the IO period

- After the IO period expires, the loan converts to a fully amortizing payment based on the remaining term

- Monthly payments during the IO period are typically 25-35% lower than fully amortizing payments

Strategic advantages of interest-only structures:

Enhanced cash flow: Lower monthly payments increase your net operating income, improving both cash-on-cash returns and the property's ability to weather vacancies or unexpected expenses.

Improved DSCR qualification: Here's a nice perk—some lenders calculate your DSCR using just the interest-only payment (ITIA) instead of the full principal-and-interest amount (PITIA). That can make qualifying easier when you're working with properties that have tighter cash flow margins.

Capital efficiency: Those monthly savings aren't just sitting idle. You can put that extra cash toward down payments on your next property, helping you grow your portfolio faster through quicker reinvestment cycles.

Flexibility during value-add phases: Renovating a property or working through lease-up? Interest-only payments give you some breathing room while you stabilize the asset and get it performing.

Tax optimization: Your interest payments remain fully deductible, and by deferring principal paydown, you're letting your capital work harder—compounding through additional acquisitions rather than building equity in just one property.

Example comparison:

| Loan Amount | Interest Rate | IO Payment (10-year) | Fully Amortizing Payment (30-year) | Monthly Savings |

|---|---|---|---|---|

| $160,000 | 7.5% | $1,000 | $1,119 | $119 |

| $400,000 | 7.5% | $2,500 | $2,797 | $297 |

| $800,000 | 7.5% | $5,000 | $5,594 | $594 |

Important considerations:

- Interest-only loans typically come with slightly higher rates (usually 0.25-0.50%) compared to fully amortizing options

- Be ready for payment shock when the IO period ends and your payments jump to fully amortizing levels

- During the IO period, your equity growth depends entirely on property appreciation—you're not paying down principal

- Plan your exit strategy carefully, whether that's refinancing or selling before the IO period wraps up

When you add it all up—no income verification, LLC vesting, unlimited properties, short-term rental qualification, enhanced scalability, and interest-only options—DSCR loans stand out as the go-to financing tool for serious investors building substantial rental portfolios. These advantages tackle the exact limitations that hold back conventional financing, opening doors to investment strategies and growth that simply aren't possible through traditional mortgage channels.

DSCR Loan Concepts

Understanding Non-QM Loans and DSCR Classification

Let's break down what sets DSCR loans apart by looking at Qualified Mortgages (QM) versus Non-Qualified Mortgages (Non-QM). Your typical conventional mortgage—the kind most folks use for their primary home—is a Qualified Mortgage backed by government-sponsored enterprises like Fannie Mae and Freddie Mac. These loans play by strict federal rules set by the Consumer Financial Protection Bureau (CFPB), meaning you'll need to hand over W-2s, tax returns, and detailed debt-to-income ratio (DTI) calculations.

Non-QM loans? They operate outside those rigid federal guidelines. But here's the thing—Non-QM doesn't mean risky or predatory. It simply means lenders have the freedom to use different criteria for approval. For DSCR loans, that means zeroing in on the property's cash flow instead of your personal financial picture.

Since DSCR loans are designed purely for business-purpose investment properties, lenders skip the deep dive into your personal income, tax returns, or personal debt-to-income ratio. This Non-QM classification opens up real flexibility for you as an investor while keeping lending standards grounded in solid property economics.

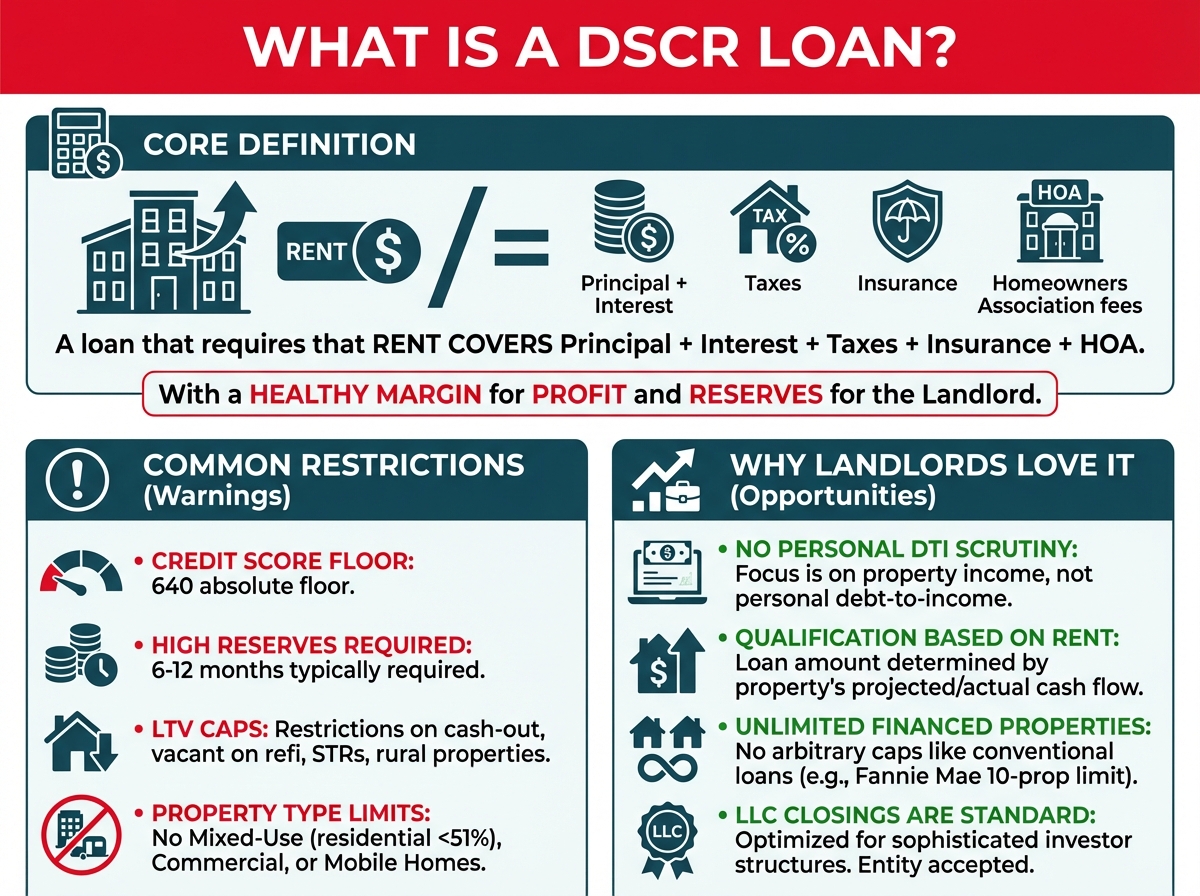

The Debt Service Coverage Ratio Concept

Let's break down the core concept behind DSCR lending: the Debt Service Coverage Ratio. Simply put, this ratio tells you whether a property can pay for itself. The debt service coverage ratio calculation compares what the property brings in each month against what it costs to own—that's your PITIA (Principal, Interest, Taxes, Insurance, and Association dues).

Here's the straightforward formula:

DSCR = Gross Monthly Rent ÷ Monthly PITIA

A DSCR of 1.00x means you're breaking even—rent covers your costs exactly. Hit 1.25x, the sweet spot for the best rates and terms, and you've got 25% extra income beyond your debt payments. That buffer gives you breathing room for vacancies, repairs, and yes, actual profit in your pocket.

How DSCR Loans Differ from Conventional Financing

DSCR loans and conventional mortgages play by completely different rules. Here's what sets them apart:

No Personal Income Documentation: With conventional loans, you're drowning in paperwork—paystubs, W-2s, tax returns, employment verification. DSCR loans? None of that. Your personal income doesn't matter one bit. It's all about what the property earns.

No DTI Ratio Limitations: Conventional lenders typically cut you off when your debt-to-income ratio hits 43-50%. That puts a hard ceiling on your portfolio growth. DSCR loans don't factor in your personal DTI at all, so you can keep scaling without hitting that wall.

Entity Vesting Allowed: Conventional loans usually force you to hold title personally, putting your assets at risk. DSCR loans let you close in an LLC or corporation right from the start. That means real asset protection and a clear line between your investments and personal finances.

How DSCR Loans Work: Understanding the Formula and Calculation

Here's the good news about DSCR loans: they're built on a simple math equation that puts your property's performance front and center. Forget digging through years of tax returns or explaining gaps in employment history. DSCR lenders want to know just one thing: Can this property pay for itself with the rent it brings in?

The DSCR Formula Explained

Let's break down the Debt Service Coverage Ratio formula into plain English:

DSCR = Gross Monthly Rent ÷ Monthly PITIA

Think of this ratio as your property's financial report card. A DSCR of 1.25x? That means your rental income exceeds your monthly obligations by 25%—giving you breathing room for those inevitable vacancies, surprise repairs, and market ups and downs.

Breaking Down the PITIA Components

Let's walk through each piece of PITIA so you can run these numbers confidently on any property you're considering:

Principal (P): This is the chunk of your payment that actually chips away at what you owe. On a $160,000 loan at 7.5% interest over 30 years, expect around $119 of your early payments to go toward principal.

Interest (I): What you're paying the lender for the privilege of borrowing their money. Using that same loan scenario, roughly $1,000 of your initial payment covers interest.

Taxes (T): Take your annual property tax bill and divide by 12. Paying $2,400 yearly in property taxes? That's $200 added to your monthly PITIA.

Insurance (I): Your homeowner's insurance, broken down monthly. A typical investment property might run $1,200 per year, which means $100 each month.

Association dues (A): Any HOA or condo fees you're on the hook for. These vary wildly—anywhere from $50 to several hundred dollars depending on the property.

Let's add it all up for our example: $119 (P) + $1,000 (I) + $200 (T) + $100 (I) + $0 (A) = $1,419 per month.

Determining Gross Rental Income: The Form 1007 Standard

Here's the deal: lenders won't just take your word for what a property can rent for. They need proof, and that comes in one of two ways:

Market Rent Analysis (Form 1007): When your property gets appraised, the appraiser fills out a Single-Family Comparable Rent Schedule (Form 1007). This document looks at similar properties that have recently rented in your area and determines the market rent—basically, what an objective expert believes your property should command right now.

Actual Lease Agreement: Already have a tenant? Great! Lenders will look at your existing lease. But here's the key rule you need to know: lenders always use the lower of your actual lease amount or the market rent from the Form 1007.

Let's break that down with an example. Say your tenant pays $1,500 per month, but the Form 1007 comes back showing market rent at $1,350. The lender uses $1,350 for qualification. Flip it around—your lease is $1,350 but market rent appraises at $1,500? The lender still uses $1,350. This protects everyone from inflated lease agreements that might not hold up over time.

Good news though: some lenders make exceptions when your actual lease is significantly higher than market rent. If you can show 2-3 months of verified rent receipts proving consistent payment, certain programs will let you use the higher lease amount—though it's usually capped at 120% of appraised market rent.

Understanding Acceptable DSCR Ratios

Not all DSCR ratios are treated the same, and knowing these thresholds helps you maximize your leverage and lock in better rates:

1.00x DSCR (Break-Even): Think of this as the baseline for most programs. At 1.00x, your rental income exactly covers your PITIA payment—no more, no less. Some lenders will work with this ratio, but expect trade-offs: credit score requirements (680+), down payments (20-30%), and more reserves on hand (3-6 months), depending on the loan amount.

0.75x - 0.99x DSCR (Negative Cash Flow): Yes, some programs actually allow properties that don't fully cover their costs. Why? Because smart investors sometimes accept short-term losses when they're banking on long-term appreciation. However, expect severe restrictions: maximum 65-75% LTV, credit scores above 680, substantial reserves (6+ months), and significantly higher interest rates. First-time investors are universally excluded from these programs.

1.20x - 1.25x DSCR (Target Range): Here's where the magic happens. A ratio in this range opens the door to maximum leverage (80% LTV for purchases), the most competitive interest rates, and standard reserve requirements (1-3 months). Most lenders consider 1.25x the golden number—it gives you breathing room while proving your property can generate solid cash flow.

1.50x+ DSCR (Strong Cash Flow): Now we're talking. Properties exceeding 1.50x are the cream of the crop. While these ratios won't typically unlock additional leverage beyond 80% LTV, they may qualify for slightly better pricing and signal to lenders that you know how to pick winners.

Real-World DSCR Calculation Examples

Let's roll up our sleeves and walk through several scenarios so you can see exactly how DSCR calculations work:

Example 1: Strong Cash Flow Property

- Purchase Price: $250,000

- Down Payment (20%): $50,000

- Loan Amount: $200,000

- Interest Rate: 7.5%

- Monthly Principal & Interest: $1,398

- Property Taxes (monthly): $250

- Insurance (monthly): $125

- HOA (monthly): $0

- Total Monthly PITIA: $1,773

- Market Rent (Form 1007): $2,250

DSCR Calculation: $2,250 ÷ $1,773 = 1.27x

This property checks all the boxes with a solid DSCR above the 1.25x target, qualifying you for maximum 80% LTV and competitive rates.

Example 2: Break-Even Scenario

- Purchase Price: $180,000

- Down Payment (25%): $45,000

- Loan Amount: $135,000

- Interest Rate: 8.0%

- Monthly Principal & Interest: $991

- Property Taxes (monthly): $200

- Insurance (monthly): $100

- HOA (monthly): $0

- Total Monthly PITIA: $1,291

- Market Rent (Form 1007): $1,300

DSCR Calculation: $1,300 ÷ $1,291 = 1. 01x

This barely positive cash flow property qualifies at the minimum threshold, but the investor needed a larger 25% down payment and will face higher rates due to the tight margin.

Example 3: Interest-Only Payment Structure

- Purchase Price: $300,000

- Down Payment (25%): $75,000

- Loan Amount: $225,000

- Interest Rate: 8.25%

- Monthly Interest-Only Payment: $1,547

- Property Taxes (monthly): $300

- Insurance (monthly): $150

- HOA (monthly): $100

- Total Monthly ITIA (Interest-Only): $2,097

- Market Rent (Form 1007): $2,800

DSCR Calculation: $2,800 ÷ $2,097 = 1.34x

Here's a smart move: by choosing an interest-only payment option (available in many DSCR loans for the first 10 years), this investor significantly boosts their cash flow while keeping a solid DSCR ratio. One important heads-up: some lenders calculate DSCR using the interest-only payment, while others require the fully amortizing payment—so always confirm with your lender before you commit.

Loan-to-Value (LTV) Limits and Their Impact

How much you can borrow compared to your property's value depends on several factors. Let's break down what you need to know:

Purchase Transactions (Maximum 80% LTV)

When you're buying an investment property, most DSCR programs limit your leverage to 80%, meaning you'll need a 20% down payment. This assumes:

- Credit score of 680-700+

- DSCR of at least 1.00x (though 1.20x+ puts you in a stronger position)

- Standard 1-4 unit residential property

- Long-term rental income (not short-term)

So for a $200,000 purchase, plan on bringing $40,000 down plus closing costs (typically 2-3% of the purchase price).

Rate/Term Refinances (Maximum 80% LTV)

Rate/term refinances—where you're adjusting your interest rate or loan term without pulling cash out—also cap at 80% LTV. But here's something crucial to remember: you must have owned the property for at least 6 months to use the new appraised value. Refinancing within 6 months of purchase? Your loan amount will be limited to your original cost basis (purchase price plus documented rehab costs).

Cash-Out Refinances (Maximum 70-75% LTV)

Cash-out refinances carry more risk for lenders, so LTV limits drop to 70-75% depending on the program and property characteristics. If your DSCR falls below 1.00x, expect the maximum to decrease further to 65-70%.

Let's break that down with a real example. Say your property appraises at $300,000:

- At 75% LTV: You can borrow up to $225,000

- At 70% LTV: You can borrow up to $210,000

- At 65% LTV: You can borrow up to $195,000

Here's something else to keep in mind: many programs cap the actual cash you can receive. Even if LTV allows a $225,000 loan, some lenders limit cash-in-hand to $500,000-$1,000,000, with unlimited cash-out only available when LTV stays below 65%.

Special Property Type Adjustments

Certain property types come with additional LTV restrictions you'll want to know about:

- Short-Term Rentals (Airbnb/VRBO): Maximum 70-75% LTV, with 20% expense deduction from gross rental income

- 2-4 Unit Properties: Maximum 75-80% LTV, often requiring minimum 1.15x-1.25x DSCR

- Foreign National Borrowers: Maximum 60-70% LTV regardless of DSCR strength

Getting a handle on these LTV limits helps you calculate your required down payment and potential cash-out proceeds. Here's the thing: the interplay between DSCR ratio and LTV determines your ultimate leverage. A property with a stellar 1.50x DSCR might still be limited to 75% LTV if it's a non-warrantable condo, while a standard single-family home with 1.25x DSCR easily achieves 80% LTV.

The bottom line: DSCR loans evaluate the property's cash flow first, then apply LTV limits based on transaction type and property characteristics. When you understand both components, you can accurately predict your financing terms before ever submitting an application.

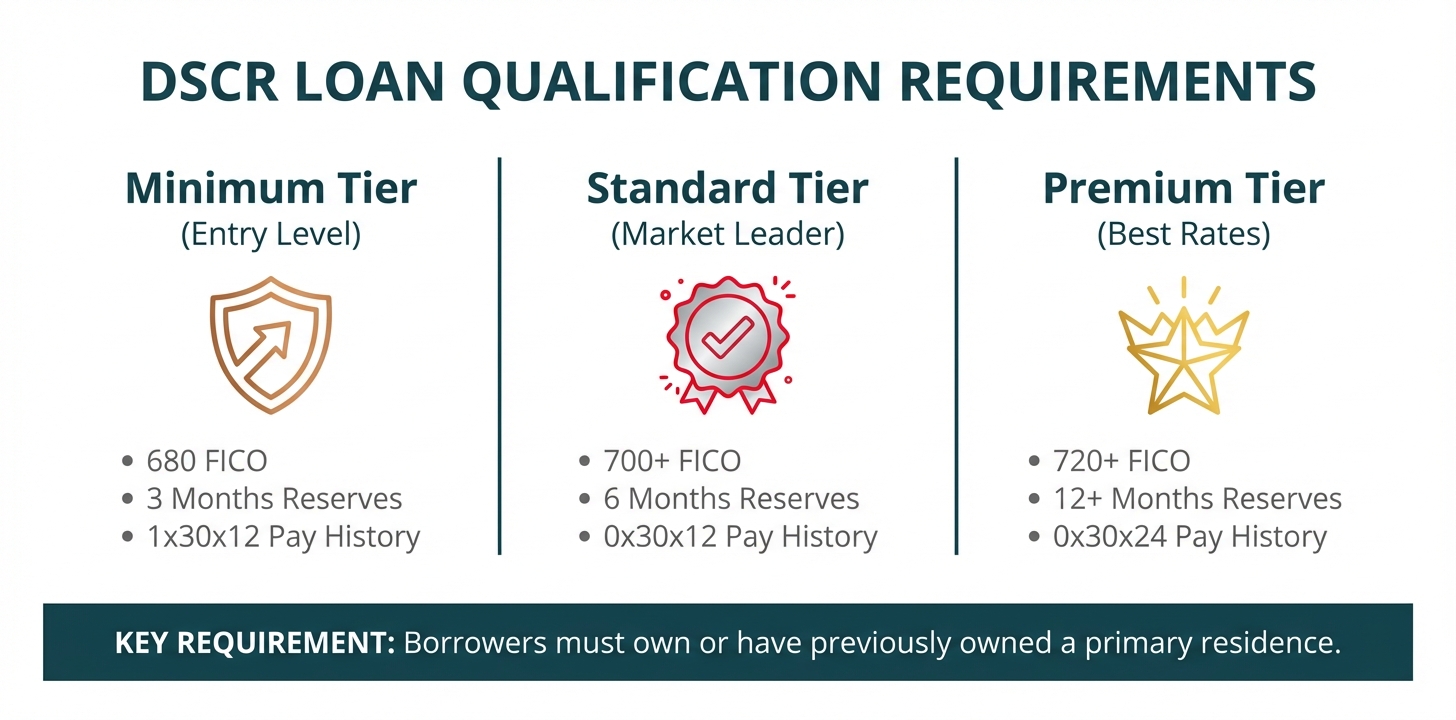

Qualification Requirements for DSCR Loans

Sure, DSCR loans skip the personal income paperwork, but lenders still want to see that you're financially responsible and have a solid track record. Let's break down the key qualification requirements so you can position yourself for the best terms and maximum leverage on your investment properties.

Comprehensive Qualification Requirements Table

| Qualification Category | Minimum Requirement | Standard Requirement | Premium Tier (Best Rates) | Notes |

|---|---|---|---|---|

| Credit Score (FICO) | 680 | 680-700 | 720+ | Scores below 680 mean reduced LTV and higher rates |

| Tradeline History | 2 tradelines for 24+ mos OR 1 mortgage line for 36+ mos | 3 tradelines for 12+ months | 4+ tradelines with diverse mix | Must show active usage within the last 12 months. |

| Mortgage Payment History | 1x30x12 | 0x30x12 | 0x30x24 | Some programs allow one 30-day late payment in the last 12 months (1x30x12), but 0x30x12 is required for premium pricing and max LTVs. |

| Reserves (Loan <$1M) | 3 months PITIA | 3-6 months PITIA | 6+ months PITIA | If DSCR is < 1.00x, lenders uniformly require a minimum of 6 months reserves regardless of loan size. |

| Reserves (Loan $1M-$1.5M) | 6 months PITIA | 6 months PITIA | 9+ months PITIA | Required across all properties. |

| Reserves (Loan >$1.5M) | 9 months PITIA | 9-12 months PITIA | 12-18+ months PITIA | Higher loan amounts strictly dictate larger reserve requirements. |

| Investor Experience | First-time allowed (strict caps apply) | 12+ months ownership / 1-2 properties | Multiple properties for 2+ years | First-time investors are typically capped at 75% LTV, min 680 FICO, min 1.00x DSCR, and cannot use short-term rental income. |

| Primary Residence | Must own or have owned | Must own | Current ownership preferred | First-Time Homebuyers" (do not own any real estate and currently rent) are universally ineligible for these investment programs. |

| Bankruptcy/Foreclosure Seasoning | 36 months | 48 months | 60+ months | 36 months from discharge/dismissal is the standard minimum for DSCR. Second-lien products (Equity Advantage) require 48 to 84 months. |

| Maximum Financed Properties | No limit | No limit | No limit | No limit on total properties owned, but lenders cap their own exposure (e.g., max 10 loans or $5M-$10M aggregate balance per borrower). |

| Down Payment Source | Documented liquid assets (seasoned 30-60 days) | Own funds (seasoned 30-60 days) | Own funds | Gift funds from immediate family ARE permitted, provided the borrower contributes a minimum of 10% of their own funds. |

| Outstanding Collections | <$2,000 (if <24 mos old) or <$2,500 (if >24 mos old) | Paid or payment plan | All resolved | Individual collections under these limits can remain open. Medical collections are completely excluded from these limits. |

| Tax Liens & Judgments | Documented repayment plan | Must be paid in full | All resolved | Can remain open ONLY if the borrower is on a documented repayment plan with at least 3 months of timely payments, and the payment is included in the DTI/DSCR. |

| Minimum Loan Amount | $55,000-$75,000 | $100,000 | $150,000+ | Small loans under $100k often face full-balance interest accrual on fix & flip loans or slightly reduced LTVs. |

| Maximum Loan Amount | $2,000,000 | $2,500,000 | $3,500,000 - $6,250,000+ | Higher amounts (above $1.5M - $2M) require two full independent appraisals. Blanket/portfolio loans can reach up to $6.25M. |

Credit Score Requirements

Your credit score plays a big role in DSCR loan qualification—it directly affects how much leverage you can get and what interest rate you'll pay. The standard minimum is 680 FICO, which gets you in the door for most DSCR loan programs. Want that maximum 80% LTV? You'll typically need a score of 700 or higher.

Here's something important: when a property has negative cash flow (DSCR below 1.00x), lenders get pickier about credit scores. Expect a minimum requirement of 700-720 to balance out the extra risk of a property that doesn't fully cover its debt.

Here's some perspective: conventional investment property loans often require similar or higher credit scores, with many lenders setting the bar at 680 for standard programs. The real win with DSCR loans isn't a lower credit score threshold—it's skipping the income verification that often trips up otherwise creditworthy investors.

Tradeline History and Financial Responsibility

Beyond your credit score, lenders look at your tradeline history to see how well you've handled credit over time. DSCR loan programs typically require a minimum of three active tradelines reporting for at least 12 months, or alternatively, two active tradelines reporting for 24 months or longer.

Active tradelines can include:

- Credit cards with regular usage and payment history

- Auto loans or leases

- Student loans

- Other mortgages or lines of credit

- Personal loans from established financial institutions

What matters most here is showing a track record of responsible credit management. Lenders want to see that you've kept these accounts in good standing, with minimal late payments and reasonable utilization rates on revolving credit. Accounts that have been sitting unused for long periods may not count toward this requirement.

Your mortgage payment history gets extra attention. Most DSCR loan programs require a clean mortgage history, commonly expressed as 0x30x12—meaning zero mortgage payments 30 days or more late in the last 12 months. If you currently own a home or other investment properties, any late mortgage payments within the past year can disqualify you or significantly impact your terms.

Reserve Requirements

Mortgage reserves—liquid assets you've set aside specifically to cover housing costs—are a key piece of DSCR loan qualification. These reserves show lenders you can handle vacancies, unexpected repairs, or other cash flow hiccups without missing payments.

Standard Reserve Requirements:

For most DSCR loans under $1 million, lenders require 3 to 6 months of PITIA (Principal, Interest, Taxes, Insurance, and Association dues) in liquid reserves. The exact amount depends on factors like your credit score, experience level, and the property's DSCR ratio.

Escalating Requirements for Larger Loans:

As loan amounts grow, so do reserve requirements:

- Loans between $1M-$1. 5M: Typically require 6-9 months of PITIA in reserves

- Loans above $1.5M: May require 9-12 months or more

- Foreign national borrowers: Often require 12 months regardless of loan size

Higher Reserves for Riskier Scenarios:

Some property types and borrower profiles come with higher reserve requirements:

- Properties with DSCR below 1.00x: 6-12 months of reserves

- First-time investors: 6-12 months of reserves

- Vacant properties: May require 3+ additional months beyond standard requirements

- Multiple financed properties: Additional reserves may be required per property

What Qualifies as Reserves:

Here's what lenders typically accept as reserve assets:

- Checking and savings accounts

- Money market accounts

- Stocks, bonds, and mutual funds (typically valued at 70% of market value due to volatility)

- Retirement accounts like 401(k)s and IRAs (often valued at 60-70% due to early withdrawal penalties)

- Cryptocurrency holdings (valued at 60% and must be liquidated for closing costs)

- Cash-out refinance proceeds (can be used to satisfy reserve requirements)

One important note: your down payment doesn't count toward reserves—you'll need separate, liquid funds beyond what's required to close the deal.

Getting a handle on reserve requirements for rental property loans puts you in a stronger position when planning your DSCR financing strategy.

Experience Considerations

Your track record as a real estate investor plays a big role in shaping your DSCR loan terms and options. Lenders typically sort borrowers into two camps: experienced investors and first-time investors.

Experienced Investor Definition:

You qualify as an experienced investor if you've owned at least one investment property for 12 months or more within the last 3 years. You'll need to back this up with mortgage statements, tax returns showing rental income, or property tax records. The property can be currently owned or previously sold, as long as the ownership duration requirement is met.

Benefits of Experienced Investor Status:

Here's where your track record really pays off. As an experienced investor, you unlock some serious advantages:

- Maximum leverage up to 80% LTV on purchases and rate-term refinances

- Access to 75% LTV on cash-out refinances

- Eligibility for short-term rental (Airbnb/VRBO) income qualification

- Lower reserve requirements (often 3-6 months vs. 6-12 for first-timers)

- Access to blanket loan programs for portfolio refinancing

- Better interest rate pricing (typically 0.25-0.50% lower than first-time investors)

First-Time Investor Restrictions:

New to the investment game? Good news: DSCR loans are still more accessible than conventional options. Just keep these guidelines in mind:

- Maximum LTV typically capped at 75% (requiring 25% down payment)

- Cannot use short-term rental income for qualification

- Ineligible for blanket loan programs

- Higher reserve requirements (6-12 months of PITIA)

- May face slightly higher interest rates

Important Note on Primary Residence Ownership:

Here's something crucial to understand: first-time real estate investors must already own a primary residence or have owned one previously. If you've never owned any property at all, DSCR loans won't be the right fit—these are strictly non-owner-occupied, business-purpose loans designed for investors, not first-time homebuyers.

Housing History and Credit Event Seasoning

Your housing payment history and any past credit events matter more than you might think. Lenders want to see that you've demonstrated financial responsibility and bounced back from any previous setbacks.

Recent Credit Events:

Had some financial bumps in the road? Here's how long you'll need to wait before qualifying for a DSCR loan:

- Bankruptcy (Chapter 7 or 11): Minimum 36-48 months from discharge date

- Bankruptcy (Chapter 13): Minimum 24-36 months from discharge, or 12 months with court approval and perfect payment history

- Foreclosure: Minimum 36-48 months from completion date

- Short Sale: Minimum 36-48 months from completion date

- Deed-in-Lieu: Minimum 36-48 months from completion date

- Loan Modification: Minimum 12-24 months with perfect payment history

These waiting periods are longer than many conventional loan programs. Why? Because investment properties carry higher risk, and lenders need confidence that you've regained solid financial footing.

Recent Late Payments:

Beyond major credit events, your recent payment history carries real weight:

- Mortgage Payments: As we covered earlier, most programs want to see 0x30x12 (that means no 30-day late payments in the last 12 months)

- Installment Loans: Late payments within the past year may need explanation letters and could affect your approval

- Revolving Accounts: Recent missed payments on credit cards or lines of credit signal potential financial management concerns

Collections and Judgments:

Here's how outstanding collections and judgments typically get handled:

- Medical collections under $5,000: Usually ignored or won't require payoff

- Non-medical collections: May need to be paid off before closing if the total exceeds $2,000-$5,000

- Judgments: Must be paid off or have a payment plan established

- Tax liens: Federal tax liens must be paid; state/local liens may work with payment plans

Improving Your Qualification Profile

Not quite meeting all the requirements for the best DSCR loan terms? Here are some practical strategies to strengthen your position:

Credit Score Improvement:

- Pay down credit card balances to reduce utilization below 30%

- Dispute any inaccurate items on your credit report

- Become an authorized user on a family member's established credit card

- Avoid opening new credit accounts in the 6 months before applying

- Set up automatic payments to ensure perfect payment history

Building Tradeline History:

- Open a secured credit card if you lack sufficient tradelines

- Keep older accounts open even if you don't use them regularly

- Use credit cards monthly and pay them off in full

- Consider a credit-builder loan from a credit union

Accumulating Reserves:

- Start setting aside monthly savings specifically for reserves

- Consider liquidating non-essential assets to build cash reserves

- Delay your property purchase by 6-12 months to build adequate reserves

- Use cash-out refinancing on existing properties to create liquidity

Gaining Experience:

- Purchase your first investment property with a investor focused loan or alternative financing

- Hold the property for 12 months to achieve "experienced investor" status

- Document your rental income and expenses meticulously

- Consider house-hacking (living in a multi-unit property) as a stepping stone

Understanding these qualification requirements is your first step toward securing DSCR financing and building your investment property portfolio. By meeting or exceeding these standards, you're setting yourself up for success—think better terms, stronger negotiating power, and loan structures that actually work for your investment strategy.

Who Should Consider a DSCR Loan?

DSCR loans aren't the right fit for every investor, but they can be a game-changer for certain real estate buyers who hit roadblocks with traditional financing. Let's break down the investor profiles that benefit most—so you can decide if this tool belongs in your wealth-building toolkit.

Self-Employed Investors with Complex Tax Returns

If you're self-employed—running your own business, freelancing, or working as an independent contractor—you know the headache of qualifying for a conventional mortgage. You might be doing great financially, but your tax returns paint a different picture. Smart write-offs, depreciation, and legitimate business deductions can shrink your taxable income well below what you're actually bringing in.

Traditional lenders want to see it all: two years of tax returns, profit and loss statements, and a deep dive into your Debt-to-Income (DTI) ratio based on that reduced taxable income. So even if you're pulling in $200,000 a year, savvy (and completely legal) tax strategies might show only $60,000 in adjusted gross income—knocking you out of the running for loans you could handle with ease.

Here's where DSCR loans change the game. Qualification hinges on the property's cash flow, not your personal income, so your tax returns don't enter the equation. The lender isn't concerned whether you report $50,000 or $500,000—they just want to see that the rental property earns enough to cover its own costs. That makes DSCR loans a perfect match for self-employed investors ready to grow their portfolios without being held back by smart tax planning.

BRRRR Method Investors Needing Reliable Cash-Out Refinancing

The BRRRR method—Buy, Rehab, Rent, Refinance, Repeat—has become one of the most popular wealth-building strategies in real estate investing. The concept is straightforward: purchase a distressed property below market value, renovate it to increase its worth, rent it out to generate income, refinance to pull out your initial capital, and repeat the process with the next property.

The refinance step is where many investors hit a wall with conventional financing. Traditional lenders impose strict limits on cash-out refinances for investment properties, often requiring extensive income documentation and capping the number of financed properties at ten. If you're self-employed or already own multiple properties, conventional refinancing becomes increasingly difficult.

Here's the good news: DSCR loans solve this critical bottleneck. The cash-out refinance process focuses exclusively on the property's ability to service the debt, not your personal financial situation. Once you've completed renovations and stabilized rental income, you can refinance based on the new appraised value—typically up to 75% LTV—and pull out your invested capital to put toward your next deal. This creates a powerful cycle where your initial capital keeps working for you across multiple properties, helping you grow your portfolio faster without needing fresh cash for each acquisition.

For BRRRR investors, DSCR loans deliver two things you need most: speed and certainty. The streamlined underwriting process means faster closings, and the property-focused qualification means you're not boxed in by personal income constraints or the ten-property cap that holds back conventional financing.

Investors Using Short-Term Rental Strategies

Short-term rentals through platforms like Airbnb and VRBO have changed the game for real estate investors, often generating 2-3 times the income of traditional long-term rentals. The challenge? Qualifying for financing using short-term rental income has historically been tough with conventional loans, which typically demand 12-24 months of documented rental history and tend to view STR income with skepticism.

DSCR loans offer a much better fit for short-term rental strategies. Many DSCR programs let you qualify using projected short-term rental income based on market analysis tools like AirDNA, or they'll use the property's long-term rental value from an appraiser's market rent analysis. Some programs even accept actual short-term rental income with as little as 12 months of documented history.

Keep in mind that STR-focused DSCR loans typically come with slightly more conservative terms—expect a 1.00x to 1.25x DSCR requirement, maximum LTV of 70-75%, and some investor experience. But they provide a clear path to financing properties specifically intended for short-term rental use. This is particularly valuable in vacation markets, urban areas with strong tourism, or properties near major attractions where short-term rental income significantly exceeds long-term rental potential.

Here's the good news: the flexibility to use STR income for qualification means you can underwrite deals based on their actual revenue potential rather than being forced to use artificially low long-term rental comparables. This opens doors to investment opportunities in markets where the short-term rental premium makes properties financially viable—properties that would otherwise fail to qualify under traditional long-term rental assumptions.

Comparison of Borrower Types and DSCR Loan Benefits

| Investor Type | Primary Challenge | DSCR Loan Solution | Key Benefits |

|---|---|---|---|

| Self-Employed with Complex Tax Returns | Low taxable income due to write-offs makes DTI qualification impossible | No personal income verification required | Qualify based on property cash flow, not tax returns; unlimited portfolio growth without DTI constraints |

| BRRRR Method Investors | Cash-out refinancing restrictions and income documentation requirements slow portfolio velocity | Streamlined cash-out refinance based solely on property performance | Fast capital recycling; no personal income hurdles; refinance up to 75% of new appraised value |

| First-Time Investors | Overwhelming documentation requirements and strict conventional lending standards | Simplified qualification focusing on credit and property cash flow | Accessible entry point; no employment verification; straightforward underwriting process |

| Aggressive Scalers (10+ Properties) | Conventional loan cap at 10 financed properties | No limit on number of financed properties | Unlimited portfolio expansion; LLC vesting for liability protection; consistent qualification criteria at any scale |

| Short-Term Rental Investors | Difficulty qualifying using STR income with conventional loans | Programs accepting projected STR income or 12-month rental history | Underwrite based on actual STR revenue potential; access vacation and high-income markets; flexible income documentation |

Here's the bottom line: conventional financing creates artificial barriers that have nothing to do with the actual risk or viability of your investment. DSCR loans remove those roadblocks and let the numbers speak for themselves. DSCR loans cut through these obstacles by zeroing in on what really counts: does the property bring in enough income to cover its debt payments? This fresh approach to underwriting opens doors for investors who have the financial chops but don't check all the boxes for traditional lending.

Special Considerations for Different Borrower Profiles

Self-Employed Investors:

If you're self-employed, here's some good news: you're exactly who DSCR loans were designed for. If you're self-employed with complex tax returns or significant legal write-offs that minimize your taxable income, DSCR loans offer a clear path to qualification without the DTI scrutiny of conventional loans. Your business income doesn't matter—only the property's cash flow.

That said, you'll still need to meet the credit, reserve, and experience requirements we covered above. Good news: your business bank accounts can satisfy reserve requirements, and business credit cards can count toward tradeline requirements if they report to personal credit bureaus.

Foreign National Investors:

Foreign nationals (non-US citizens and non-permanent residents) can absolutely qualify for DSCR loans, though you'll face some additional requirements:

- Valid passport and visa documentation

- US credit report (if available) or international credit report

- Higher reserve requirements (typically 12 months)

- Lower maximum LTV (usually 60-70%)

- May require larger down payments (30-40%)

- Must have US bank account for mortgage payments

Investors with Multiple Properties:

Already own several financed properties? Here's where DSCR loans really shine. While conventional loans typically limit investors to 10 financed properties, DSCR loans have no such cap. Keep in mind that each additional property in your portfolio may trigger higher reserve requirements—lenders often require 2-6 months of reserves per financed property.

Investors Using Business Entities:

Planning to close in an LLC or corporation? All members owning 20-25% or more must personally guarantee the loan and meet the qualification requirements individually. The entity itself doesn't have a credit score—the guarantors' credit profiles are what matter. So if you have multiple LLC members, the member with the lowest credit score often determines your qualification tier.

Pros and Cons of DSCR Loans

Let's break down what makes DSCR loans shine—and where they might fall short. These loans open doors for real estate investors like few other options can, but they're not a perfect fit for everyone. Here's what you need to know to decide if they're right for you.

The Advantages: Why Investors Choose DSCR Loans

Streamlined, No-Income-Verification Underwriting

Here's the big one: DSCR loans don't care about your personal income documentation. No W-2s, no tax returns, no pay stubs, no employment verification letters. If you're self-employed and write off expenses to keep your taxable income low, you know how frustrating traditional lending can be. With DSCR loans, that headache disappears. Your personal Debt-to-Income ratio? Doesn't matter. What matters is whether the property pays for itself.

This means less paperwork and faster approvals. No more waiting around for IRS tax transcripts or explaining your business structure six different ways. Underwriters zero in on three things: the property appraisal, the rent schedule (Form 1007), and your credit score. Simple as that.

Interest-Only Payment Options for Maximum Cash Flow

Want to keep more money in your pocket each month? Many DSCR programs let you make interest-only payments for the first 5 to 10 years. This can be a smart move when you're building your portfolio and need every dollar working for you.

Let's look at real numbers on a $200,000 loan at 8% interest:

- Principal + Interest Payment: $1,468/month

- Interest-Only Payment: $1,333/month

- Monthly Savings: $135

That's $16,200 over a 10-year interest-only period—money you can put toward building reserves, upgrading your property, or snagging your next investment. The DSCR calculation can even be performed using the IO payment (ITIA—Interest, Taxes, Insurance, Association dues) rather than the fully amortizing PITIA. This means you can qualify for higher leverage more easily.

LLC Vesting and Liability Protection

Here's a big win: unlike conventional loans that require you to close in your personal name, DSCR loans let you vest the property directly in an LLC or Corporation. Why does this matter? It creates a legal wall between your personal assets and your investment properties.

If a tenant files a lawsuit or a property-related claim pops up, your personal home, retirement accounts, and other assets stay protected. For investors building multi-property portfolios, this peace of mind is often worth the slightly higher loan cost.

Unlimited Property Financing

Conventional loans hit you with a hard cap—usually 10 financed properties, max. After that, you're stuck with commercial lending or portfolio loans that come with much tougher terms. DSCR loans? No such limit.

Whether you're financing property number 5 or number 50, the underwriting stays the same. This makes DSCR loans the go-to choice for investors who want to scale aggressively and build a portfolio of dozens of rentals.

Short-Term Rental Income Qualification

Good news for vacation rental investors: many DSCR programs accept short-term rental income from Airbnb and VRBO—something conventional loans typically won't touch. Lenders can qualify you using:

- 12-month historical income from your STR operation (bank statements, platform reports)

- Projected income based on market data from tools like AirDNA

Fair warning: STR qualification does come with extra requirements (typically a 20% expense haircut, lower LTV caps around 70-75%, and proof you're an experienced investor). But it opens doors to profitable vacation rental markets that would otherwise be off the table.

The Disadvantages: Understanding the Trade-Offs

Prepayment Penalties (1-5 Year Terms)

Here's the biggest thing to watch out for with DSCR loans: prepayment penalties (PPP). With conventional loans, you can refinance or sell whenever you want without extra costs. DSCR loans? Most come with a 1 to 5-year prepayment penalty clause.

Here's what those PPP structures typically look like:

- Step-Down: 5% / 4% / 3% / 2% / 1% (drops each year)

- Fixed Percentage: 5% for the whole penalty period

- Six-Month Interest: You pay six months of interest charges

Let's put this in real numbers. Say you take out a $200,000 DSCR loan with a 5-4-3-2-1 step-down penalty. If you sell or refinance in year two, you're looking at an $8,000 hit (4% of your loan balance). That can really eat into your profits, especially if you're running the BRRRR strategy and counting on a quick refinance.

Good news for some of you: Certain states don't allow or limit prepayment penalties on 1-4 unit residential properties. Alaska, Minnesota, and New Mexico ban them completely. States like Ohio and Pennsylvania have loan amount thresholds—below those amounts, PPPs aren't allowed.

Higher Interest Rates (1-2% Above Conventional)

DSCR loans fall into the Non-QM (Non-Qualified Mortgage) category, which means you'll pay more in interest than you would with a conventional owner-occupied mortgage. Right now in 2025, DSCR loan interest rates typically sit between 7.25% and 9.00%, while conventional investment property rates run from 6.25% to 7.50%.

That 1-2% difference adds up. Here's what it looks like in your wallet:

Example: $200,000 Loan, 30-Year Fixed

- Conventional at 6.5%: $1,264/month, $255,000 total interest

- DSCR at 8.0%: $1,468/month, $328,480 total interest

- Difference: $204/month, $73,480 over 30 years

But here's the thing—you need to weigh this cost against what you're getting. If a DSCR loan helps you close on a property you couldn't qualify for otherwise, or lets you grow beyond conventional loan limits, that extra cost might be worth every penny.

Larger Down Payments (20-30%)

DSCR loans ask for more skin in the game compared to conventional investment property loans:

- Standard DSCR Purchase/Refi: 20% down (80% LTV maximum)

- Cash-Out Refinance: 25-30% equity required (70-75% LTV maximum)

- DSCR < 1.00x or Lower Credit: 30-35% down (65-70% LTV)

Here's the reality: conventional investment property loans often let experienced investors with solid credit put down just 15% (85% LTV). This higher equity requirement with DSCR loans means you'll need more cash for each property, which can pump the brakes on your portfolio growth if capital is tight.

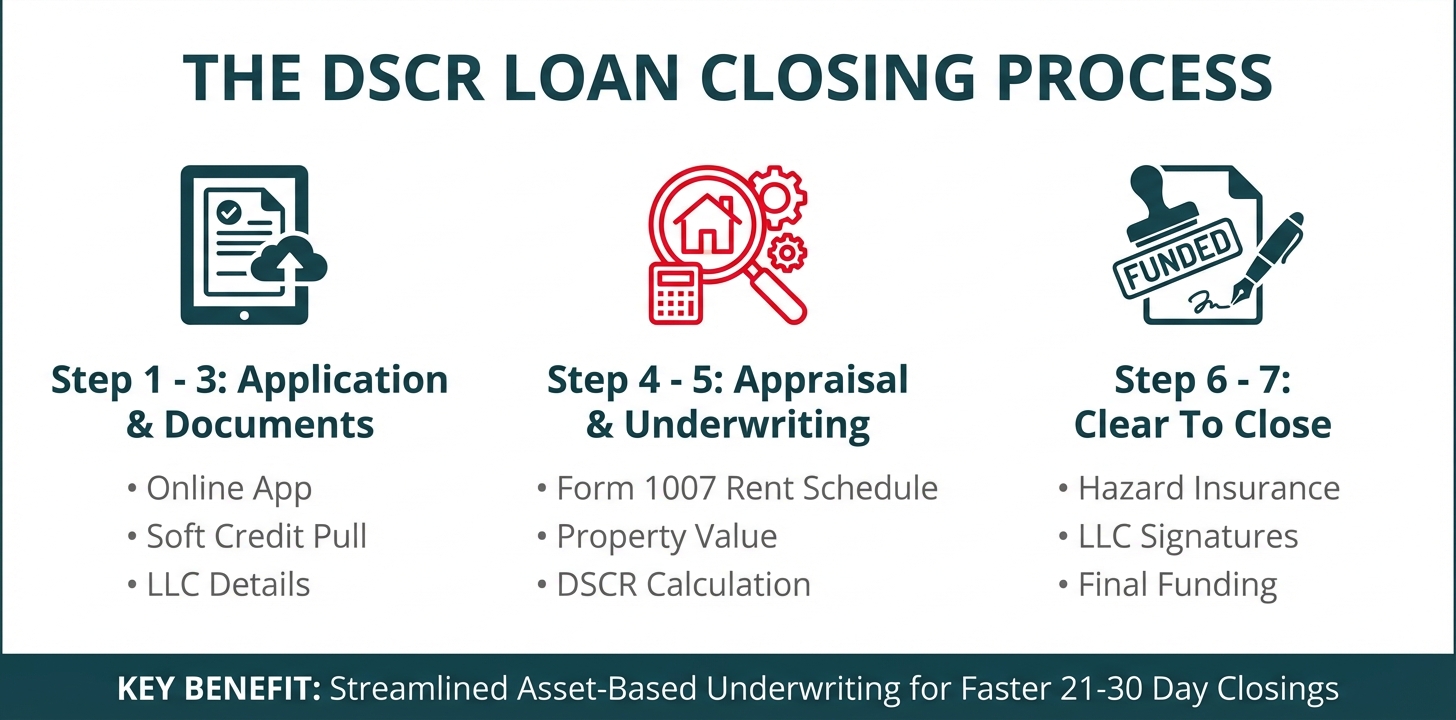

Steps to Get a DSCR Loan: A Streamlined Process

Good news: the DSCR loan process is built for speed and simplicity. Since there's no personal income verification, you skip a lot of the paperwork headaches. While traditional mortgages can drag on for 30 to 60 days, DSCR loans typically close faster thanks to streamlined documentation. Let's walk through each step and show you how OfferMarket makes it even easier.

DSCR Loan Process Timeline

| Step | Timeline | Key Activities | OfferMarket Support |

|---|---|---|---|

| Pre-Application | Days 1 | Run property calculations, gather LLC docs | Instant quote tool, DSCR calculator |

| Application Submission | Day 1-2 | Submit Urgent items and complete the full Loan Application | Simplified online application |

| Credit & Liquidity Review | Day 2-3 | Allow soft credit pull and submit bank statements | Soft credit pull |

| Entity Review | Day 3-4 | Borrowing entity verification | Entity compliance check |

| Appraisal Ordered | Day 4-6 | Lender orders property appraisal and Form 1007 | Market expertise for strong appraisals |

| Appraisal Completion | Days 6-9 | Property inspection, rent schedule analysis | Coordination with local appraisers |

| Underwriting Review | Days 9-12 | DSCR calculation, condition review | Direct communication on any issues |

| Title Work | Days 12-15 | Title search, lien verification, clearance | Relationships with reliable title companies |

| Insurance Binding | Days 15-16 | Secure landlord insurance policy | Integrated insurance quotes |

| Clear to Close | Day 16-18 | Final approval issued by underwriter | Immediate notification to all parties |

| Closing | Day 18-21 | Document signing, funding, recording | Flexible scheduling, remote options available |

| Total Timeline | 18-21 Days | From application to keys in hand | Average 21-30 days with OfferMarket |

Step 1: Submit Application

First up: submit your loan application online, where we ask a few multiple choice questions such as:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

OfferMarket Advantage: Our instant quote system lets you run the numbers on potential deals before you even submit a formal application. You can run multiple property scenarios through our calculator to identify which investments offer the best cash flow potential, ensuring you only submit applications for properties that make financial sense.

Step 2: Upload Purchase contract and complete sections marked URGENT

Once you move forward, our streamlined system walks you through the full underwriting checklist inside your dashboard.

First you will need to complete Processing section that are marked URGENT. We like to kick off our process by having you upload a Purchase Contract, authorize a soft credit pull through our website as well as complete a loan application where you enter some additional information.

If your property requires an appraisal we also like you to complete appraisal authorization on the first day so we can order the appraisal on the next business day which should accelerate all the timelines. In some cases for fix and flip loans we allow a desktop appraisal which make things a lot more streamlined.

Step 3: Upload remaining documents

You’ll complete and upload:

- ID Verification

- Bank Statements

- Borrowing Entity Details (LLC/Corp)

- W-9 Form

- ACH Form

- Primary residence verification

- Incumbency certificate

- Insurance information (OfferMarket can help with that since we specialize in insurance for Fix and Flip properties)

Step 4: Property Appraisal and Title

The property appraisal is the most critical piece of a DSCR loan because it determines both your property value and the qualifying rental income. The lender orders a full appraisal that includes Form 1007 (Single-Family Comparable Rent Schedule).

Appraisal Components:

- Property Value Assessment: Determines current market value using comparable sales

- Form 1007 Rent Schedule: Establishes market rent based on comparable rental properties in the area

- Property Condition: Documents the physical condition and any needed repairs

- Rental Market Analysis: Provides context on local rental demand and typical lease terms

Rent Determination Rules:

- The lender uses the lower of the actual lease amount or the appraised market rent

- If the property is vacant, most programs calculate income at 75-90% of market rent

- For short-term rentals, appraisers may reference AirDNA data or comparable STR properties

Once appraisal is complete, the closing process moves to the title company. OfferMarket's integrated platform connects directly with title companies across the country, giving everyone involved real-time access to closing documents, wire instructions, and settlement statements.

OfferMarket Advantage: Since we also specialize in real estate listings and know local markets inside and out, we can help you spot properties likely to appraise well with strong rent schedules—before you even make an offer. Our insurance division also provides immediate property insurance quotes, which are required for the appraisal and closing process.

Step 5: DSCR Calculation by Underwriting

Once the appraisal is complete, our underwriting team gets to work calculating the property's DSCR to see if it meets program guidelines. This is the moment of truth—where the property either qualifies or needs some adjustments.

Here's How We Calculate It:

- Determine Qualifying Rent: We take the lower of actual lease or Form 1007 market rent

- Calculate Monthly PITIA: We add up principal, interest, property taxes, insurance, and HOA dues

- Compute DSCR Ratio: We divide gross monthly rent by monthly PITIA

- Prepare documents for closing: We verify the ratio meets minimum requirements (typically 1.00x-1.25x)

Let's Walk Through an Example:

- Purchase Price: $300,000

- Down Payment (25%): $75,000

- Loan Amount: $225,000

- Interest Rate: 7.5%

- Monthly P&I: $1,573

- Property Taxes: $250/month

- Insurance: $150/month

- HOA: $0

- Total PITIA: $1,973

- Market Rent (Form 1007): $2,500

- DSCR: $2,500 ÷ $1,973 = 1.27x

Good news for this property—it qualifies with room to spare. That 1.27x ratio clears most program minimums and signals solid cash flow potential.

OfferMarket Advantage: Want to run these numbers yourself before applying? Our DSCR loan calculator lets you play with variables like down payment amount, estimated rent, and property taxes to see exactly how different scenarios affect your qualification.

Step 6: Landlord Insurance

While underwriting reviews the DSCR calculation, we're also moving forward on insurance and title work. Both need to be buttoned up before closing.

Insurance Requirements:

- Hazard Insurance: Standard property coverage for fire, wind, and other perils

- Flood Insurance: Required if your property sits in a FEMA flood zone

- Landlord/Dwelling Policy: Specific coverage designed for non-owner-occupied rentals

- Umbrella Policy: Often a smart move for extra liability protection

OfferMarket Advantage: Our integrated insurance services let you secure competitive landlord insurance quotes right through our platform—no need to shop around. This eliminates the need to shop separately and ensures your coverage meets lender requirements from day one. Our relationships with title companies also help keep the title process moving smoothly, cutting down on unnecessary delays.

Step 7: Clear to Close and Loan Document Signing

Once underwriting gives the thumbs up on your DSCR calculation, insurance is in place, and title comes back clear, your loan gets "clear to close" status. Now it's time to sign those final loan documents.

Final Steps:

- Final Closing Disclosure: Your chance to review final loan terms, closing costs, and cash to close

- Wire Instructions: Confirmation of where to send your down payment and closing cost funds

- Signing Appointment: Sit down with a notary or closing attorney to sign your loan documents

- LLC Signature: You'll sign in the name of your LLC, not your personal name

- Funding: The lender wires loan proceeds to the title company

- Recording: Deed and mortgage get recorded with the county

Typical Timeline: Most mortgage closings happen 21-30 days after application, though DSCR loans can sometimes wrap up faster since there's less paperwork involved.

OfferMarket Advantage: Our efficient process and connections with multiple lenders mean we can often get DSCR loans closed in just 21-30 days. We keep you in the loop at every step, so you always know where things stand and what's needed next. Our team handles coordination between all parties—appraiser, insurance provider, title company, and lender—so nothing slips through the cracks.

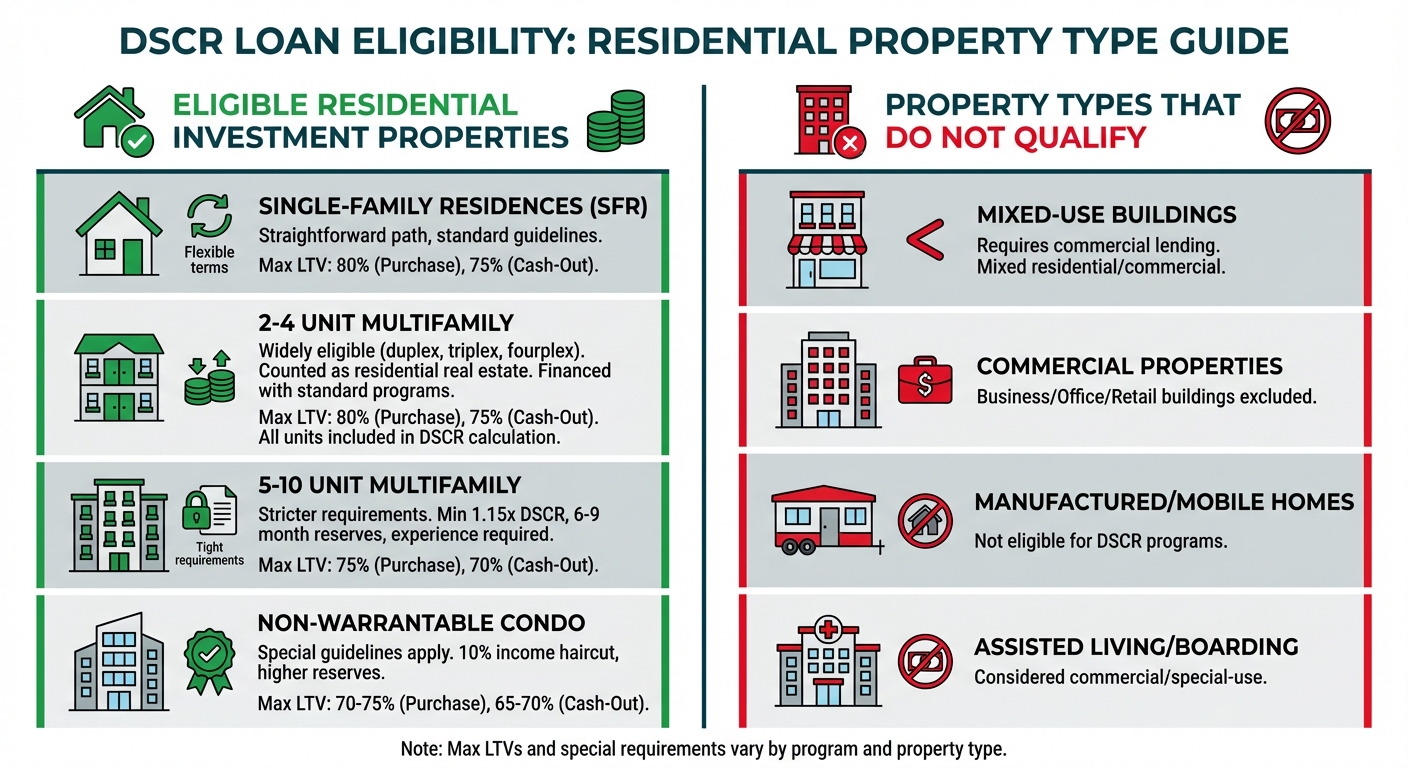

Property Types & Special Use Cases

Knowing which properties qualify for DSCR financing—and under what conditions—helps you make smarter decisions as you grow your portfolio. While DSCR loans offer more flexibility than conventional financing, certain property types and use cases come with specific restrictions, adjusted leverage, or additional documentation requirements.

Property Type Eligibility Table

| Property Type | Eligible? | Max LTV (Purchase) | Max LTV (Cash-Out) | Special Requirements |

|---|---|---|---|---|

| Single-Family (1 Unit) | ✅ Yes | 80% | 75% | Standard DSCR guidelines |

| 2-4 Unit Multifamily | ✅ Yes | 80% | 75% | All units included in DSCR calculation |

| 5-10 Unit Multifamily | ✅ Yes | 75% | 70% | Min 1.15x DSCR, 6-9 month reserves, experience required |

| Non-Warrantable Condo | ✅ Yes | 70-75% | 65-70% | 10% income haircut, higher reserves |

| Condotel | ⚠️ Restricted | 65-75% | 60-65% | Severe restrictions, limited lender availability |

| Rural Property | ⚠️ Restricted | 65-70% | 60-65% | No STR income allowed, limited comparables |

| Mixed-Use | ❌ No | N/A | N/A | Requires commercial lending |

| Manufactured/Mobile | ❌ No | N/A | N/A | Not eligible for DSCR programs |

| Assisted Living/Boarding | ❌ No | N/A | N/A | Considered commercial/special-use |

Standard Property Eligibility: 1-4 Unit Residential

DSCR lending is built around 1-4 unit residential properties—single-family homes, duplexes, triplexes, and fourplexes. These are the bread and butter of most investor portfolios and qualify under standard DSCR guidelines with maximum leverage of 80% LTV on purchases and rate-term refinances, and 75% LTV on cash-out refinances.

For 2-4 unit properties, lenders typically factor all units into the DSCR calculation. If one unit is vacant, the appraiser's Form 1007 estimates market rent for that unit, but many programs apply a 75-90% haircut to the vacant unit's projected income to account for turnover risk. This conservative approach ensures the property can still cover the debt even with occasional vacancies.

Multifamily Properties: 5-10 Units

Ready to scale up? Good news—DSCR programs extend beyond the conventional 4-unit cap. Properties with 5-10 units are eligible under most DSCR programs, though you'll encounter tighter underwriting standards:

- Minimum DSCR requirement increases to 1.15x-1.25x (compared to 1.00x for smaller properties)

- Maximum LTV typically drops to 75% on purchases and 70% on cash-out refinances

- Higher reserve requirements of 6-9 months of PITIA are standard

- Experience requirement is often mandatory—first-time investors are generally prohibited from financing 5+ unit properties

Here's the upside for experienced investors: these larger properties often generate stronger cash flow per dollar invested and benefit from economies of scale in property management.

Why OfferMarket for Your DSCR Loan?

Let's be real—not all DSCR lenders bring the same value to the table. You've got traditional banks, mortgage brokers, and specialized lenders all competing for your business, each with their own strengths and limitations. Here's what makes OfferMarket different: we bring together listings, insurance, and lending all in one place. This means a smoother experience that saves you time and money while helping you grow your portfolio faster.

The OfferMarket Advantage: Everything You Need, One Platform

Here's what typically happens: investors juggle multiple companies—one for finding properties, another for insurance, and yet another for financing. It's messy, inefficient, and opportunities slip through the cracks. OfferMarket changes that game entirely. We've built a complete ecosystem where every piece of your investment puzzle fits together seamlessly.

Real Estate Listings Expertise: We don't just crunch numbers—we understand deals. Our team knows what makes a property cash flow, which neighborhoods are on the rise, and how to spot opportunities that meet DSCR requirements before you even submit your application. This market knowledge means faster approvals and more confident underwriting decisions for you.

Insurance Integration: Property insurance directly impacts the PITIA calculation that determines your DSCR. Our insurance expertise helps you secure competitive coverage without inflating your monthly obligations. We often find insurance savings that boost your DSCR ratio by 0.05x to 0.10x—that could mean qualifying at 80% LTV instead of 75% LTV, potentially saving you tens of thousands in down payment requirements.

Lending Excellence: Unlike single-source lenders limited to their own products, OfferMarket connects you with multiple capital providers to secure the most competitive rates and terms available. Our broker model means we work for you, not for a single lending institution. Your success is our success.

Access to Multiple Capital Providers: Your Competitive Edge

Here's where things get exciting. While a traditional bank gives you one set of terms on a take-it-or-leave-it basis, we shop your deal across multiple lenders simultaneously to find the best combination of:

- Interest rates (we often find differences of 0.25% to 0.75% between providers)

- Prepayment penalty structures (some lenders offer shorter PPP terms or step-down schedules)

- Reserve requirements (ranging from 3 to 12 months depending on the program)

- Maximum leverage (LTV options from 65% to 80% based on your profile)

- Underwriting flexibility (some lenders are more accommodating for unique property types or borrower situations)

This multi-provider approach is especially valuable if you have a complex scenario—whether you're a foreign national, a first-time investor, or seeking financing for short-term rentals or properties with DSCR below 1. 00x. Where one lender might decline or offer unfavorable terms, another in our network may have a program perfectly suited to your needs.

Streamlined Process: From Application to Closing

Time is money in real estate investing, and OfferMarket's streamlined process ensures you can close deals quickly and efficiently. Our integrated platform eliminates redundant paperwork, reduces back-and-forth communication, and accelerates timelines at every stage:

Instant Quote Tool: Before you even pick up the phone, OfferMarket's instant quote tool provides preliminary pricing and terms in seconds. Simply input your property details, purchase price, and estimated rent, and you'll receive an immediate indication of what programs you qualify for and at what rates. This lets you evaluate multiple deals rapidly and zero in on the opportunities with the strongest numbers. Go ahead—try our instant quote with an example deal to see what we can do for you. No commitment, no sales pressure, just straightforward information.

Simplified Documentation: Our team knows exactly what underwriters need and how to package your application for maximum efficiency. We'll walk you through gathering LLC documents, bank statements, and property information in a logical sequence that prevents delays and re-submissions.

Coordinated Closing: Because we understand both the lending and insurance sides of the transaction, we coordinate these moving parts seamlessly. Insurance quotes are obtained early, appraisals are ordered promptly, and title work proceeds without bottlenecks. The result? Closings that consistently meet or beat projected timelines, giving you confidence when negotiating purchase contracts or planning your next move.

Expert Guidance Through DSCR Complexity

DSCR loans, while powerful, come with nuances that can trip up even experienced investors. OfferMarket's team serves as your expert guide through every complexity:

DSCR Optimization: We help you structure deals to maximize your DSCR ratio, whether that means adjusting your down payment, exploring interest-only payment options, or identifying properties with stronger rent-to-price ratios.

Entity Structuring: Closing in an LLC gives you liability protection, but your entity needs to be set up correctly from the start. We'll guide you through LLC formation, operating agreements, and guarantor requirements so your application moves smoothly through underwriting.

Reserve Planning: Knowing what reserves you'll need across different loan sizes and scenarios helps you put your capital to work more efficiently. We'll show you how to leverage your existing assets, use cash-out proceeds strategically, and plan for future acquisitions without locking up more cash than necessary.

Program Selection: With dozens of DSCR programs out there, picking the right one takes some know-how. Should you accept a higher rate for a shorter prepayment penalty? Does it make sense to increase your down payment to unlock better terms? We'll give you data-driven recommendations based on your specific investment strategy and timeline.

The DSCR Calculator: Your Portfolio Planning Powerhouse

Beyond financing individual deals, OfferMarket gives you powerful tools to build and optimize your entire portfolio. Our DSCR loan calculator does much more than crunch payment numbers—it's a full analysis tool that lets you:

Compare Multiple Properties: Plug in details for several potential acquisitions and instantly see which ones generate the strongest cash flow and require the least cash to close.

Model Different Scenarios: Adjust down payment amounts, interest rates, and rental income projections to see exactly how changes affect your DSCR and qualification.

Plan Your Growth: Figure out how many properties you can acquire with your available capital, accounting for down payments, reserves, and closing costs across multiple deals.

Optimize Cash Flow: Find the right balance between leverage and monthly cash flow by comparing standard amortization against interest-only payment structures.

Use OfferMarket's DSCR loan calculator to run mock calculations for your target properties and build a data-driven acquisition strategy that maximizes your returns while keeping your finances strong.

Getting Started: Your Path to DSCR Financing Excellence

Here's the truth: the difference between average returns and exceptional portfolio growth often comes down to who's handling your financing. OfferMarket's combination of deep expertise, smart technology, and access to multiple providers sets you up for success from day one.

Take the First Step: Head to OfferMarket's instant quote tool and plug in details for a property you're eyeing (or test it out with sample numbers). In seconds, you'll see preliminary pricing and terms—no commitment, no pressure, just clarity.

Analyze Your Strategy: Use our DSCR loan calculator to compare potential acquisitions, test different down payment scenarios, and identify properties with the best mix of cash flow and capital efficiency.

Connect with Experts: When you're ready to move forward, our team is here to answer your questions, walk you through the details, and kick off your application. We'll work with you to structure the optimal financing solution for your specific situation and investment goals.

Real estate wealth is built one smart decision at a time. Choosing the right financing partner is one of the most important decisions you'll make. Choose OfferMarket, and experience the difference that integrated expertise, competitive access, and investor-focused service can make in your portfolio growth journey.

Next Steps: Get an Instant DSCR Loan Quote

Ready to turn knowledge into action? The fastest way to get started is to see real numbers on a real deal. OfferMarket's instant quote tool gives you immediate loan estimates—no phone calls, no scheduled meetings, no lengthy applications. You can evaluate potential investment properties in minutes, not days, and make confident, data-driven decisions about where to put your capital.

Why Use OfferMarket's Instant Quote Tool?

Here's the reality: traditional lenders make you jump through hoops. Full applications, stacks of documentation, and days or weeks of waiting just to get preliminary numbers. OfferMarket's instant quote cuts through all that. Simply plug in basic property details—purchase price, estimated rent, property taxes, insurance costs—and you'll get an immediate estimate of your loan terms, monthly payment, and cash needed to close.

This no-obligation tool puts you in the driver's seat:

- Evaluate multiple deals at once without getting bogged down in lengthy pre-approval processes

- Compare cash flow projections across different properties to spot the highest-performing investments

- Know your closing costs upfront so you can budget with confidence and avoid surprises

- Test different scenarios by adjusting down payment amounts, interest-only options, or property types

Here's a practical example: say you're eyeing three different rental properties in your target market. You can run instant quotes on all three in about 15 minutes. The tool shows you which property delivers the strongest DSCR ratio, requires the least cash to close, and generates the best monthly cash flow. This comparative analysis is invaluable when you're competing in fast-moving markets where properties move quickly.

Leverage the DSCR Calculator for Mock Calculations

Beyond instant quotes, OfferMarket's DSCR loan calculator lets you run detailed mock calculations on target properties before you even make an offer. Here's what you can figure out:

- Exact DSCR ratios based on market rent estimates and projected PITIA payments